SLIDE 1

CHI-FRB Indy June 10, 2009

ECONOMIC OUTLOOK

Weathering the Storm

Timothy Slaper, Ph.D. Director of Economic Research Indiana Business Research Center Kelley School of Business, Indiana University

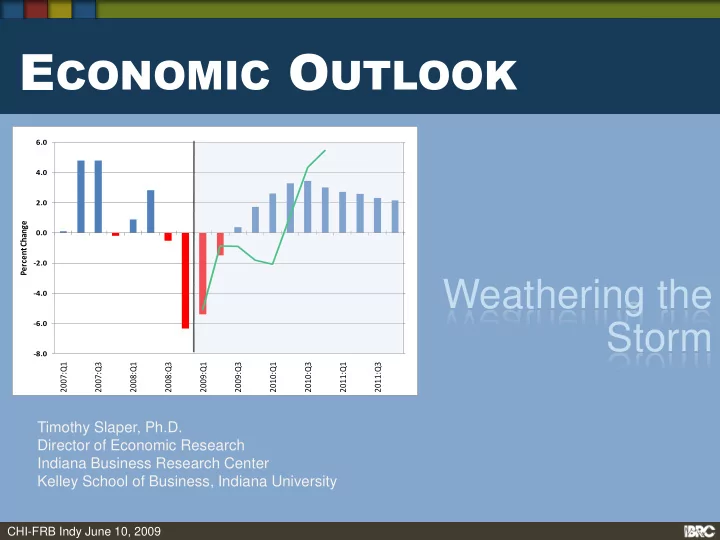

- 8

- 6

- 4

- 2

2 4 6

- 8.0

- 6.0

- 4.0

- 2.0

0.0 2.0 4.0 6.0

2007:Q1 2007:Q3 2008:Q1 2008:Q3 2009:Q1 2009:Q3 2010:Q1 2010:Q3 2011:Q1 2011:Q3 Percent Change