SLIDE 1

1

April 8, 2019 Q1-2019 PRESENTATION CHANGES / NEW ACCOUNTING STANDARDS MD&A and/or Consolidated Financial Statements (in Canadian dollars except as otherwise noted) To whom it may concern, Effective Q1-2019, we have refined the way we report the performance of our distribution channel, as well as investment/other expenses, to better align our reporting with how management views the results of our business. These changes, outlined in the section ‘Presentation changes’ below, have no impact on Net Operating Income (NOI), net income, or on 2019 growth guidance previously provided for distribution income and net investment income. Furthermore, on January 1, 2019, IFRS 16 (Leases) came into effect. The impact of this new accounting standard is outlined in the section ‘New Accounting standards’. PRESENTATION CHANGES A) Distribution EBITA will replace Net distribution income (MD&A basis)

1 Broker associates include joint ventures and brokers over which we have significant influence. The results from these investments

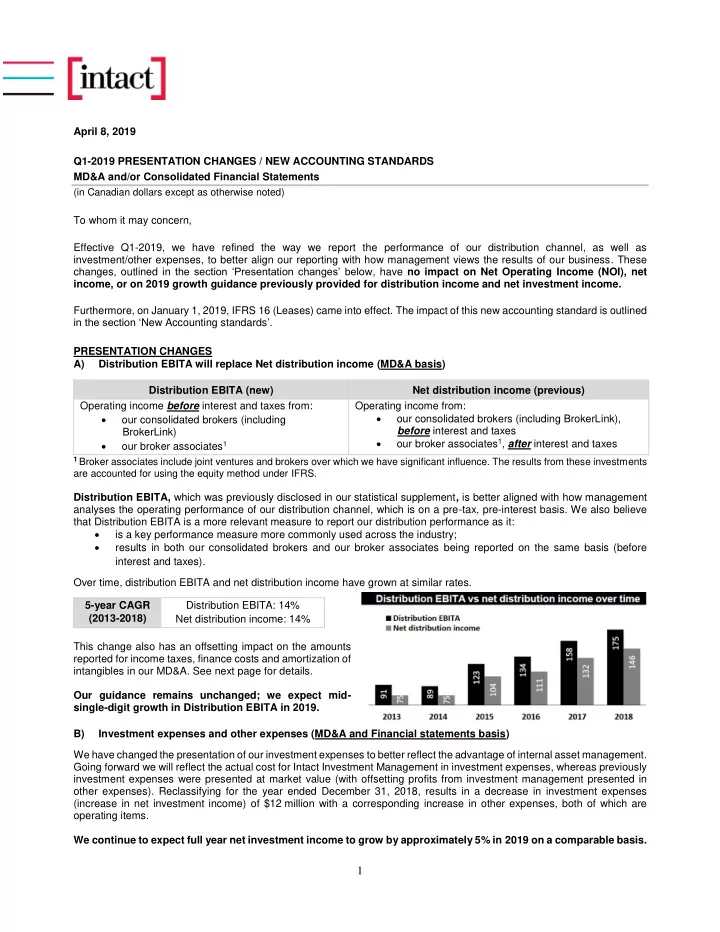

are accounted for using the equity method under IFRS. Distribution EBITA, which was previously disclosed in our statistical supplement, is better aligned with how management analyses the operating performance of our distribution channel, which is on a pre-tax, pre-interest basis. We also believe that Distribution EBITA is a more relevant measure to report our distribution performance as it:

- is a key performance measure more commonly used across the industry;

- results in both our consolidated brokers and our broker associates being reported on the same basis (before

interest and taxes). Over time, distribution EBITA and net distribution income have grown at similar rates. This change also has an offsetting impact on the amounts reported for income taxes, finance costs and amortization of intangibles in our MD&A. See next page for details. Our guidance remains unchanged; we expect mid- single-digit growth in Distribution EBITA in 2019. B) Investment expenses and other expenses (MD&A and Financial statements basis) We have changed the presentation of our investment expenses to better reflect the advantage of internal asset management. Going forward we will reflect the actual cost for Intact Investment Management in investment expenses, whereas previously investment expenses were presented at market value (with offsetting profits from investment management presented in

- ther expenses). Reclassifying for the year ended December 31, 2018, results in a decrease in investment expenses

(increase in net investment income) of $12 million with a corresponding increase in other expenses, both of which are

- perating items.

We continue to expect full year net investment income to grow by approximately 5% in 2019 on a comparable basis. Distribution EBITA (new) Net distribution income (previous) Operating income before interest and taxes from:

- ur consolidated brokers (including

BrokerLink)

- ur broker associates1

Operating income from:

- ur consolidated brokers (including BrokerLink),

before interest and taxes

- ur broker associates1, after interest and taxes