SLIDE 1

1 Department of Logistics Management

Box-Jenkins Forecasting

傳統預測方式

- 觀察數據變化的型態,選擇影響數據變化的因素

– Trend, seasonal factors, causal forecasting

- 如果預測模式合理,預測誤差(residuals)接近隨機變化

Box-Jenkins預測

- 將難以解釋的數據變化輸入black box

- 觀察black box產生的預測誤差是否接近white noise

– White noise: 隨機變化的數值,沒有關聯,看不出任何變化型態

- 如果預測誤差不像是white noise,再換另一種black box

– Three types of black boxes: MA, AR, ARMA

1

Department of Logistics Management

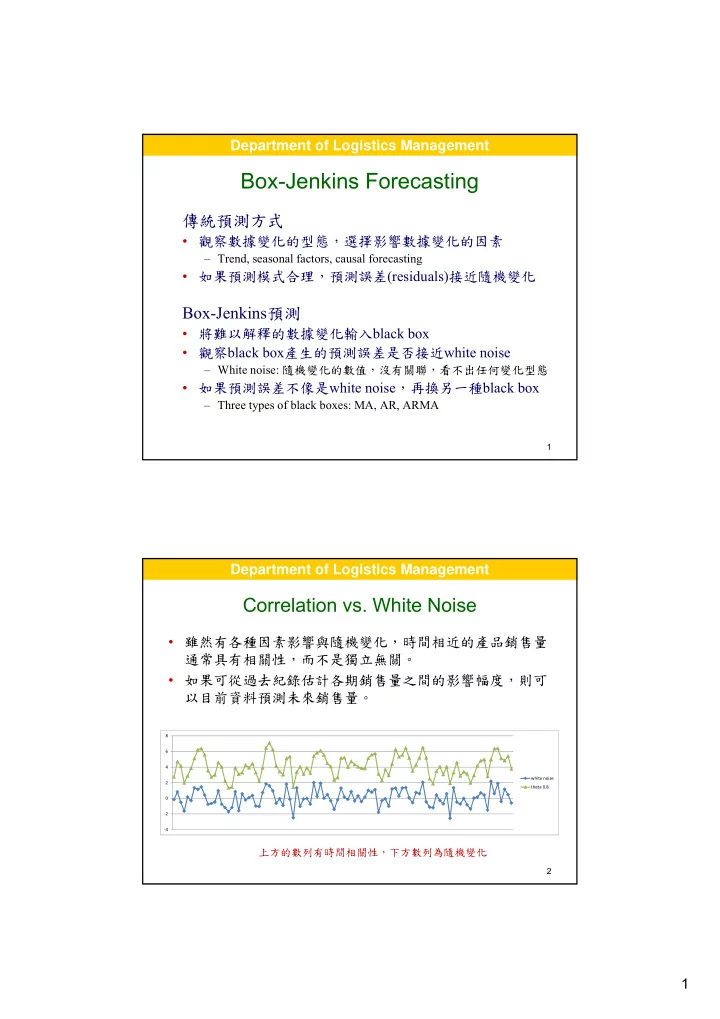

Correlation vs. White Noise

- 雖然有各種因素影響與隨機變化,時間相近的產品銷售量

通常具有相關性,而不是獨立無關。

- 如果可從過去紀錄估計各期銷售量之間的影響幅度,則可

以目前資料預測未來銷售量。

‐4 ‐2 2 4 6 8 white noise theta 0.8

2

上方的數列有時間相關性,下方數列為隨機變化