Slide

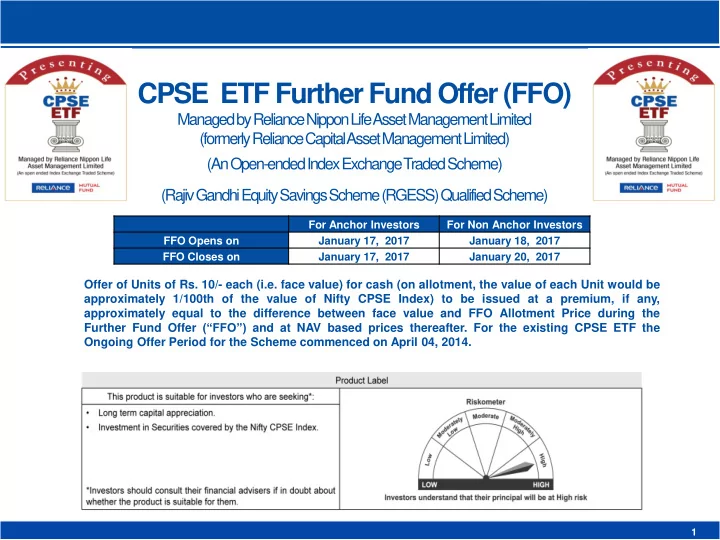

CPSE ETF Further Fund Offer (FFO)

Managed by Reliance Nippon Life Asset Management Limited (formerly Reliance Capital Asset Management Limited) (An Open-ended Index Exchange Traded Scheme) (Rajiv Gandhi Equity Savings Scheme (RGESS) Qualified Scheme)

For Anchor Investors For Non Anchor Investors FFO Opens on January 17, 2017 January 18, 2017 FFO Closes on January 17, 2017 January 20, 2017

Offer of Units of Rs. 10/- each (i.e. face value) for cash (on allotment, the value of each Unit would be approximately 1/100th of the value of Nifty CPSE Index) to be issued at a premium, if any, approximately equal to the difference between face value and FFO Allotment Price during the Further Fund Offer (“FFO”) and at NAV based prices thereafter. For the existing CPSE ETF the Ongoing Offer Period for the Scheme commenced on April 04, 2014.

1