SLIDE 1

1

Q4

JOHAN DENNELIND PRESIDENT & CEO

YEAR-END REPORT JANUARY – DECEMBER 2017

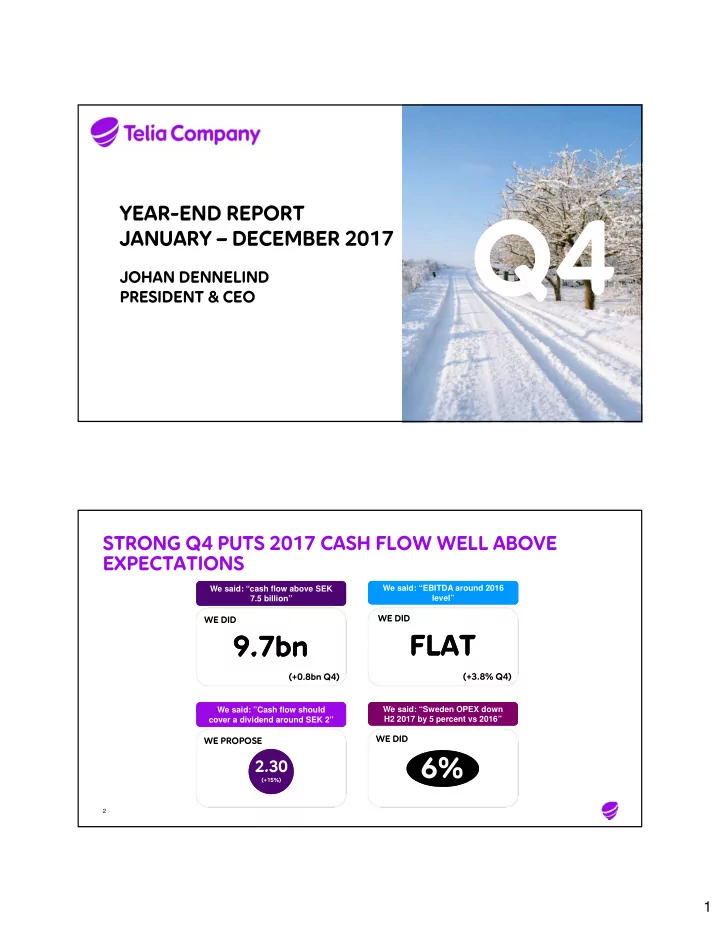

STRONG Q4 PUTS 2017 CASH FLOW WELL ABOVE EXPECTATIONS

2 We said: “cash flow above SEK 7.5 billion” We said: “cash flow above SEK 7.5 billion” We said: “Sweden OPEX down H2 2017 by 5 percent vs 2016” We said: “Sweden OPEX down H2 2017 by 5 percent vs 2016” We said: ”Cash flow should cover a dividend around SEK 2” We said: ”Cash flow should cover a dividend around SEK 2” We said: “EBITDA around 2016 level” We said: “EBITDA around 2016 level”6% 9.7bn 9.7bn

WE DID WE DID WE DID WE PROPOSE

2.30

(+15%)FLAT FLAT +3.8%

Q4+0.8bn

Q4(+3.8% Q4) (+0.8bn Q4)