SLIDE 1

Institute For New Economic Thinking

Too Much of the Wrong Sort of Capital Flow ¡|1 ¡

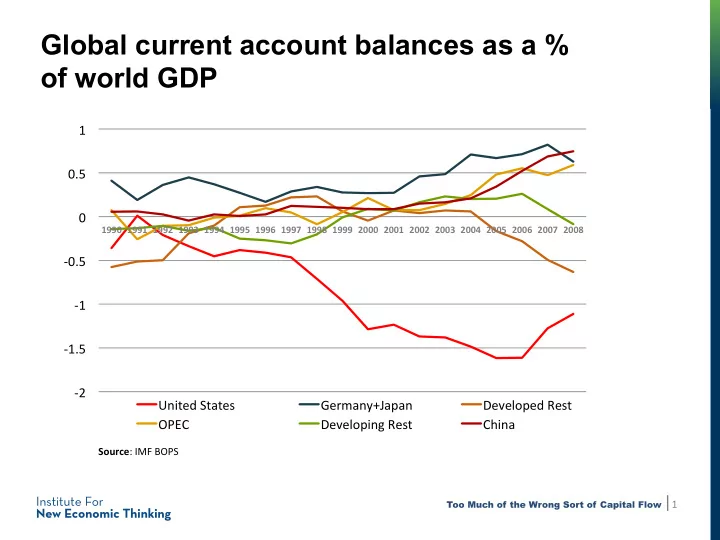

Global current account balances as a %

- f world GDP

- ‑2 ¡

- ‑1.5 ¡

- ‑1 ¡

- ‑0.5 ¡

0 ¡ 0.5 ¡ 1 ¡

1990 ¡ 1991 ¡ 1992 ¡ 1993 ¡ 1994 ¡ 1995 ¡ 1996 ¡ 1997 ¡ 1998 ¡ 1999 ¡ 2000 ¡ 2001 ¡ 2002 ¡ 2003 ¡ 2004 ¡ 2005 ¡ 2006 ¡ 2007 ¡ 2008 ¡

United ¡States ¡ Germany+Japan ¡ Developed ¡Rest ¡ OPEC ¡ Developing ¡Rest ¡ China ¡ ¡

Source: ¡IMF ¡BOPS ¡