SLIDE 1

. .

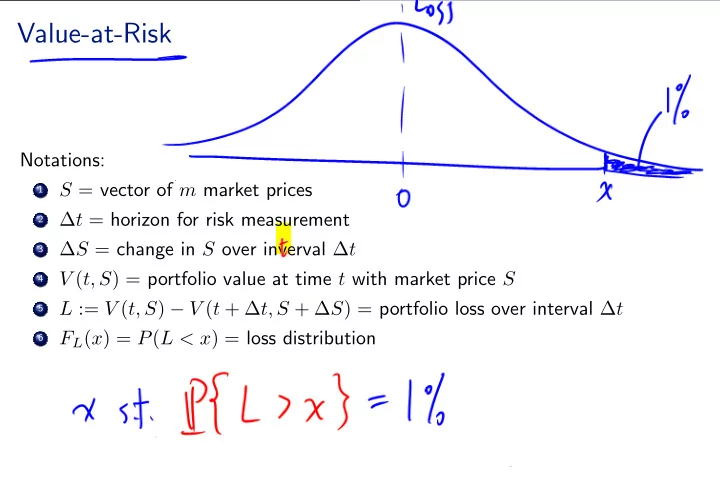

Value-at-Risk

Notations: .

1

S = vector of m market prices .

2

∆t = horizon for risk measurement .

3

∆S = change in S over inverval ∆t .

4

V (t, S) = portfolio value at time t with market price S .

5

L := V (t, S) − V (t + ∆t, S + ∆S) = portfolio loss over interval ∆t .

6