SLIDE 1

1

Vertical Arrangements and Competition: Evidence from Electricity Markets

Jim Bushnell, UC Energy Institute www.ucei.berkeley.edu

Presentation based upon “Vertical Arrangements, Market Structure and Competition: An Analysis of US Restructured Electricity Markets” with Erin Mansur and Celeste Saravia

2

Outline

- Motivation

– How do different market attributes interact in determining market competitiveness?

- Punchline

– By traditional measures of horizontal market structure, California should have been the most competitive, not the least – vertical relationships played a key role in the “successful” markets

- General implications

- The details of the empirical study

- conclusions

3

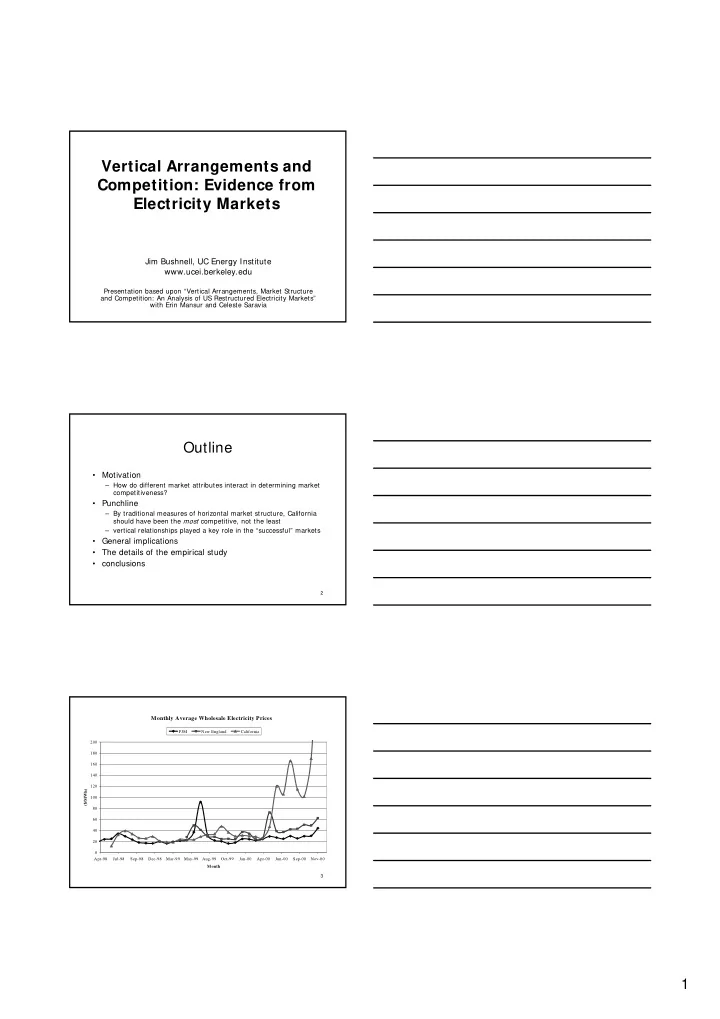

Monthly Average Wholesale Electricity Prices

20 40 60 80 100 120 140 160 180 200 Apr-98 Jul-98 Sep-98 Dec-98 Mar-99 May-99 Aug-99 Oct-99 Jan-00 Apr-00 Jun-00 Sep-00 Nov-00 Month ($/MWh) PJM New England California