SLIDE 1

Programme

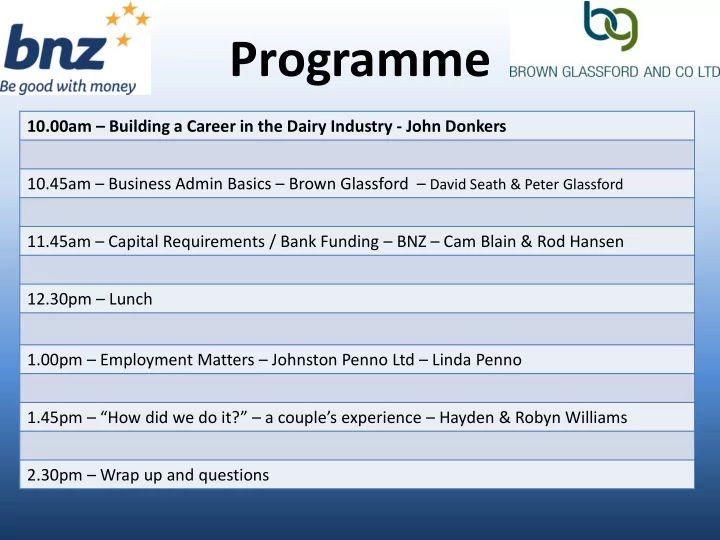

10.00am – Building a Career in the Dairy Industry - John Donkers 10.45am – Business Admin Basics – Brown Glassford – David Seath & Peter Glassford 11.45am – Capital Requirements / Bank Funding – BNZ – Cam Blain & Rod Hansen 12.30pm – Lunch 1.00pm – Employment Matters – Johnston Penno Ltd – Linda Penno 1.45pm – “How did we do it?” – a couple’s experience – Hayden & Robyn Williams 2.30pm – Wrap up and questions