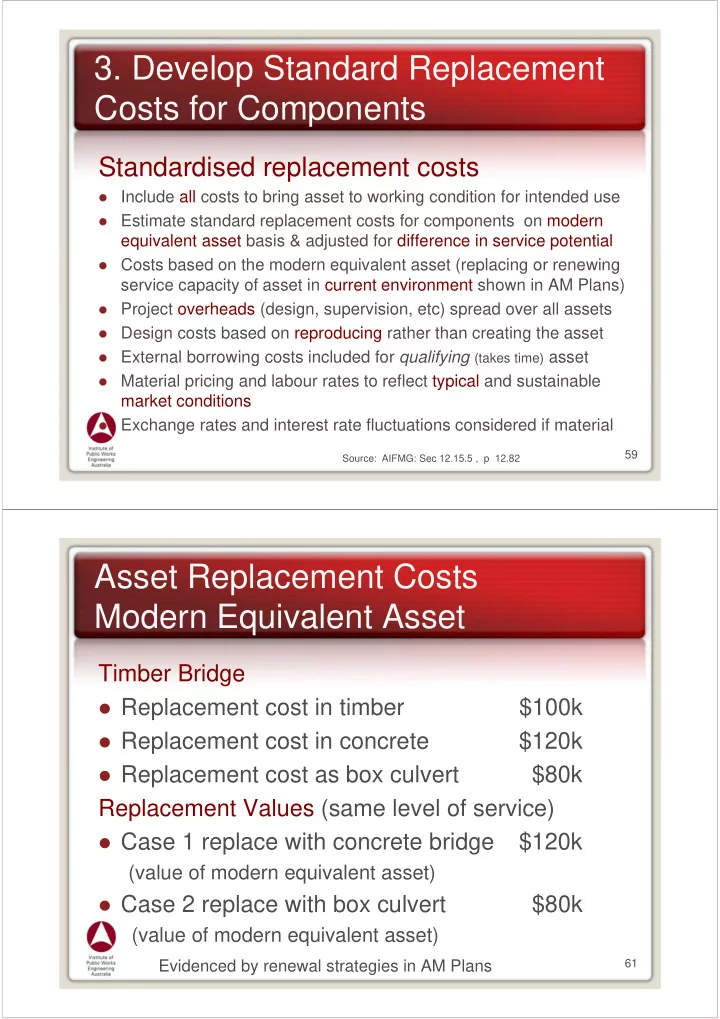

- 3. Develop Standard Replacement

Costs for Components

Standardised replacement costs

Include all costs to bring asset to working condition for intended use Estimate standard replacement costs for components on modern

equivalent asset basis & adjusted for difference in service potential

Costs based on the modern equivalent asset (replacing or renewing

service capacity of asset in current environment shown in AM Plans)

Project overheads (design, supervision, etc) spread over all assets Design costs based on reproducing rather than creating the asset External borrowing costs included for qualifying (takes time) asset Material pricing and labour rates to reflect typical and sustainable

market conditions

Exchange rates and interest rate fluctuations considered if material

59

Source: AIFMG: Sec 12.15.5 , p 12.82

Asset Replacement Costs Modern Equivalent Asset

Timber Bridge

Replacement cost in timber

$100k

Replacement cost in concrete

$120k

Replacement cost as box culvert

$80k Replacement Values (same level of service)

Case 1 replace with concrete bridge $120k

(value of modern equivalent asset)

Case 2 replace with box culvert

$80k

(value of modern equivalent asset)

Evidenced by renewal strategies in AM Plans

61