SLIDE 1

1

Corporate Finance

Project Evaluation

Javier Estrada Spring, 2014

- 1. Tools

- Net Present Value (NPV)

- Internal Rate of Return (IRR)

- Shortcomings of the IRR

- 2. Further Analysis

- Sensitivity analysis

- One or more discount rates?

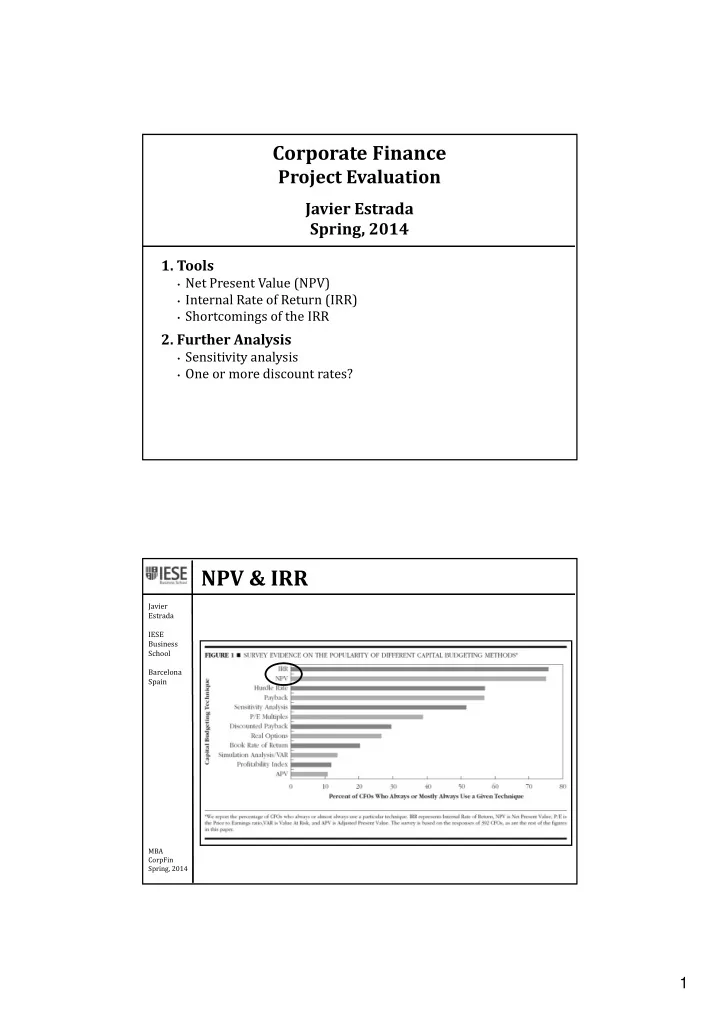

Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014