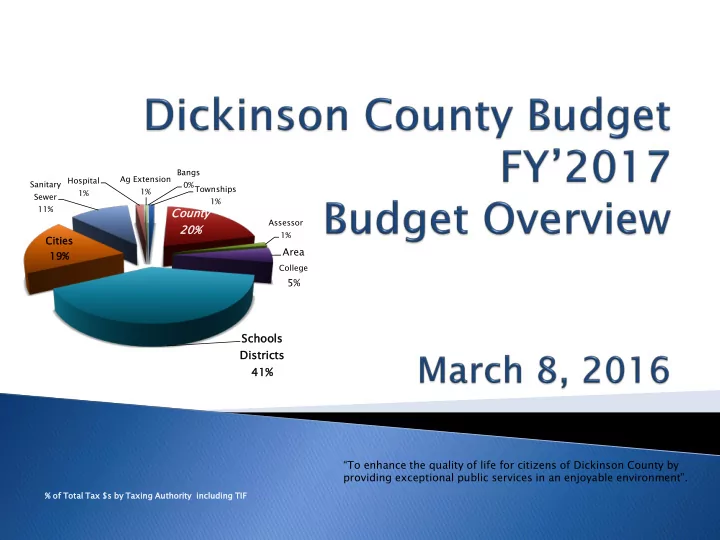

SLIDE 31 31

Rur ural al Fun und d Expen enses ses & R Reven enue ues by Year ar

Source: Auditor’s Budget Reports Rural Basic Revenue by Year

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Fy16 Budget FY17 Request

Net property tax

$917,745 $967,461 $967,331 $1,097,790 $1,226,223 $1,341,502 $1,407,202 $1,468,376 $1,541,723 $1,588,903 $1,631,683 $1,820,783

Local Option Sales Tax

$721,971 $876,301 $761,044 $819,998 $741,437 $841,908 $850,023 $856,545 $819,501 $979,463 $825,000 $1,000,000

Commercial replacement

$87,398

Other Revenues

$41,711 $39,749 $39,391 $39,442 $41,623 $50,274 $49,612 $57,951 $59,272 $81,063 $74,084 $160,594

Total

$1,681,427 $1,883,511 $1,767,766 $1,957,230 $2,009,283 $2,233,684 $2,306,837 $2,382,872 $2,420,496 $2,649,429 $2,530,767 $2,981,377

Rural Basic Expenses by Year

2006 2007 2008 2009 2010 2011 2012 2013 2014 FY15 FY16 Budget FY17 Request

Secondary Roads

$1,340,795 $1,560,137 $1,699,087 $1,884,085 $1,754,358 $1,850,724 $1,958,985 $2,011,045 $2,113,066 $2,177,198 $2,244,723 $2,498,568

Sirens

$0 $23,229 $23,287 $46,154 $37,000 $25,112 $28,368 $33,267 $3,768 $29,594 $45,000 $9,900

28E Agreement

$59,220 $84,600 $84,600 $84,600 $84,600 $74,957 $70,297 $84,600 $84,600 $84,600 $84,600 $84,600

Landfill Commission

$7,318 $7,318 $18,295

Recycling

$44,700 $45,600 $45,600 $48,900 $48,000 $37,920 $37,920 $40,904 $40,211 $40,124 $44,290 $45,722

Roadside Management

$0 $99,736

Weed Commissioner

$13,291 $13,919 $14,042 $15,032 $16,638 $15,073 $15,848 $17,119 $15,946 $16,825 $18,695 $18,042

Libraries

$56,000 $58,000 $58,000 $58,000 $58,000 $58,000 $58,000 $58,000 $58,000 $58,000 $58,000 $58,000

Ambulance

$3,494 $3,494 $3,494 $3,494 $3,494 $21,179 $3,137 $10,435 $3,127 $3,117 $3,117 $3,117

Total

$1,517,500 $1,788,979 $1,928,110 $2,140,265 $2,002,090 $2,082,965 $2,172,555 $2,255,370 $2,318,718 $2,416,776 $2,505,743 $2,835,980