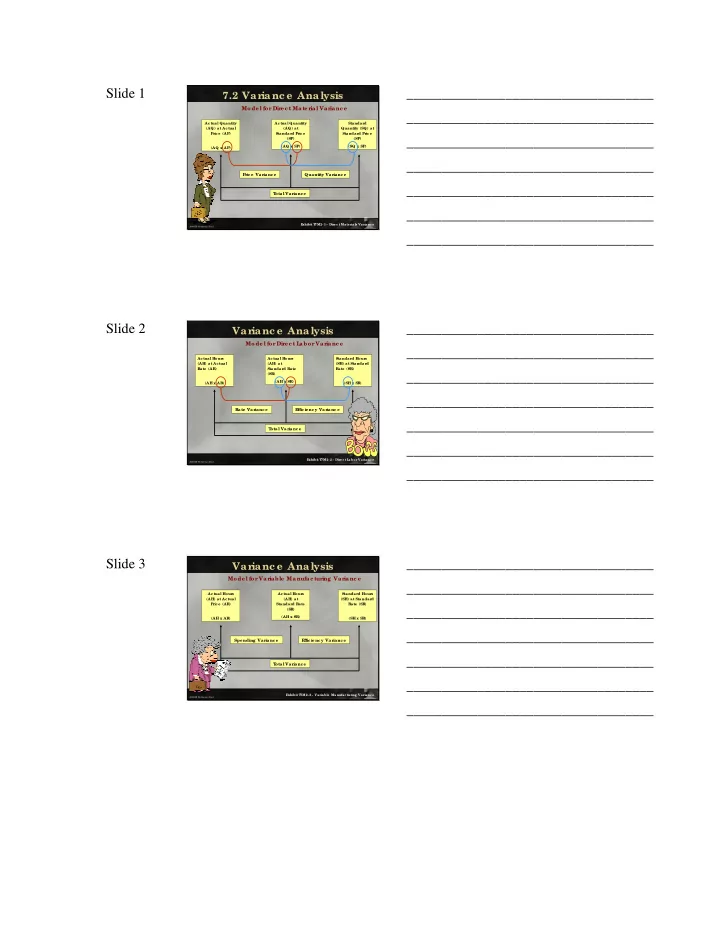

Slide 1

7.2 Var ianc e Analysis

Mode l for Dir e c t Mater ial Var ianc e

2005 KD Ha the wa y-Dia l

Ac tual Quantity (AQ) at Ac tual Pr ic e (AP) (AQ x AP) Ac tual Quantity (AQ) at Standar d Pr ic e (SP) (AQ x SP) Standar d Quantity (SQ) at Standar d Pr ic e (SP) (SQ x SP) Pric e Varianc e Quantity Varianc e T

- tal Varia nc e

E xhibit T 7M2-1~ Dir e c t Ma ter ia ls Var ianc e

___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ Slide 2

Var ianc e Analysis

Mode l for Dir ec t L abor Var ianc e

2005 KD Ha the wa y-Dia l

Ac tual Hour s (AH) at Ac tual Rate (AR) (AH x AR ) Ac tual Hour s (AH) at Standar d R ate (SR ) (AH x SR ) Standar d Hour s (SH) at Standar d R ate (SR ) (SH x SR ) Rate Varianc e E ffic ie nc y Var ianc e T

- tal Var

ia nc e

E xhibit T 7M2-2~ Dire c t L abor Va rianc e

___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ Slide 3

Var ianc e Analysis

Mode l for Var iable Manufac tur ing Var ianc e

2005 KD Ha the wa y-Dia l

Ac tual Hour s (AH) at Ac tual Pr ic e (AR ) (AH x AR ) Ac tual Hour s (AH) at Standar d R ate (SR ) (AH x SR ) Standar d Hour s (SH) at Standar d R ate (SR ) (SH x SR ) Spe nding Varianc e E ffic ie nc y Var ianc e T

- tal Varia nc e

E xhibit T 7M2-3~ Varia ble Manufa c turing Varianc e