SLIDE 1

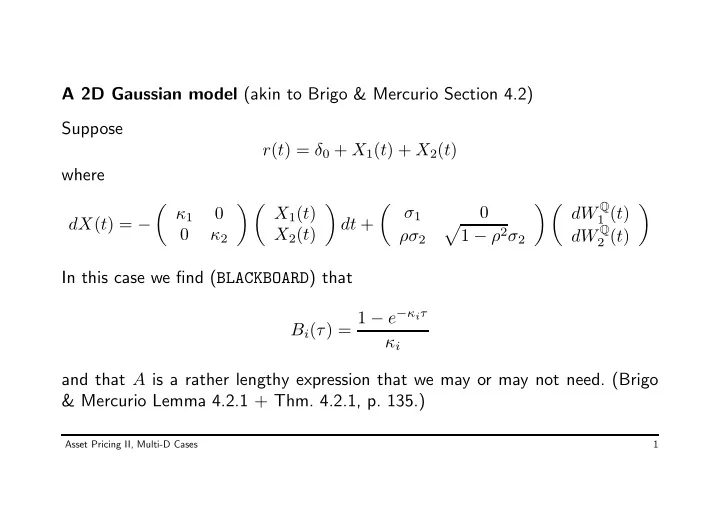

A 2D Gaussian model (akin to Brigo & Mercurio Section 4.2) Suppose r(t) = δ0 + X1(t) + X2(t) where dX(t) = −

- κ1

κ2 X1(t) X2(t)

- dt +

σ1 ρσ2

- 1 − ρ2σ2

dW Q

1 (t)

dW Q

2 (t)

- In this case we find (BLACKBOARD) that