SLIDE 1

11/19/2014 1

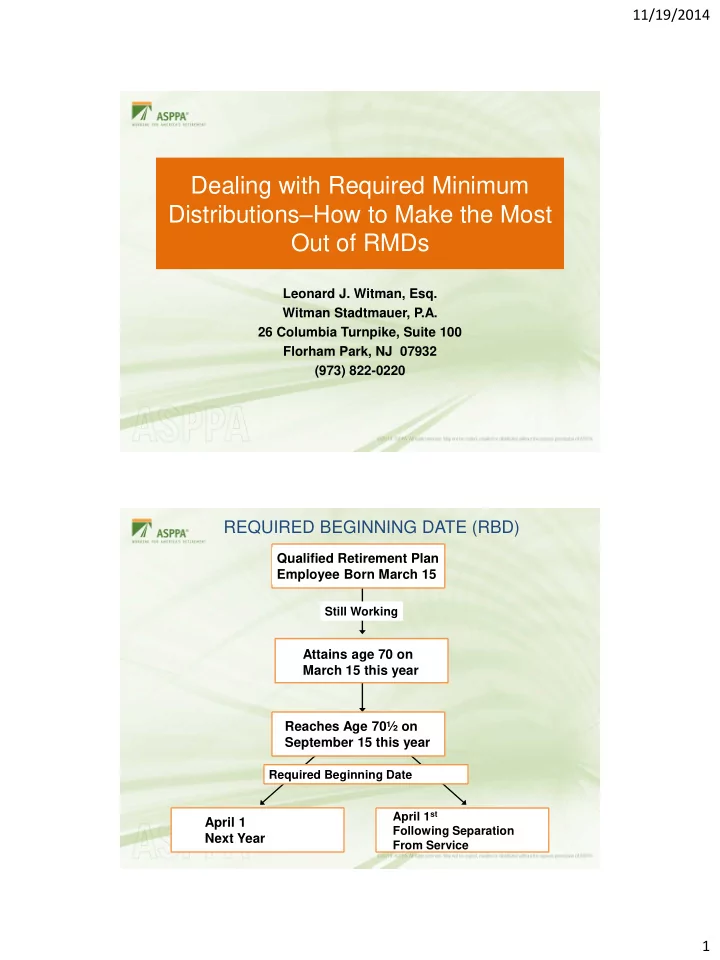

Dealing with Required Minimum Distributions–How to Make the Most Out of RMDs

Leonard J. Witman, Esq. Witman Stadtmauer, P.A. 26 Columbia Turnpike, Suite 100 Florham Park, NJ 07932 (973) 822-0220 Attains age 70 on March 15 this year Qualified Retirement Plan Employee Born March 15

REQUIRED BEGINNING DATE (RBD)

Reaches Age 70½ on September 15 this year

Still Working

April 1 Next Year

April 1st Following Separation From Service Required Beginning Date

SLIDE 2 11/19/2014 2

Calculation of Penalty 50% Excise Tax Prior Terminated Keogh Plan $100,000

First take $4,824 minimum distribution for current age 73 before end of year

RMDs not made for ages 70½ to 73

Profit Sharing Plan $119,102

RMD for age 73 - $4,824 50% Excise Tax on $12,039 not withdrawn (ages 70½ to 72) $6,020

$100,000

RMDs not made for: RMDs For past 3 years $12,039 Excise Tax x 50% Amount Due $ 6,020 $ 3,650 3,996 4,393 $12,039 Age 70½ Age 71 Age 72 Total

FAILURE TO COMMENCE DISTRIBUTIONS AT THE REQUIRED BEGINNING DATE

REQUIRED BEGINNING DATE - TAKING DISTRIBUTION AT AGE 70½ RATHER THAN DEFERRING UNTIL APRIL 1 OF THE FOLLOWING YEAR

1st Year Distribution Age 70 3.65% of $300,000, or $10,950 Tax Bracket 31% Scenario 1 One Distribution Each Year $22,639 Year 1 and 2 15,037 2nd Year Distribution Age 71 3.77% of $310,050 or $11,689 Tax Bracket 36% Cumulative Distributions Net After Tax

SLIDE 3

11/19/2014 3

1st Year Distribution Age 70 3.65% of $300,000, or $10,950 Tax Bracket 31%

Scenario 1 One Distribution Each Year

No Distribution This Year $23,412 Both in Year 2 14,984

Scenario 2 Two Distributions Second Year

2nd Year: Two Distributions First for age 70: 3.77% of $300,000 or $11,310 Second for Age 71: 3.77% of $321,000 or $12,102 Tax Bracket 36% $22,639 Year 1 and 2 15,037 2nd Year Distribution Age 71 3.77% of $310,050 or $11,689 Tax Bracket 36% Cumulative Distributions Net After Tax

REQUIRED BEGINNING DATE - TAKING DISTRIBUTION AT AGE 70½ RATHER THAN DEFERRING UNTIL APRIL 1 OF THE FOLLOWING YEAR

1st Year Distribution Age 70 3.65% of $300,000, or 10,950 Tax Bracket 36%

Scenario 1 One Distribution Each Year

$22,639 Year 1 and 2 $15,424 2nd Year Distribution Age 71 3.77% of $310,050 or $11,689 Tax Bracket 28% Cumulative Distributions Net After Tax

REQUIRED BEGINNING DATE - NO DISTRIBUTION AT AGE 70½ TWO DISTRIBUTIONS THE FOLLOWING YEAR

SLIDE 4 11/19/2014 4

1st Year Distribution Age 70 3.65% of $300,000, or 10,950 Tax Bracket 36%

Scenario 1 One Distribution Each Year

No Distribution This Year $23,412 Both in Year 2 $16,857

Scenario 2 Two Distributions Second Year

2nd Year: Two Distributions First for age 70: 3.77% of $300,000 or $11,310 Second for Age 71: 3.77% of $321,000 or $12,102 Tax Bracket 28% $22,639 Year 1 and 2 $15,424 2nd Year Distribution Age 71 3.77% of $310,050 or $11,689 Tax Bracket 28% Cumulative Distributions Net After Tax

REQUIRED BEGINNING DATE - NO DISTRIBUTION AT AGE 70½ TWO DISTRIBUTIONS THE FOLLOWING YEAR

Profit Sharing Plan Account Balance Profit Sharing Plan

Actual Withdrawal $18,250

Required Withdrawal 3.65% of $500,000

Required Minimum DISTRIBUTION FOR YEAR ONE $100,000 10% Yield CD IRA 1

Actual Withdrawal $0

Calculated Withdrawal $3,650 $50,000 7% Yield Mutual Fund IRA 2

Actual Withdrawal $0

Calculated Withdrawal $1,825 $50,000 2% Yield Money Market IRA 3

Actual Withdrawal $7,300

Calculated Withdrawal $1,825 Total Withdrawals $25,550 (3.65% of $700,000)

DISTRIBUTIONS AT AGE 70½ FROM A QUALIFIED PLAN AND SEVERAL INDIVIDUAL RETIREMENT ACCOUNTS

SLIDE 5

11/19/2014 5

Age of Employee 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 Distribution Period 27.4 26.5 25.6 24.7 23.8 22.9 22.0 21.2 20.3 19.5 18.7 17.9 17.1 16.3 15.5 14.8 Redetermined Applicable Percentage 3.65% 3.77% 3.91% 4.05% 4.20% 4.37% 4.55% 4.72% 4.93% 5.13% 5.35% 5.59% 5.85% 6.13% 6.45% 6.76%

LIFETIME REQUIRED MINIMUM DISTRIBUTIONS

Age of Employee 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 Distribution Period 14.1 13.4 12.7 12.0 11.4 10.8 10.2 9.6 9.1 8.6 8.1 7.6 7.1 6.7 6.3 5.9 Redetermined Applicable Percentage 7.09% 7.46% 7.87% 8.33% 8.77% 9.26% 9.80% 10.42% 10.99% 11.63% 12.35% 13.16% 14.08% 14.93% 15.87% 16.95%

LIFETIME REQUIRED MINIMUM DISTRIBUTIONS

SLIDE 6 11/19/2014 6

Age 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 Applicable Percentage 3.65% 3.77% 3.91% 4.05% 4.20% 4.37% 4.55% 4.72% 4.93% 5.13% 5.35% 5.59% 5.85% 6.13% 6.45% 6.76% Income (7%) 70,000 72,345 74,679 76,990 79,262 81,480 83,626 85,678 87,634 89,452 91,126 92,632 93,941 95,023 95,845 96,371 RMD (36,496) (39,000) (41,674) (44,529) (47,576) (50,830) (54,302) (57,735) (61,671) (65,532) (69,615) (73,928) (78,480) (83,281) (88,337) (93,022) Ending Balance 1,033,504 1,066,849 1,099,854 1,132,316 1,164,001 1,194,652 1,223,975 1,251,919 1,277,882 1,301,801 1,323,313 1,342,016 1,357,477 1,369,220 1,376,728 1,380,077 Beginning Balance $1,000,000 1,033,504 1,066,849 1,099,854 1,132,316 1,164,001 1,194,652 1,223,975 1,251,919 1,277,882 1,301,801 1,323,313 1,342,016 1,357,477 1,369,220 1,376,728

REQUIRED MINIMUM LIFETIME DISTRIBUTIONS AT AGE 70½ AND SUBSEQUENT IRA ROLLOVER BY SURVIVING SPOUSE

Distribution Period 27.4 26.5 25.6 24.7 23.8 22.9 22.0 21.2 20.3 19.5 18.7 17.9 17.1 16.3 15.5 14.8

SIGNIFICANCE OF DESIGNATED BENEFICIARY (DB) AND THE RBD FOR THE DB

The DB is the Individual that Inherits the IRA from the IRA Owner

DB Son

SLIDE 7 11/19/2014 7

THE DESIGNATED BENEFICIARY MUST BE FINALIZED BY SEPTEMBER 30 FOLLOWING THE YEAR OF THE IRA OWNER'S DEATH

RMD was taken Before He Died

IRA $1,000,000 DB Brother Names Daughter As Successor Beneficiary

Year Mr. K Died

No RMDs Paid to Brother RMD will be Paid on 12/30 DB (Brother) Dies on 8/1 Daughter is Successor Beneficiary

Year Following IRA Owner’s (Mr. K) Death

RMDs Based

Remaining 12.4 Year Life Expectancy Deceased Brother’s IRA

If Brothers are Classified as DB

Daughter’s Life Expectancy (36 Years) Used For RMDs

IRA Owner Brother’s Daughter Should in Effect Become DB

IRA Has Until 9/30 of Year Following IRA Owner’s Death to Finalize Determination of DB

Daughter is Successor Beneficiary

SLIDE 8 11/19/2014 8

THE ADVANTAGE OF INCLUDING CONTINGENT IRA BENEFICIARIES

At Her Death IRA Proceeds Payable to Her Estate

IRA

Estate

At Her Death Designated Beneficiary

IRA Son

If Mr. K (Sole DB) Predeceases Mrs. K (IRA Owner) and She Does Not Name a New DB If Mrs. K Had Named Her Son as Primary and Grandson as Secondary DBs

At Her Death IRA Proceeds Payable to

IRA

Estate

IRA Death Proceeds Paid to Primary Contingent Beneficiary

IRA Son

If there are No Contingent Beneficiaries and Mr. K Files a Qualified Disclaimer at Her Death Assume Mr. K Files Qualified Disclaimer at Her Death If Mrs. K Names Son as Primary and Grandson as Secondary DB

SLIDE 9 11/19/2014 9

Son is Next Beneficiary (Not DB)

For 20 Years Son will Receive RMDs For Remaining 4.4 years Rollover to

Age 60 $1,000,000 No RMDs From Mrs. K’s Age 60 to 70 Son, Age 51 is the DB Maximum duration of RMD Payout 33.3 Years (Life Expectancy at Age 51)

IRA At Mr. K’s Death If Mrs. K Is Outright DB RBD at age 70½ To death at age 80 Via Favorable Uniform Table IRA Remains in

QTIP Trust is Non-Spousal DB RBD in Year After Mr. K’s Death RMDs via 24.4 Year Fixed Period Life Expectancy for

If QTIP Trust Is DB

- Mrs. K’s death in 20 years - age 80

20 Years Until Mrs. K’s Death Next 10 Years First 10 Years

IRA STRETCH OUT VIA OUTRIGHT DISTRIBUTION TO SURVIVING SPOUSE VS. ACCUMULATION QTIP TRUST ARRANGEMENT

SINGLE LIFE EXPECTANCY TABLE V (SPOUSAL DB)

Used by Spousal Designated Beneficiary

Starting Age 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 Life Expectancy 34.2 33.3 32.3 31.4 30.5 29.6 28.7 27.9 27.0 26.1 25.2 24.4 23.5 22.7 21.8 Redetermined Applicable Percentage 2.92% 3.00% 3.10% 3.18% 3.28% 3.38% 3.48% 3.58% 3.70% 3.83% 3.97% 4.10% 4.26% 4.41% 4.59%

SLIDE 10 11/19/2014 10

Starting Age 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 Life Expectancy 21.0 20.2 19.4 18.6 17.8 17.0 16.3 15.5 14.8 14.1 13.4 12.7 12.1 11.4 10.8 10.2 Redetermined Applicable Percentage 4.76% 4.95% 5.15% 5.38% 5.62% 5.88% 6.13% 6.45% 6.76% 7.09% 7.46% 7.87% 8.26% 8.77% 9.26% 9.80%

SINGLE LIFE EXPECTANCY TABLE V (SPOUSAL DB)

Used by Spousal Designated Beneficiary

ELONGATED QUALIFIED PLAN DISTRIBUTION TECHNIQUES Summary

During Mr. K’s lifetime During son’s lifetime During grandson’s lifetime RMDs $ 900,044 5,325,818 9,290,013

SLIDE 11 11/19/2014 11

ELONGATED DISTRIBUTION PLANNING TECHNIQUES

At Mrs. K’s demise, the $1,878,823 account is inherited 2/3 by

- Mrs. K’s son ($1,252,549) and 1/3 by her grandson ($626,274).

RMDs will now be based on each beneficiary’s fixed period life expectancy in the year following Mrs. K’s death. Year 1 2

12 (year of death)

Age 70 71 74 79 81 IRA Beginning Balance $1,400,000 1,446,905 1,585,242 1,789,035 1,852,638 Uniform Table Life Expectancy 27.4 26.5

17.9 Total RMDs Applicable Percentage 3.65% 3.77% 4.20% 5.13% 5.59% RMD ($51,095) (54,600) (66,607) (91,745) (103,499) ($900,044) IRA Ending Balance 7% growth $1,446,905 1,493,588

1,878,823

Lifetime Distributions to Mrs. Kugler IRA 1 - At Mrs. K’s Death: payout to son for 34.2 year fixed period life expectancy

Year 1 2

30 35 Son’s Age 50 51 59 69 79 84 IRA Beginning Balance $1,252,549 1,303,603 1,731,568 2,125,376 1,540,459 124,103 Fixed Life Expectancy Table V 34.2 33.2

5.2 0.2 Total RMDs Applicable Percentage 2.92% 3.01% 3.97% 6.58% 19.23 100.00% RMD ($36,624) (39,265) (68,713) (139,827) (296,242) (132,790) ($5,325,818) IRA Ending Balance 7% Growth $1,303,603 1,355,590

1,352,049

SLIDE 12 11/19/2014 12

RMD ($10,597) (11,351) (19,695) (39,318) (78,830) (328,311) (135,897) ($9,290,013) Year 1 2

Grand- son’s Age 24 25 33 43 53 73 83 Fixed Life Expectancy Table V 59.1 58.1 50.1 40.1 30.1 10.1 0.1 Total RMDs Applicable Percentage 1.69% 1.72% 2.00% 2.49% 3.32% 9.90% 100.00% IRA Ending Balance 7% growth $659,517 694,331 1,036,118 1,647,715 2,460,063 3,219,744

IRA II - At Mrs. K’s Death: payout to grandson for 59.1 year fixed period life expectancy

IRA Beginning Balance $626,274 659,517 986,741 1,576,667 2,372,798 3,315,939 127,007

ANALYSIS OF STRETCH OUT IRAs (DEATH AFTER RBD)

At Mr. K’s death, Mrs. K will be owner and sole beneficiary Year 1 2

16 (year of death)

age 70 71 79 84 85 IRA Beginning Balance $1,000,000 1,033,5042 1,277,882 1,369,220 1,376,728 Uniform Table Life Expectancy 27.4 26.5

14.8 Total RMDs Applicable Percentage 3.65% 3.77% 5.13% 6.45% 6.76% RMD ($36,496) (39,000) (65,532) (88,337) (93,022) ($986,008) IRA Ending Balance 7% growth $1,033,504 1,066,849

1,380,077

Kugler Brother 1

Beneficiary: Mrs. K outright

SLIDE 13 11/19/2014 13 Kugler Brother 1

At Mr. K’s death; Mrs. K rolls over to IRA in her own name

At Mrs. K’s death, RMDs will be based on son’s fixed period life expectancy in year following Mrs. K’s death Year 1 2 3 4 5 6 7

age 79 80 81 82 83 84 85 IRA Beginning Balance $1,380,077 1,405,909 1,429,141 1,449,340 1,466,037 1,478,719 1,486,828 Uniform Table Life Expectancy 19.5 18.7 17.9 17.1 16.3 15.5 14.8 Total RMDs Applicable Percentage 5.13% 5.35% 5.59% 5.85% 6.14% 6.45% 6.76% RMD ($70,773) (75,182) (79,840) (84,757) (89,941) (95,401) (100,461) ($596,356) IRA Ending Balance 8% growth $1,405,909 1,429,141 1,449,340 1,466,037 1,478,719 1,486,828 1,490,445 Year 1 2

Son's age 50 51 59 69 79 84

Kugler Brother 1

At Mrs. K’s death; payout to son for 34.2 year fixed life expectancy

IRA Beginning Balance $1,490,445 1,551,195 2,060,444 2,529,947 1,833,037 147,674 Table V Fixed Life Expectancy 34.2 33.2 25.2 15.2 5.2 0.2 Total RMDs Applicable Percentage 2.92% 3.01% 3.97% 6.58% 19.23% 100% RMD (432,580) (46,723) (81,764) (166,385) (352,507) (158,011) ($6,337,349) IRA Ending Balance 8% growth $1,551,185 1,613,056 2,122,911 2,539,696 1,608,843 If son dies before 34.2 years, RMDs will continue to son’s designated beneficiary

SLIDE 14 11/19/2014 14

Year 1 2

16 (year of death)

age 70 71 79 84 85

Kugler Brother 2

Beneficiary: Conduit QTIP

IRA Beginning Balance $1,000,000 1,033,504 1,277,882 1,369,220 1,376,728 Uniform Table Life Expectancy 27.4 26.5

14.8 Total RMDs Applicable Percentage 3.65% 3.77% 5.13% 6.45% 6.76% RMD ($38,496) (39,000) (65,532) (88,337) (93,022) ($986,008) IRA Ending Balance 8% growth $1,033,504 1,066,849

1,380,077 At Mr. K’s death, Mrs. K will be recognized as sole designated beneficiary via Conduit QTIP (cannot roll over) Year 1 2 3 4 5 6 7

age 79 80 81 82 83 84 85

Kugler Brother 2

At Mr. K’s death; payout to Mrs. K via Conduit QTIP

IRA Beginning Balance $1,380,077 1,348,897 1,311,075 1,267,688 1,217,120 1,160,793 1,098,741 Applicable Percentage 9.26% 9.80% 10.31% 10.99% 11.63% 12.35% 13.16% RMD ($127,785) (132.245) (135,162) (139,306) (141,526) (143,308) (144,571) ($963,903) IRA Ending Balance 8% growth $1,348,897 1,311,075 1,267,688 1,217,120 1,160,793 1,098,741 1,031,081 At Mrs. K’s death, son is sole designated beneficiary. RMDs will be based on Mrs. K’s fixed period life expectancy in year of her death Table V Single Life Expectancy 10.8 10.2 9.7 9.1 8.6 8.1 7.6 Total RMDs

SLIDE 15 11/19/2014 15

Year 1 2 3 4 5 6 7 8 Son's age (not a factor)

Kugler Brother 2

At Mrs. K’s death; payout to son for 7.6 year fixed life expectancy

IRA Beginning Balance $1,031,081 967,588 888,715 792,226 675,459 535,114 366,759 163,208 Table V Fixed Life Expectancy 7.6 6.6 5.6 4.6 3.6 2.6 1.6 0.6 Total RMDs Applicable Percentage 13.16% 15.15% 17.86% 21.74% 27.78% 38.46% 62.59% 100% RMD ($135,669) (146,604) (158,699) (172,223) (187,627) (205,813) (229,224) (174,632) ($1,410,492) IRA Ending Balance 7% growth $967,588 888,715 792,226 675,459 535,114 366,759 163,208 (0) If son dies in less than 7.6 years, RMDs will continue to son’s designated beneficiary Year 1 2

16 (year of death)

age 70 71 79 84 85

Kugler Brother 3

Beneficiary: Accumulation QTIP

IRA Beginning Balance $1,000,000 1,033,504 1,277,882 1,369,220 1,376,728 Uniform Table Life Expectancy 27.4 26.5

14.8 Total RMDs Applicable Percentage 3.65% 3.77% 5.13% 6.45% 6.76% RMD ($36,496) (39,000) (65,532) (88,337) (93,022) ($986,008) At Mr. K’s death, Mrs. K will be oldest beneficiary, but not sole designated beneficiary RMDs will be based on Mrs. K’s fixed period life expectancy (not redetermined) in year following Mr. K’s death. IRA Ending Balance 7% growth $1,033,504 1,066,849

1,380,077

SLIDE 16

11/19/2014 16

Year 1 2 3 4 5 6 7 Beginning Balance $1,380,077 1,348,897 1,305,678 1,248,703 1,176,022 1,085,399 974,239 Total RMD paid to QTIP ($127,785) (137,643) (148,372) (160,090) (172,944) (187,138) (202,966) $(1,136,939) Ending Balance 1,348,897 1,305,678 1,248,703 1,176,022 1,085,399 974,239 839,469 At Mrs. K's death, the son is sole designated beneficiary. However, RMDs are now based on Mrs. K's remaining unused fixed period life expectancy in year of her death.

IRA

Kugler Brother 3

Accumulation QTIP at Mr. K’s death

Kugler Brother 3

Accumulation QTIP at Mr. K’s death

At Mrs. K's death, the son is sole designated beneficiary. However, RMDs are now based on Mrs. K's remaining unused fixed period life expectancy in year of her death. Year 1 2 3 4 5 6 7

QTIP

3% IRA Income to Mrs. K via QTIP ($41,402) (40,467) (39,170) (37,461) (35,281) (32,562) (29,227) ($255,570) Difference between RMD & 3% QTIP ($86,383) (97,176) (109,202) (122,629) (137,664) (154,576) (173,739) Cumulative after Tax (40%) difference ($51,830) (110,135) (175,656) (249,234) (331,832) (424,577) (528,821) 3% from prior year's QTIP balance to Mrs. K $0 (1,555) (3,304) (5,270) (7,477) (9,955) (12,737) ($40,298)

SLIDE 17

11/19/2014 17

Year 1 2 3 4 Beginning Balance $839,469 677,319 482,832 214,592 Total RMD paid to QTIP ($220,913) (241,900) (268,240) (265,777) ($996,830) Ending Balance $677,319 482,832 248,390

Kugler Brother 3

Accumulation QTIP at Mrs. K’s death; payout to son

IRA

Kugler Brother 3

Accumulation QTIP at Mrs. K’s death; payout to son

Year 1 2 3 4

QTIP

3% IRA Income to Mrs. K via QTIP ($25,184) (20,320) (14,485) (7,452) ($67,440) Difference between RMD & 3% QTIP ($195,729) (221,580) (287,553) (223,176) Cumulative after Tax (40%) difference ($646,258) (779,206) (951,738) (1,085,644) 3% from prior year's QTIP balance to Mrs. K ($15,865) (19,388) (23,376) (27,944) ($86,572)

SLIDE 18 11/19/2014 18

At Mr. K’s death, Mrs. K is the outright beneficiary of the IRA. Year 1 2

16 (year of death)

age 70 71 79 84 85 IRA Beginning Balance $1,000,000 1,033,504 1,277,882 1,369,220 1,376,728 Uniform Table Life Expectancy 27.4 26.5

14.8 Total RMDs Applicable Percentage 3.65% 3.77% 5.13% 6.45% 6.76% RMD ($36,496) (39,000) (65,532) (88,337) (93,022) ($986,008) IRA Ending Balance 7% growth $1,033,504 1,066,849

1,380,077

Kugler Brother 4

Beneficiary: Mrs. K (primary, deceased) Grandson (secondary)

Year 1 2 3 4 5 6 7

age 79 80 81 82 83 84 85 IRA Beginning Balance $1,380,077 1,405,909 1,429,141 1,449,340 1,466,037 1,478,719 1,486,828 Uniform Table Life Expectancy 19.5 18.7 17.9 17.1 16.3 15.5 14.8 Total RMDs Applicable Percentage 5.13% 5.35% 5.59% 5.85% 6.13% 6.45% 6.76% RMD ($70,773) (75,182) (79,840) (84,757) (89,941) (95,401) (100,461) ($596,356) IRA Ending Balance 7% growth $1,405,909 1,429,141 1,449,340 1,466,037 1,478,719 1,486,828 1,490,445

Kugler Brother 4

In year following Mr. K’s death, Mrs. K will roll IRA into her own name

SLIDE 19 11/19/2014 19

Year 1 10 20 30 40 50 54 Grand- son’s Age 30 39 49 59 69 79 83

Kugler Brother 4

At Mr. K’s Death: payout to grandson for 53.3 year fixed period single life expectancy

IRA Beginning Balance $1,490,445 2,305,431 3,571,389 5,092,612 6,108,868 3,929,373 482,183 Fixed Life Expectancy Table V 53.3 44.3 34.3 24.3 14.3 4.3 0.3 Applicable Percentage 1.88% 2.26% 2.92% 4.12% 6.99% 23.26% 100.00%

Total RMDs

RMD ($27,963) (52,041) (104,122) (209,573) (427,194) (913,808) (515,936) ($16,320,607) IRA Ending Balance 7% growth $1,566,812 2,414,769 3,717,264 5,239,523 6,109,295 3,290,622 If grandson dies before 53.3 years, RMDs will continue to the designated beneficiary.

Kugler Brother 1: Outright to Spouse

Years 16 7 34 57 During Mr. K’s lifetime During Mrs. K’s lifetime During son’s lifetime RMDs $986,008 596,356 6,337,349 $7,919,713 IRA Balance $1,380,077 1,490,445

SLIDE 20

11/19/2014 20

Kugler Brother 1: Outright to Spouse

Years 16 7 34 57 During Mr. K’s lifetime During Mrs. K’s lifetime During son’s lifetime RMDs $986,008 596,356 6,337,349 $7,919,713

Kugler Brother 2: Conduit QTIP

Years 16 7 8 31 RMDs $986,008 963,903 1,410,492 $3,360,403 During Mr. K’s lifetime During Mrs. K’s lifetime During Son’s lifetime IRA Balance $1,380,077 1,490,445 IRA Balance $1,380,077 1,031,081

Kugler Brother 3: Accumulation QTIP

Years 16 7 4 27 During Mr. K’s lifetime During Mrs. K’s lifetime During son’s lifetime Ending IRA Balance $1,380,077 839,469 3% Income via QTIP $0 255,570 67,440 $323,011 IRA & QTIP Balance $1,380,077 1,368,290 1,086,455 RMDs $986,008 1,136,939 996,830 $3,119,777

SLIDE 21 11/19/2014 21

Kugler Brother 3: Accumulation QTIP Kugler Brother 4: Outright to Spouse

Years 16 7 54 77 RMDs $986,008 596,356 16,320,607 $17,902,972 During Mr. K’s lifetime During Mrs. K’s lifetime During Grandson’s lifetime IRA Balance $1,380,077 1,490,445 Years 16 7 4 27 RMDs $986,008 1,136,939 996,830 $3,119,777 During Mr. K’s lifetime During Mrs. K’s lifetime During son’s lifetime Ending IRA Balance $1,380,077 839,469 3% Income via QTIP $0 255,570 67,440 $323,011 IRA & QTIP Balance $1,380,077 1,368,290 1,086,455

$250,000 IRA

$1,000,000 Plus $250,000 Rollover Rollover to

Transfer $250,000 IRA Balance to 401(k) During Mr. K’s Lifetime

THE DIFFERENCE BETWEEN A QRP AND IRA DEATH BENEFIT PAYABLE TO A NON-SPOUSAL DB WITH RESPECT TO A ROTH CONVERSION

Direct Transfer

To New Separate IRA for Son

At Mr. K’s Death

$1,250,000 401(k)

$1,250,000 to Roth IRA Son DB

SLIDE 22 11/19/2014 22

$250,000 IRA

$1,000,000 Plus $250,000 Rollover Convert to Roth Income Tax Paid by Mr. K

Transfer $250,000 IRA Balance to Roth IRA During Mr. K’s Lifetime Transfer $250,000 IRA Balance to Roth IRA

$250,000 Roth IRA

$250,000 to Roth IRA Payable to Son Direct Transfer to Direct Transfer Income Tax Paid by Son

At Mr. K’s Death

$1,000,000 401(k)

$1,000,000 to Roth IRA Son DB

SLIDE 23 11/19/2014 23

KAY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION

Difference Between Roth and Traditional IRA

Traditional IRA -- The contributions are tax deductible up to specified amounts (a maximum of $5,000 plus an additional $1,000 if over age 50). Contributions are not allowed after the Required Beginning Date (RBD), age 70½. The values accumulate on an income tax-deferred basis. Roth IRA -- The contributions are permitted up to the same specific

- amounts. The contributions are not tax deductible and may be made

after age 70½. The values accumulate on an income tax-free basis. There is no RBD and thus no RMDs applicable to the IRA owner (including a surviving spouse that implements a Roth IRA rollover). RMDs to the DB commence in the year following the death of the Roth IRA owner. Distributions (lifetime or death) are not subject to income tax to the Roth IRA owner and/or successor beneficiaries.

When Reviewing Primary Factors the Following Should Be Considered:

There is no income test applicable and any IRA owner can convert. One primary factor in determining the viability of a Roth conversion is the number of years the IRA funds will accumulate before distributions

- commence. The duration of the accumulation period for the IRA owner

is of paramount importance. The duration and subsequent payout to the DB must also be factored into the ultimate accumulation period. The factors that impact the duration of the IRA payout for the IRA owner must also be considered for the DB.

SLIDE 24

11/19/2014 24

When Reviewing Primary Factors the Following Should Be Considered:

In certain situations a participant in a Qualified Plan (QRP) may convert his/her account balance to a Roth IRA. Generally, in order to implement the IRA conversion the following requirements may be applicable: 1) spousal consent may be required, 2) the QRP must provide for a lump sum distribution, 3) the plan participant must have separated from service and/or attained retirement age.

THE FOLLOWING IS A BRIEF REVIEW OF THE PRIMARY FACTORS:

Splitting the IRA in to multiple IRAs prior to the Roth conversion. Using outside funds to pay the income tax on a Roth conversion rather than liquidating a portion of the existing IRA. Does the IRA owner or surviving spouse need the IRA for retirement purposes? Anticipated number of years before RMDs for IRA owner and/or the DB. Will a lump sum distribution or RMDs be applicable to the IRA owner and/or DB? Current income tax bracket. Pre and post-retirement income tax bracket.

SLIDE 25

11/19/2014 25

THE FOLLOWING IS A BRIEF REVIEW OF THE PRIMARY FACTORS (continued):

The current amount in the traditional IRA. Estate tax situation. State income tax. Special considerations for state laws applicable to IRAs. Partial Roth conversion of an IRA asset that has substantial growth potential in the near future. Charitable contribution by the IRA owner.

THE FOLLOWING IS A BRIEF REVIEW OF THE PRIMARY FACTORS (continued):

Using the IRA to fund a credit shelter trust. Portion of Social Security retirement income included in AGI. Medicare premiums. Pre-Age 59½ distributions and the Roth five-year rule. Community property states. Summary