SLIDE 3 3

Board Status Report, May 7, 2009

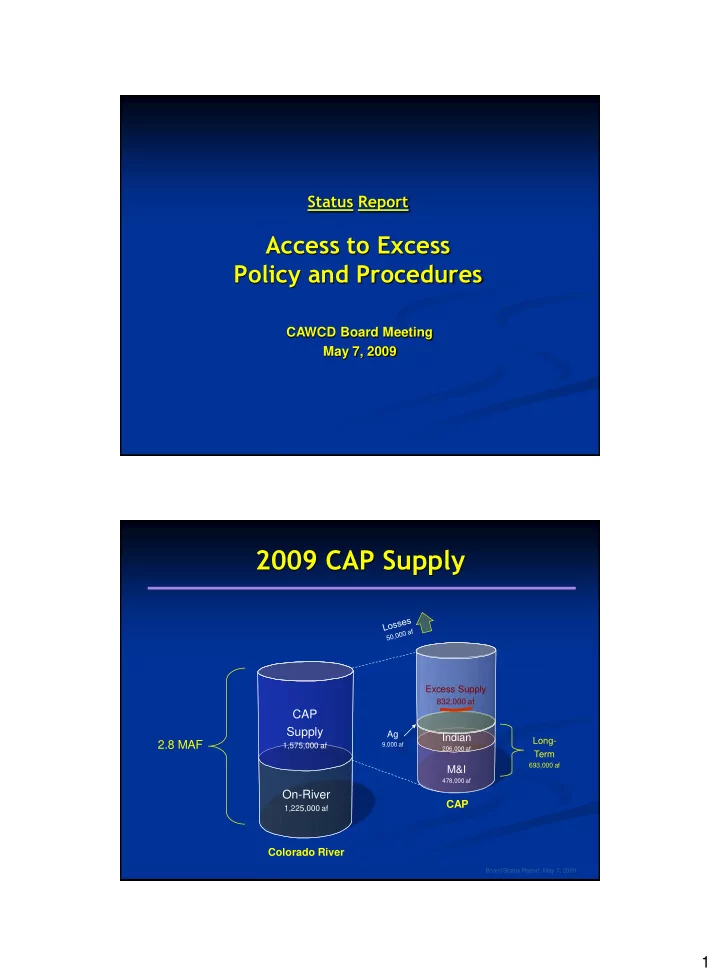

AWBA

Goal was to ensure that Arizona’s entire Colorado River

Allocation was put to use by storing Excess CAP water

Firm M&I subcontracts Firm Colorado River communities Assist water management goals Enter into interstate banking

Original “Access to Excess” allocation scheme:

Fill all Excess CAP orders AWBA stores the rest Use of Excess CAP water to solve problems

Board Status Report, May 7, 2009

Ag Settlement Pool

In exchange for contract relinquishment:

Defined block of Excess CAP water through 2030 Highest priority of Excess Use of Excess CAP water to solve problems

Pinal AMA Phoenix AMA Tucson AMA 57,527 AF 289,799 AF 32,537 AF 13,582 AF

A critical component of the

Settlements Act

Ag Settlement Pool Allocations

Use of Excess CAP water to solve problems