SLIDE 1

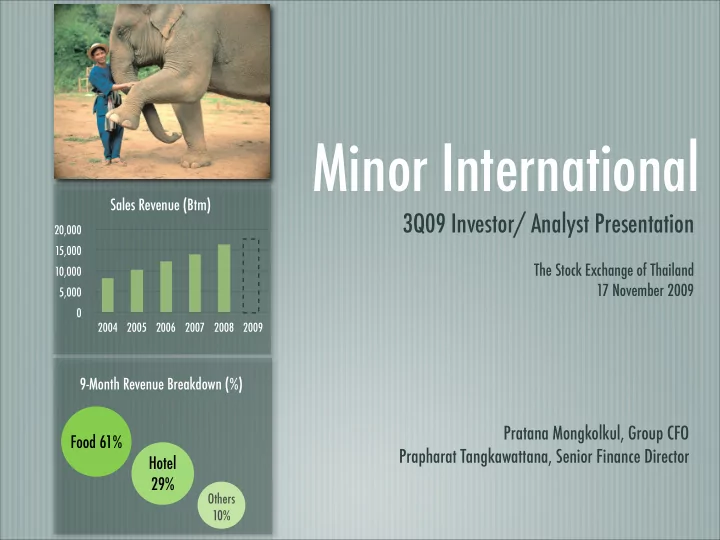

9-Month Revenue Breakdown (%)

3Q09 Investor/ Analyst Presentation

The Stock Exchange of Thailand 17 November 2009

Pratana Mongkolkul, Group CFO Prapharat Tangkawattana, Senior Finance Director

Minor International

Food 61% Hotel 29%

Others 10%

5,000 10,000 15,000 20,000 2004 2005 2006 2007 2008 2009

Sales Revenue (Btm)