SLIDE 1

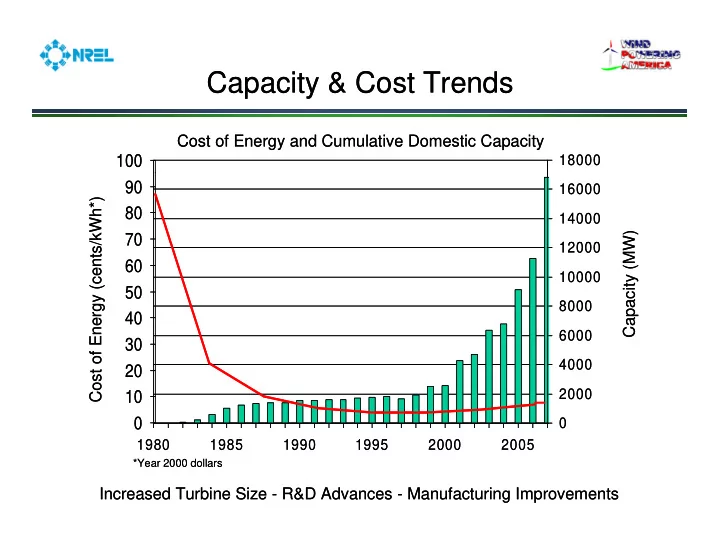

Capacity & Cost Trends Capacity & Cost Trends

18000

100 Cost of Energy and Cumulative Domestic Capacity

18000

100 Cost of Energy and Cumulative Domestic Capacity

12000 14000 16000

70 80 90 W) /kWh*)

12000 14000 16000

70 80 90 W) /kWh*)

8000 10000 12000

40 50 60 70 pacity (MW rgy (cents/

8000 10000 12000

40 50 60 70 pacity (MW rgy (cents/

4000 6000

20 30 40 Cap

- st of Ener

4000 6000

20 30 40 Cap

- st of Ener

2000 1980 1985 1990 1995 2000 2005

10 Co

2000 1980 1985 1990 1995 2000 2005

10 Co Increased Turbine Size - R&D Advances - Manufacturing Improvements

*Year 2000 dollars

Increased Turbine Size - R&D Advances - Manufacturing Improvements

*Year 2000 dollars