SLIDE 1

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets Session 6 • Applications of Perfect Competition Page 1

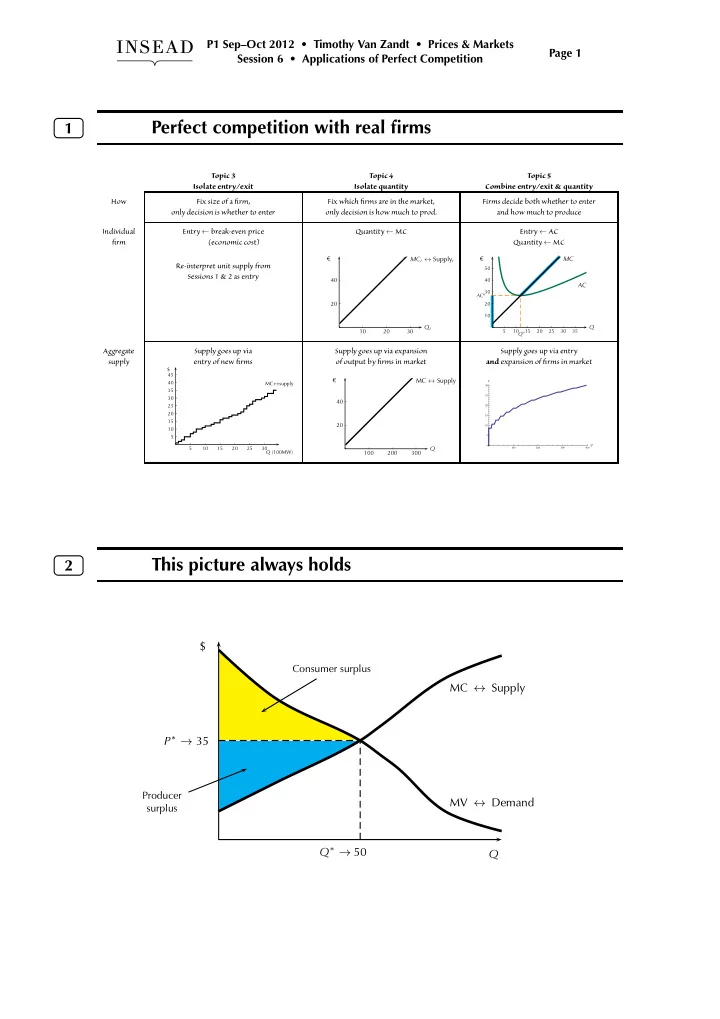

1

Perfect competition with real firms

Topic 3 Topic 4 Topic 5 Isolate entry/exit Isolate quantity Combine entry/exit & quantity How Fix size of a firm, Fix which firms are in the market, Firms decide both whether to enter

- nly decision is whether to enter

- nly decision is how much to prod.

and how much to produce Individual Entry ← break-even price Quantity ← MC Entry ← AC firm (economic cost) Quantity ← MC Re-interpret unit supply from Sessions 1 & 2 as entry

20 40 10 20 30

MCi ↔ Supplyi €

Qi

10 20 30 40 50 5 10 15 20 25 30 35

AC MC €

Q

Qu ACu

Aggregate Supply goes up via Supply goes up via expansion Supply goes up via entry supply entry of new firms

- f output by firms in market

and expansion of firms in market

MC↔supply 5 10 15 20 25 30 35 40 45 5 10 15 20 25 30 Q (100MW) $

20 40 100 200 300

MC ↔ Supply €

Q

100 200 300 400 Q 5 10 15 20 25 30 P