SLIDE 1

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets Review Session Page 1

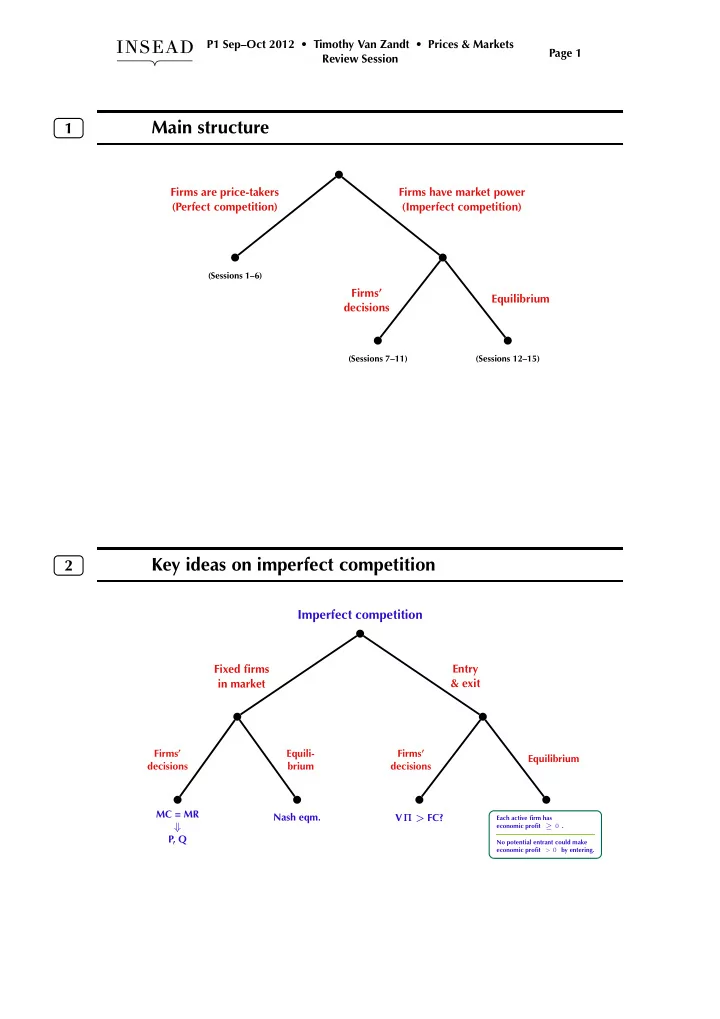

1

Main structure

(Sessions 1–6)

(Firms’ decisions & equilibrium)

Firms are price-takers (Perfect competition) Firms have market power (Imperfect competition)

(Sessions 7–11)

Firms’ decisions

(Sessions 12–15)

Equilibrium

In each case: fixed firms in the market, then entry/exit

2

Key ideas on imperfect competition

Imperfect competition

Fixed firms in market

MC = MR ⇓ P, Q Firms’ decisions Nash eqm. Equili- brium

Entry & exit

VΠ > FC? Firms’ decisions

Each active firm has economic profit ≥ 0 . No potential entrant could make economic profit > 0 by entering.