SLIDE 1

1

Emerging Markets (IV):

Project Evaluation

Javier Estrada ADFIN – Winter/2014

- 1. Expected Cash Flows and Discount Rates

- Expected cash flows and issues

- Models and discount rates

- 2. Evaluation

- NPV and IRR

- Sensitivity analysis

Javier Estrada IESE Business School Barcelona Spain ADFIN Winter/2014

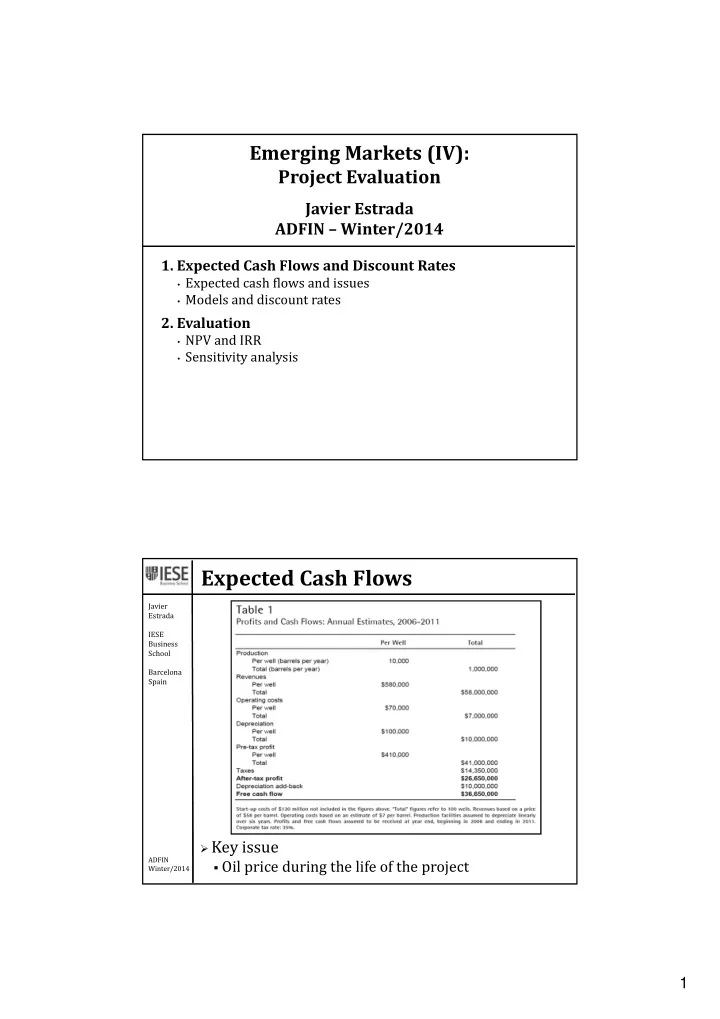

Expected Cash Flows

- Key issue

- Oil price during the life of the project