SLIDE 1

1

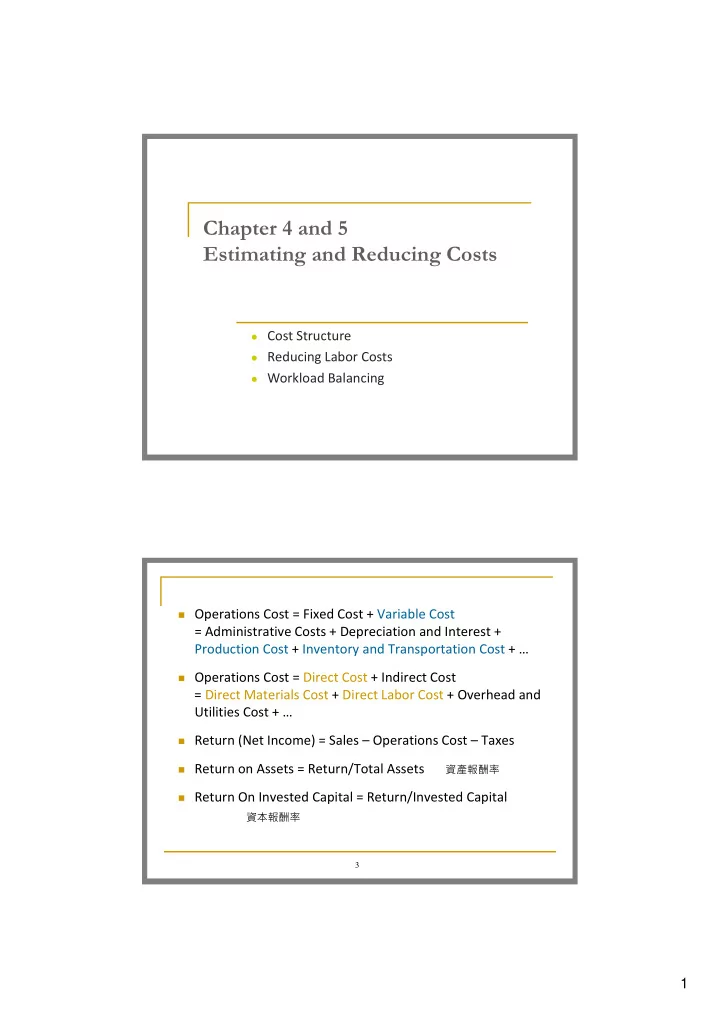

Chapter 4 and 5 Estimating and Reducing Costs

Cost Structure Reducing Labor Costs Workload Balancing 3

Operations Cost = Fixed Cost + Variable Cost

= Administrative Costs + Depreciation and Interest + Production Cost + Inventory and Transportation Cost + …

Operations Cost = Direct Cost + Indirect Cost

= Direct Materials Cost + Direct Labor Cost + Overhead and Utilities Cost + …

Return (Net Income) = Sales – Operations Cost – Taxes Return on Assets = Return/Total Assets Return On Invested Capital = Return/Invested Capital