SLIDE 19 19

Analysis: Adoption curves are not linear, they are exponential

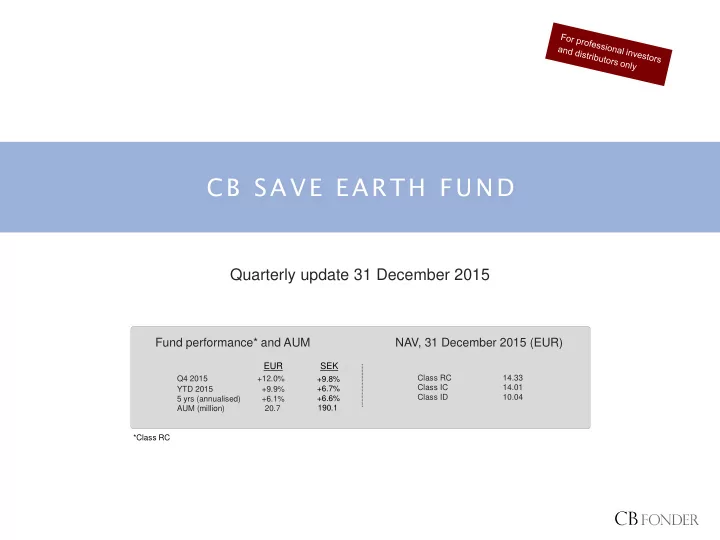

C B S A V E E A R T H F U N D

Source: Bernstein Research, CB Fonder

The price of solar energy (real, in $/MMBTU) has fallen sharply during the last years

figure illustrates the price development of the five different types of energy: Natural gas ("Henry Hub"), coal ("US Bitumous Coal"),

("Brent"), liquefied natural gas ("LNG") and solar energy ("solar").

- The price of solar energy has in recent

years fallen sharply and is now a competitive alternative to

more established forms of energy.

energy market is becoming technology-based, which implies that higher demand gives lower prices (comp. Moore’s law). A new world order...

- Most adoption curves are so-called S-

curves, which implies exponential rather than linear growth. When the new technology reaches 10% market share it’s game

the new technology substitutes the old one.

- Solar and wind currently accounts for a

small fraction of the global energy market (1.6%), but the proportion has increased 8x in 10 years. What is interesting is that solar and wind today represents more than 20% of the new capacity installed globally. Renewable energy is still marginal, but it begins to have a significant impact on the margin.

Solar and wind, percentage of the global energy market Adoption curves for colour TVs

% Source: Technology Futures, Inc Source: Bernstein Research, CB Fonder Source: Bernstein Research, CB Fonder