SLIDE 1 Chart 1

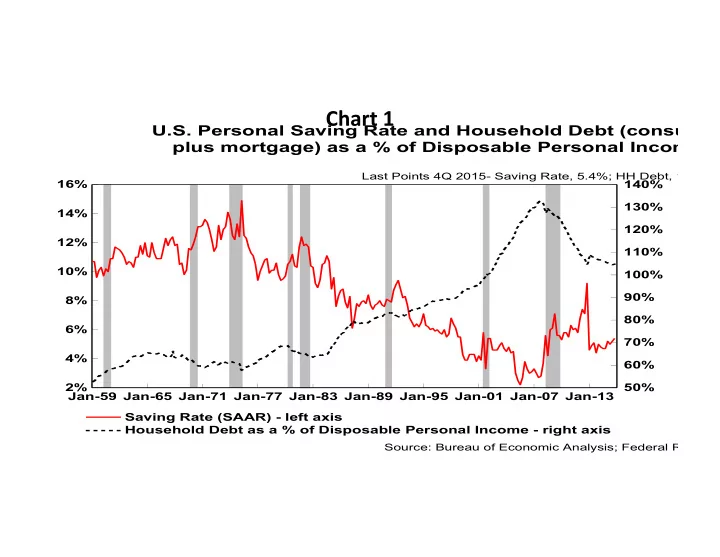

Jan-59 Jan-65 Jan-71 Jan-77 Jan-83 Jan-89 Jan-95 Jan-01 Jan-07 Jan-13 2% 4% 6% 8% 10% 12% 14% 16% 50% 60% 70% 80% 90% 100% 110% 120% 130% 140% Saving Rate (SAAR) - left axis Household Debt as a % of Disposable Personal Income - right axis

U.S. Personal Saving Rate and Household Debt (consumer plus mortgage) as a % of Disposable Personal Income

Last Points 4Q 2015- Saving Rate, 5.4%; HH Debt, 104.7% Source: Bureau of Economic Analysis; Federal Reserve

SLIDE 2 Chart 2

Real GDP Growth During Expansions

annualized rates of expansion from NBER trough-to-peak

*Through 1Q 2016 Source: BEA, NBER

7.6% 4.0% 5.6% 4.9% 5.1% 4.3% 4.4% 4.3% 3.6% 2.8% 2.1%* 1950 1954 1958 1961 1971 1975 1980 1983 1991 2002 2009 0% 1% 2% 3% 4% 5% 6% 7% 8% 0% 1% 2% 3% 4% 5% 6% 7% 8%

Recession Start Date

SLIDE 3 Chart 3

Eurozone Real GDP Growth

Source: eurostat Last Point 1Q 2016: Q/Q, 2.2%; Y/Y, 1.6%

2007 2008 2009 2010 2011 2012 2013 2014 2015

- 12.0%

- 10.0%

- 8.0%

- 6.0%

- 4.0%

- 2.0%

0.0% 2.0% 4.0% 6.0%

- 12.0%

- 10.0%

- 8.0%

- 6.0%

- 4.0%

- 2.0%

0.0% 2.0% 4.0% 6.0% quarter/quarter % change, seas. adj. annual rates year/year % change

SLIDE 4 Chart 4

Japanese Real GDP Growth

Source: Japanese Cabinet Office Last Points 4Q 2015: Q/Q, -1.1%; Y/Y, 0.8%

2007 2008 2009 2010 2011 2012 2013 2014 2015

0% 5% 10% 15%

0% 5% 10% 15% quarter/quarter % change, seas. adj. annual rates year/year % change

SLIDE 5 Chart 5

Jan-07 Sep-08 May-10 Jan-12 Sep-13 May-15

0% 50% 100% 150% 200% 250% 300% 350% 400% 450%

0% 50% 100% 150% 200% 250% 300% 350% 400% 450% Federal Reserve European Central Bank Bank of England Bank of Japan

Central Bank Assets

change since January 2007

Source: Bloomberg; The Central Banks Last Points: April 2016

SLIDE 6

Chart 6

Jan-07 Dec-08 Dec-10 Dec-12 Dec-14 600 800 1000 1200 1400 1600 1800 2000 2200 600 800 1000 1200 1400 1600 1800 2000 2200

S&P 500 Index

Source: Thomson Reuters Last Point 05/12/16: 2,064.11

SLIDE 7 Chart 7

2010 2011 2012 2013 2014 2015 2016 2017 2018 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% Actual Real GDP 2011 2012 2013 2014 2015

Historical Fed Committee Forecasts for Real GDP Growth

based on central tendency midpoint forecast at first FED meeting of the year

Source: Federal Reserve Note: Longer run forecast used for 2018 forecast made in 2015.

SLIDE 8 Chart 8

1947-I 1959-III 1972-I 1984-III 1997-I 2009-III 58% 59% 60% 61% 62% 63% 64% 65% 66% 67% 68% 7% 8% 9% 10% 11% 12% 13% 14% 15% Compensation of Employees - left axis

- Corp. Profits with IVA and CCAdj - right axis

Corporate Profits and Employee Compensation as a percentage of National Income

Source: Bureau of Economic Analysis Last Points 4Q 2015 - Corp. Profits: 12.1%, Employee Comp: 62.6%

SLIDE 9 Chart 9

1980 1985 1990 1995 2000 2005 2010

0% 1% 2% 3% 4%

0% 1% 2% 3% 4%

- Avg. Real Weekly Wages of Production and Supervisory Employees

Real Median Household Income

Real Weekly Wages and Household Incomes

year/year percent changes

Source: Bureau of Labor Statistics; Census Bureau Last Points 2014- Income: -1.5%, Wages: 1.0%

SLIDE 10

Chart 10

Jan-48 Jan-57 Jan-66 Jan-75 Jan-84 Jan-93 Jan-02 Jan-11 58% 59% 60% 61% 62% 63% 64% 65% 66% 67% 68% 58% 59% 60% 61% 62% 63% 64% 65% 66% 67% 68%

Labor Force Participation Rate

Source: Bureau of Labor Statistics Last Point April 2016: 62.8%

SLIDE 11 Chart 11

Retail Sales

retail trade and food services

Source: U.S. Census Bureau Last Point April 2016: M/M, 1.3%; Yr/Yr, 3.0%

Jan-15 Mar-15 May-15 Jul-15 Sep-15 Nov-15 Jan-16 Mar-16

0.0% 0.5% 1.0% 1.5%

0.0% 1.0% 2.0% 3.0% 4.0% Month/Month Percent Change - left axis Year/Year Percent Change - right axis

SLIDE 12

Chart 12

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 4% 6% 8% 10% 12% 14% 16% 4% 6% 8% 10% 12% 14% 16%

Chinese Real Gross Domestic Product

year/year percent change

Last Point 1Q 2016: 6.7% Source: Bloomberg; Chinese National Bureau of Statistics

SLIDE 13 Chart 13

Jan-07 Sep-08 May-10 Jan-12 Sep-13 May-15

0% 10% 20% 30% 40% 50% 60%

0% 10% 20% 30% 40% 50% 60%

Chinese Exports

year/year percent change

Source: China General Administration of Customs Last Point April 2016: -1.8%

SLIDE 14

Chart 14

2004 2006 2008 2010 2012 2014 150% 160% 170% 180% 190% 200% 210% 220% 230% 240% 250% 150% 160% 170% 180% 190% 200% 210% 220% 230% 240% 250%

Chinese Total Debt as a Share of GDP

includes corporate, household, government and bank debt

Source: Bloomberg Last Point 2015: 246.8%

SLIDE 15 Chart 15

1997 1999 2002 2004 2007 2009 2012 2014 11.5% 12.0% 12.5% 13.0% 13.5% 14.0% 14.5% 15.0% 15.5% 16.0% 16.5% 17.0% 11.5% 12.0% 12.5% 13.0% 13.5% 14.0% 14.5% 15.0% 15.5% 16.0% 16.5% 17.0%

United States Manufacturing Value Added

as % share of GDP

Source: Bureau of Economic Analysis; The World Bank Last Point 4Q 2015: 12.0%

SLIDE 16

Chart 16

G7 and BRIC Personal Consumption to GDP Ratio: 2014

68.6% 64.7% 62.5% 61.1% 61.1% 59.3% 55.9% 55.8% 55.5% 53.0% 36.5% 30% 35% 40% 45% 50% 55% 60% 65% 70% 75% U.S. U.K. Brazil Japan Italy India Germany Canada France Russia China

Source: The World Bank

SLIDE 17

Chart 17

Jan-15 Mar-15 May-15 Aug-15 Oct-15 Dec-15 Mar-16 150 160 170 180 190 200 210 220 230 240 25 30 35 40 45 50 55 60 65 CRB Index - left axis WTI Crude Oil (dollars per barrel) - right axis

Reuters/Jeffries CRB Index and WTI Crude Oil

Source: Thomson Reuters Last Points 05/12/16- CRB: 184.39; WTI: $46.70

SLIDE 18 Chart 18

Jan-07 Sep-08 May-10 Jan-12 Sep-13 May-15 20 40 60 80 100 120 140 160 180 200 5000 10000 15000 20000 25000 30000 35000 40000 45000 50000 Iron Ore - left axis Nickel - right axis

Iron Ore and Nickel

$ per tonne

Source: Thomson Reuters; Bloomberg Last Point 05/12/16: Iron Ore, $54.50; Nickel, $8,775

SLIDE 19

Chart 19

1774 1814 1854 1894 1934 1974 2014 200 400 600 800 1000 1200 1400 200 400 600 800 1000 1200 1400

Real U.S. Commodity Prices

CRB Index Deflated by CPI

Source: Bianco Research, Bureau of Labor Statistics, Historical Statistics of the Un Last Point March 2016: 72.15

SLIDE 20 Chart 20

Mar-07 Jun-08 Sep-09 Dec-10 Mar-12 Jun-13 Sep-14 Dec-15

0% 5% 10%

0% 5% 10% Brazil GDP Russia GDP

Brazil and Russia Real GDP Growth

year/year percent change

Source: Brazil Institute of Geography and Statistics; Bloomberg Last Points 4Q 2015: Brazil, -5.9%; Russia, -3.8%

SLIDE 21

Chart 21

1996 1998 2001 2003 2006 2008 2011 2013 25 30 35 40 45 50 55 60 25 30 35 40 45 50 55 60 Non-OPEC OPEC

Total Oil Output for Non-OPEC and OPEC Countries

million barrels per day

Source: Energy Information Administration Last Points 3Q 2015 - Non-OPEC: 58.68; OPEC: 37.71

SLIDE 22

Chart 22

United States Crude Oil Production

million barrels per day

Source: Energy Information Administratio Last Points 05/6/16: 8.80

2000 2001 2002 2004 2005 2006 2008 2009 2010 2012 2013 2014 1 2 3 4 5 6 7 8 9 10 1 2 3 4 5 6 7 8 9 10

SLIDE 23 Chart 23

Crude Oil Rotary Rig Count and Average Oil Production Per Rig

Source: Bloomberg; Baker Hughes Last Points April 2016: Rigs, 372; Oil Prod., 475

2008 2009 2010 2011 2012 2013 2015 200 400 600 800 1000 1200 1400 1600 50 100 150 200 250 300 350 400 450 500 Rig Count - left axis Average Oil Production Per Rig (barrels/day) - right axis

SLIDE 24 Chart 24

Oil Breakeven Price for Major Petrostates

$ per barrel

Source: Bloomberg; The Wall Street Journal

$52 $58 $68 $70 $76 $89 $93 $96 $98 $105 $208 Kuwait Qatar U.A.E. Iran Iraq Venezuela Algeria Saudi Arabia Oman Bahrain Libya $0 $50 $100 $150 $200 $250 $0 $50 $100 $150 $200 $250 *Breakeven price needed in order to balance the national budget.

Current Brent Crude, $/barrel: $48.08

SLIDE 25 Chart 25

OPEC Oil Output By Country

million barrels per day

Source: Bloomberg Last Point: April 2016

10.3 4.3 3.5 3.0 2.9 2.4 1.8 1.7 1.1 0.7 0.7 0.6 0.3 Saudi Arabia Iraq Iran U.A.E. Kuwait Venezuela Angola Nigeria Algeria Indonesia Qatar Ecuador Libya 2 4 6 8 10 12 2 4 6 8 10 12

SLIDE 26 Chart 26

2001 2002 2004 2006 2007 2009 2011 2012 2014 2016 100 200 300 400 500 600 700 800 100 200 300 400 500 600 700 800

Saudi Arabia Foreign Exchange Reserves

billion USD

Source: Bloomberg; International Monetary Fund Last Point March 2016: $587.08

SLIDE 27 Chart 27

A Successful Cartel

1. Involves a commodity that can otherwise be left in the ground, avoiding production and inventory costs until it’s needed.

- 2. Its product is so much in demand that buyers are relatively insensitive to price.

- 3. The commodity has few if any close substitutes.

- 4. It includes most of the low-cost suppliers and has few meaningful non-cartel competitors.

- 5. It involves relatively few cartel members, thereby promoting discipline.

6. It's sponsored by governments and even religious authorities that benefit from the cartel and protect it.

- 7. It operates in a period of strong economic growth and robust demand for the product.

- 8. It faces few technological improvements in the industry.

SLIDE 28 Chart 28

Unfavorable Climate for OPEC

1. Alternatives to oil, especially natural gas but also government-subsidized renewables, are growing.

- 2. Non-OPEC supplies are leaping, notably from Russia and especially American frackers.

- 3. Infighting among OPEC members has destroyed discipline.

- 4. Global economic growth is weak, and the ongoing shift from goods production to services in

China and elsewhere is curbing oil demand.

- 5. Conservation is limiting oil demand.

- 6. Rapid technological advances in fracking, horizontal drilling, deep-water and Arctic drilling, etc.

are mushrooming non-OPEC supplies at low and declining costs.

SLIDE 29 Chart 29

Annual Average Oil Demand for OECD and Non-OECD Countries

million barrels per day

Source: The Wall Street Journal; Bloomberg Last Points 2015: OECD, 46.39; Non-OECD, 48.28

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 10 20 30 40 50 60 10 20 30 40 50 60 OECD Non-OECD

SLIDE 30 Chart 30

World Crude Oil Supply and Demand

million barrels per day

Source: Bloomberg; International Energy Agency Last Points 4Q 2015: Ex. Supply, 1.7; Demand, 95.5; Suppl

2001 2002 2003 2004 2006 2007 2008 2009 2011 2012 2013 2014

0.0 0.5 1.0 1.5 2.0 2.5 75 80 85 90 95 100 Excess Supply - left axis Demand - right axis Supply - right axis

SLIDE 31 Chart 31

Commercial Crude Oil Inventory

weekly U.S. ending stocks

Source: Energy Information Administratio Last Points 05/6/16: Inventory: 539.9; Yr/Yr: 10.9%

Jan-14 Apr-14 Aug-14 Dec-14 Mar-15 Jul-15 Nov-15 200 250 300 350 400 450 500 550

0% 5% 10% 15% 20% 25% 30% Crude Oil Inventory (million barrels) - left axis Year/Year Percent Change - right axis

SLIDE 32 Chart 32

Mar-11 Oct-11 May-12 Dec-12 Jul-13 Feb-14 Sep-14 Apr-15 Nov-15 20% 30% 40% 50% 60% 70% 80% 90% 20% 30% 40% 50% 60% 70% 80% 90% Tank Net Available Shell Storage Capacity Utilization Tank Working Storage Capacity Utilization

Crude Oil Storage Capacity Utilization

Cushing, OK

Source: Energy Information Administratio Last Points 05/6/16: Shell, 77.3%; Working, 92. Note: Net available shell includes idle (not working) capacity.

SLIDE 33

Chart 33

Jun-16 Feb-18 Oct-19 Jun-21 Feb-23 Oct-24 46 48 50 52 54 56 58 46 48 50 52 54 56 58

Source: Bloomberg

WTI Crude Oil Futures Curve

05/12/16 close prices; dollars per barrel

SLIDE 34 Chart 34

Total Crude Oil Storage in Amsterdam-Rotterdam-Antwerp Region

million barrels

Source: Bloomberg Last Point 05/6/2016: 55.79

Feb-13 Jun-13 Oct-13 Feb-14 Jun-14 Oct-14 Jan-15May-15Sep-15 Jan-16 40 45 50 55 60 65 40 45 50 55 60 65

SLIDE 35 Chart 35

Jan-15 Mar-15 May-15 Jul-15 Oct-15 Dec-15 Feb-16 May-16 6.15 6.20 6.25 6.30 6.35 6.40 6.45 6.50 6.55 6.60 6.15 6.20 6.25 6.30 6.35 6.40 6.45 6.50 6.55 6.60

Chinese Yuan Per U.S. Dollar

Source: Bloomberg Last Point 05/12/16: 6.514

Stronger U.S. Dollar

08/11/15: People's Bank of China lowers yuan reference rate

Stronger U.S. Dollar

SLIDE 36 Chart 36

Chinese Trade Balance and Capital Flow

billion USD

Source: Bloomberg Last Points 03/16: Cap. Flow, -$44.3; 04/16: Balance, $45.56

Jan-10 Sep-10 May-11 Jan-12 Sep-12 May-13 Jan-14 Sep-14 May-15

50 100 150

10 30 50 70 Monthly Capital Flow - left axis Trade balance - right axis

SLIDE 37

Chart 37

Jan-00 Sep-01 May-03 Jan-05 Sep-06 May-08 Jan-10 Sep-11 May-13 Jan-15 500 1000 1500 2000 2500 3000 3500 4000 500 1000 1500 2000 2500 3000 3500 4000

Chinese Foreign Exchange Reserves

billion USD

Source: Bloomberg Last Point April 2016: $3,219.67

SLIDE 38 Chart 38

Dec-13 May-14 Oct-14 Feb-15 Jul-15 Dec-15 Apr-16 2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8 4.0 4.2 30 35 40 45 50 55 60 65 70 75 80 85 BRL/USD - left axis RUB/USD- right axis

Brazilian Real and Russian Ruble Exchange Rates

Last Points 05/12/16: Real: 3.485; Ruble: 64.711 Source: Thomson Reuters

Stronger U.S. Dollar Stronger U.S. Dollar

SLIDE 39 Chart 39

Mexican Peso and WTI Crude Oil

Source: Thomson Reuters Last Points 05/12/16 - Pesos/$:17.964; WTI: $46.70

Jan-14 May-14 Oct-14 Feb-15 Jul-15 Dec-15 Apr-16 12.0 13.0 14.0 15.0 16.0 17.0 18.0 19.0 20.0 20 30 40 50 60 70 80 90 100 110 Mexican Pesos per U.S. Dollar - left axis WTI Crude Oil ($/barrel) - right axis

Stronger U.S. Dollar

SLIDE 40 Chart 40

Jul-12 Apr-13 Jan-14 Oct-14 Jul-15 May-16 1.00 1.05 1.10 1.15 1.20 1.25 1.30 1.35 1.40 75 80 85 90 95 100 105 110 115 120 125 130 USD/EUR - left axis (inverted) JPY/USD - right axis

Euro and Yen Exchange Rates

Last Points 05/12/16 - USD/EUR: 1.138; JPY/USD: 109.01 Source: Thomson Reuters

Stronger U.S. Dollar Stronger U.S. Dollar

SLIDE 41 Chart 41

Jan-14 Jun-14 Nov-14 Apr-15 Sep-15 Feb-16

0% 1% 2% 3% 4% 5%

0% 1% 2% 3% 4% 5% United States Eurozone Japan

Producer Price Index

year/year percent change

Source: Bloomberg; Bureau of Labor Statistics Last Points 04/16: U.S., 0.0%; 03/16: Japan, -3.8%; EZ, -4.2%

SLIDE 42 Chart 42

Chinese Producer Price Index

Source: Bloomberg Last Points April 2016: M/M, 0.7%; Yr/Yr, -3.4%

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

0.0% 0.5% 1.0% 1.5%

0.0% 2.0% 4.0% 6.0% 8.0% Month/Month Percent Change - left axis Year/Year Percent Change - right axis

SLIDE 43 Chart 43

Jan-07 Sep-08 May-10 Jan-12 Sep-13 May-15

0% 1% 2% 3% 4% 5% 6%

0% 1% 2% 3% 4% 5% 6% Goods Services

U.S. Personal Consumption Expenditures Implicit Price Deflator

year/year percent change

Source: Bureau of Economic Analysis Last Points March 2016 - Goods: -1.8%; Services: 2.1%

SLIDE 44 Chart 44

PCE Deflator

seasonally-adjusted

Source: Bureau of Economic Analysis Last Point March 2016 - M/M: 0.1%; Y/Y: 0.8%

2007 2008 2009 2010 2011 2012 2013 2014 2015

0.0% 0.5% 1.0%

0.0% 3.0% 6.0% Month/Month % Change - left axis Year/Year % Change - right axis

Fed Target: 2.0%

SLIDE 45 Chart 45

Japanese CPI and Real GDP

year/year percent change

Source: Japanese Cabinet Office Last Points 4Q 2015- GDP: 0.8%; CPI: 0.3%

1981 1985 1989 1993 1997 2001 2005 2009 2013

0% 2% 4% 6% 8% 10%

0% 2% 4% 6% 8% 10% Real GDP Consumer Price Index

SLIDE 46 Chart 46

Investment Themes

- 1. Short commodities

- 2. Short crude oil and related securities

- 3. Long the dollar vs. euro and yen, commodity currencies and developing

economy currencies

- 4. Short emerging market stocks and bonds

- 5. Short junk bonds

- 6. Long 30-year Treasuries

- 7. Short U.S. stocks

SLIDE 47 Chart 47

10-Year Sovereign Bond Yields

as of 05/12/16 Source: Financial Times

Country Yield Spread vs. Treasurys

Switzerland

Japan

Germany 0.13

Netherlands 0.21

Denmark 0.37

Finland 0.42

France 0.48

Austria 0.52

Belgium 0.52

Ireland 0.86

Canada 1.30

Norway 1.31

United Kingdom 1.53

Italy 1.54

Spain 1.59

United States 1.75

2.43 0.68 Portugal 3.27 1.52 Greece 7.39 5.64

SLIDE 48 Chart 48

Oct-81 Oct-86 Oct-91 Oct-96 Oct-01 Oct-06 Oct-11 5000 10000 15000 20000 25000 30000 35000 5000 10000 15000 20000 25000 30000 35000 25 Year Zero Coupon Bond (Oct-81=100) 28,666 or 17.8% Annual Return S&P 500 Total Return (July-82=100) 4,527 or 12.0% Annual Return

Comparative Stock and Bond Performances

Last Points April 2016 - Stocks: 4,527; Bonds: 28,666 Source: Bianco Research & Haver Analytics