SLIDE 1

4/6/2011 1

Aerospace & Defense Forum M&A Panel Aerospace & Defense Forum M&A Panel

Michael Cohen Global Capital Markets Inc

M&A Panel M&A Panel

Global Capital Markets, Inc.

310‐829‐9301

March 18, 2011 March 18, 2011

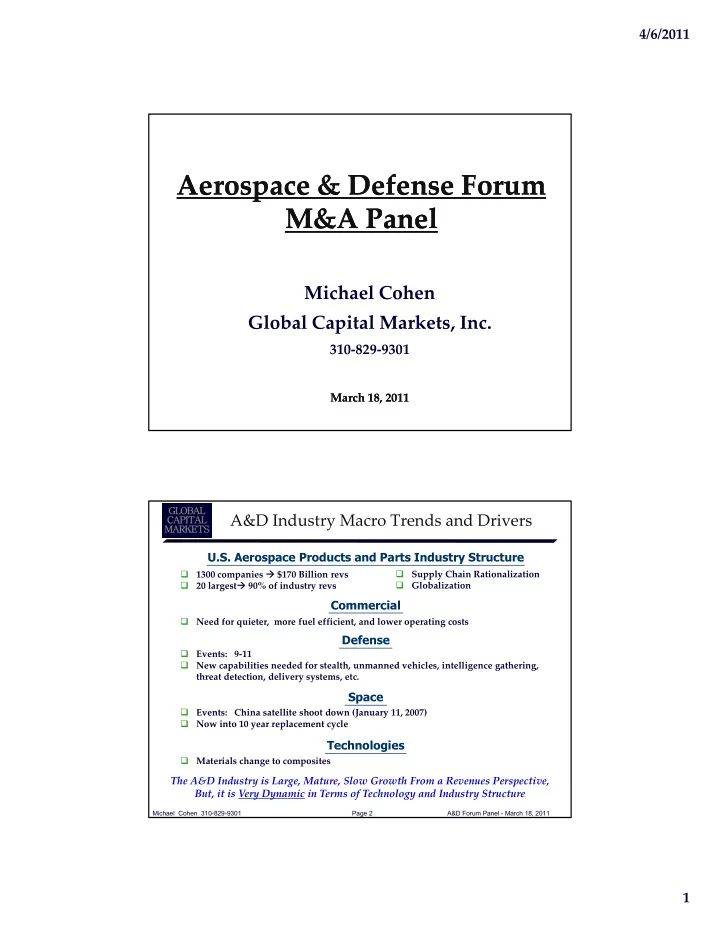

A&D Industry Macro Trends and Drivers

Commercial

- Supply Chain Rationalization

- Globalization

U.S. Aerospace Products and Parts Industry Structure

- 1300 companies $170 Billion revs

- 20 largest 90% of industry revs

- Need for quieter, more fuel efficient, and lower operating costs

- Events: 9‐11

- New capabilities needed for stealth, unmanned vehicles, intelligence gathering,

threat detection, delivery systems, etc.

Commercial Defense Space

- Events: China satellite shoot down (January 11 2007)

Michael Cohen 310-829-9301 Page 2 A&D Forum Panel - March 18, 2011

The A&D Industry is Large, Mature, Slow Growth From a Revenues Perspective, But, it is Very Dynamic in Terms of Technology and Industry Structure

- Events: China satellite shoot down (January 11, 2007)

- Now into 10 year replacement cycle

- Materials change to composites

Technologies