SLIDE 1

1

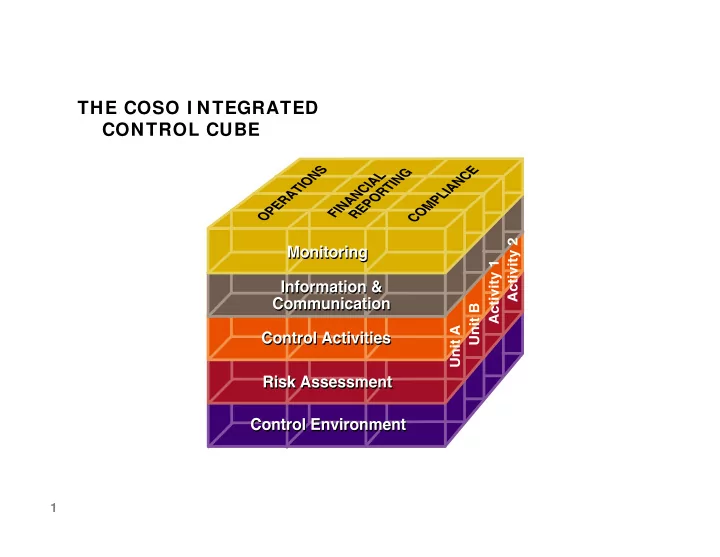

THE COSO INTEGRATED CONTROL CUBE THE COSO I NTEGRATED CONTROL CUBE - - PowerPoint PPT Presentation

THE COSO INTEGRATED CONTROL CUBE THE COSO I NTEGRATED CONTROL CUBE 1 COSO Definition of I nternal Control Internal control is a process, effected by an entitys Board of Directors, management and other personnel, designed to provide

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16