SLIDE 1

Mt020.02 Slide 1 on 4/12/00

raj

Compound Interest (continued) Well use the term scenario to refer to - - PDF document

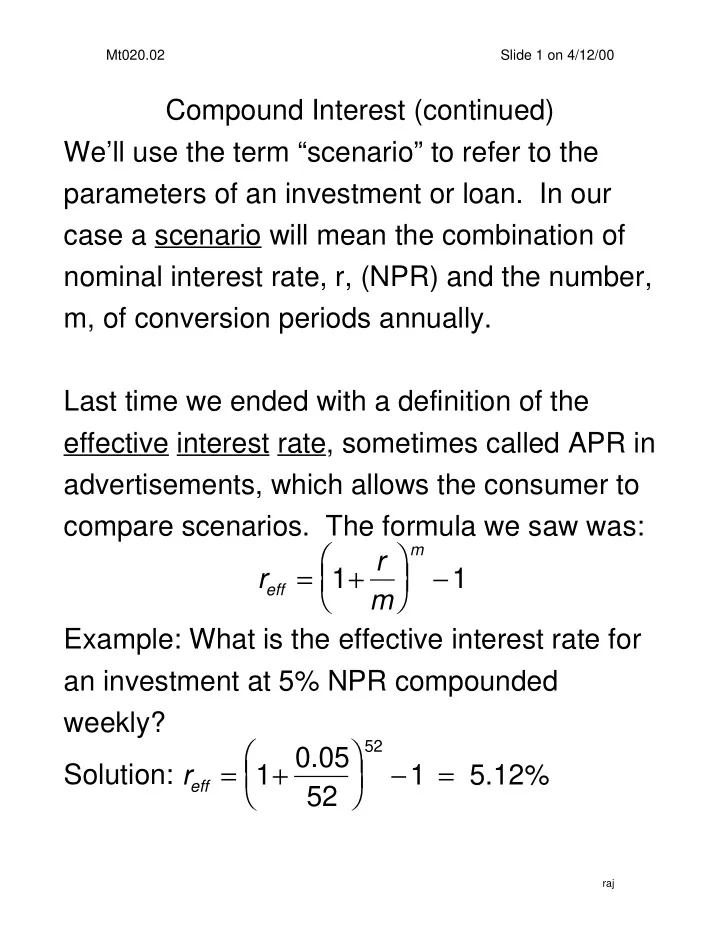

Mt020.02 Slide 1 on 4/12/00 Compound Interest (continued) Well use the term scenario to refer to the parameters of an investment or loan. In our case a scenario will mean the combination of nominal interest rate, r, (NPR) and the

Mt020.02 Slide 1 on 4/12/00

raj

Mt020.02 Slide 2 on 4/12/00

raj

Mt020.02 Slide 3 on 4/12/00

raj

Mt020.02 Slide 4 on 4/12/00

raj

Mt020.02 Slide 5 on 4/12/00

raj

Mt020.02 Slide 6 on 4/12/00

raj