SLIDE 1

3/13/2015 1

2015 Cotton Situation and Outlook

Don Shurley Professor Emeritus of Cotton Economics Department of Agricultural and Applied Economics University of Georgia Arkansas Farm Bill Webinar March 12, 2015

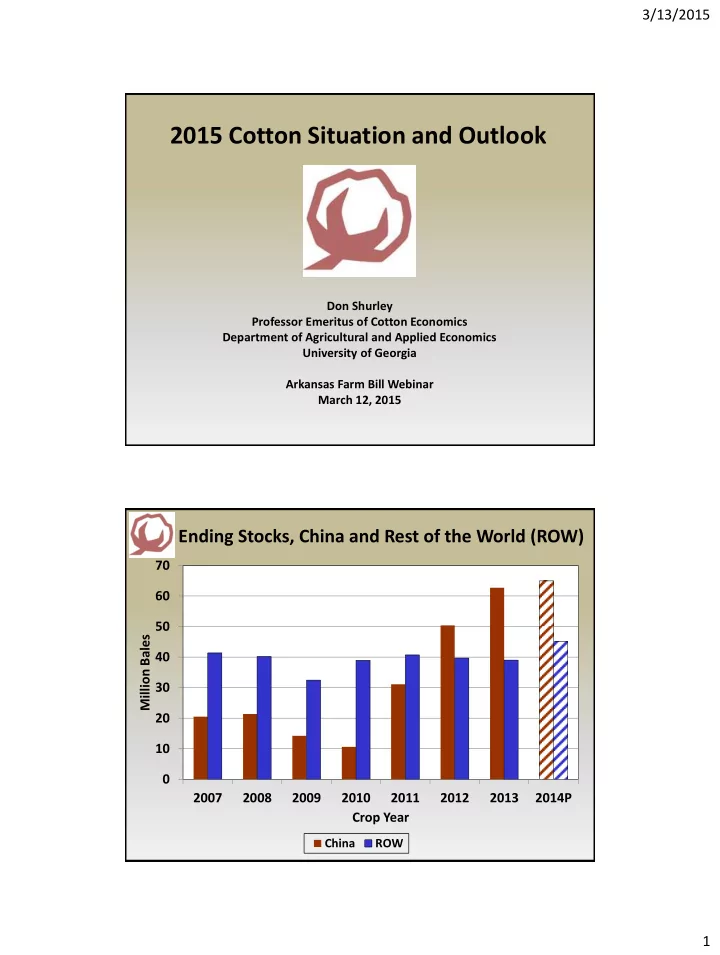

10 20 30 40 50 60 70 2007 2008 2009 2010 2011 2012 2013 2014P Million Bales Crop Year

China ROW