SLIDE 1

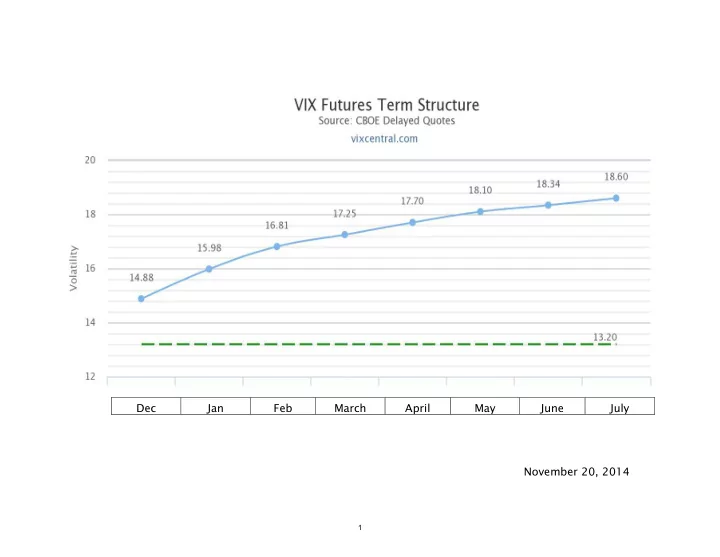

Dec Jan Feb March April May June July November 20, 2014

1

Dec Jan Feb March April May June July November 20, 2014 1 VIX - - PowerPoint PPT Presentation

Dec Jan Feb March April May June July November 20, 2014 1 VIX Futures Historical Prices August 1, 2011 August 8, 2011 40 35 30 Volatility 25 20 15 0 30 60 90 120 150 180 210 Days to

1

2

Credit Suisse

3

4