SLIDE 1

Moral Hazard within Economic Monetary Union Weak Countries

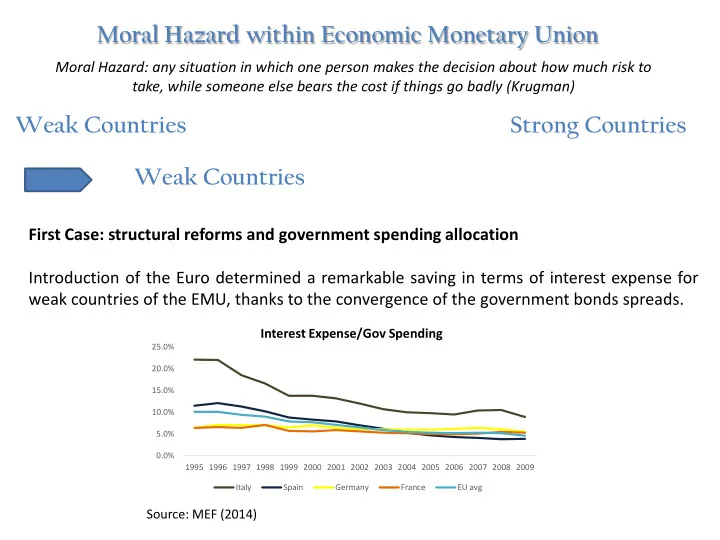

First Case: structural reforms and government spending allocation Introduction of the Euro determined a remarkable saving in terms of interest expense for weak countries of the EMU, thanks to the convergence of the government bonds spreads.

Weak Countries Strong Countries

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Interest Expense/Gov Spending

Italy Spain Germany France EU avg