SLIDE 1

1

Changes in global shipping and long-distance rail networks: possible impacts on hub port Singapore

Theo Notteboom

Foreign Expert/Full Professor, Dalian Maritime University, China Professor, ITMMA - University of Antwerp, Belgium Professor, Antwerp Maritime Academy, Belgium Council member and immediate past President, International Association of Maritime Economists (IAME) Co-Director Port Economics.eu

MPA Visiting Professor Public Lecture NTU - School of Civil & Environmental Engineering Singapore - February 5, 2015

2

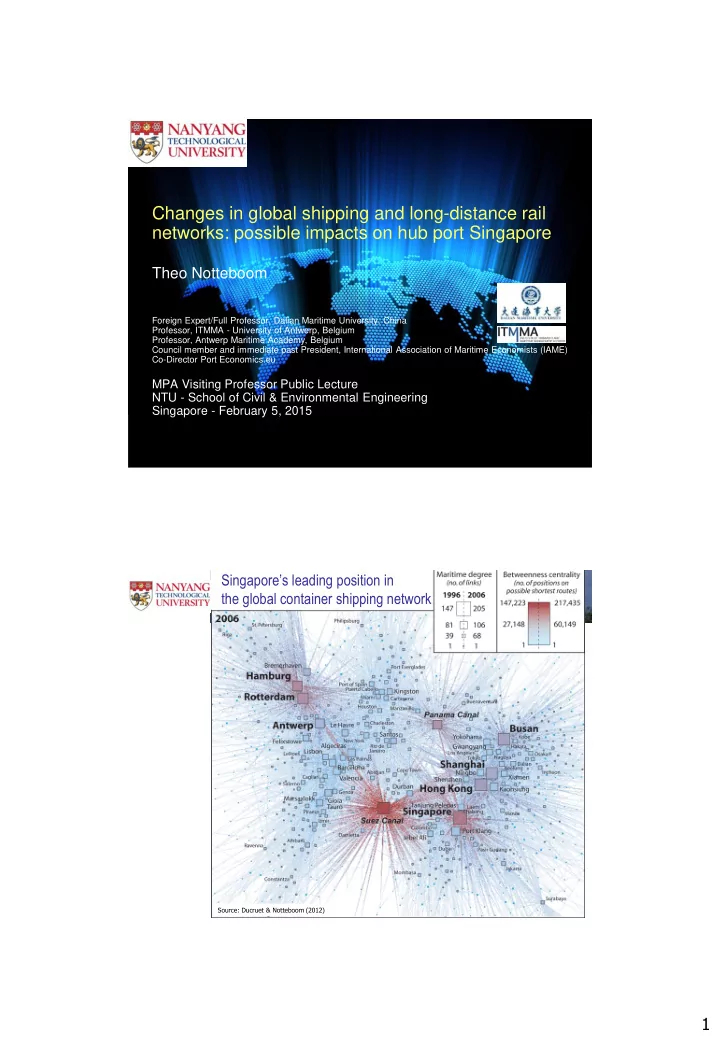

Source: Ducruet & Notteboom (2012)