SLIDE 1

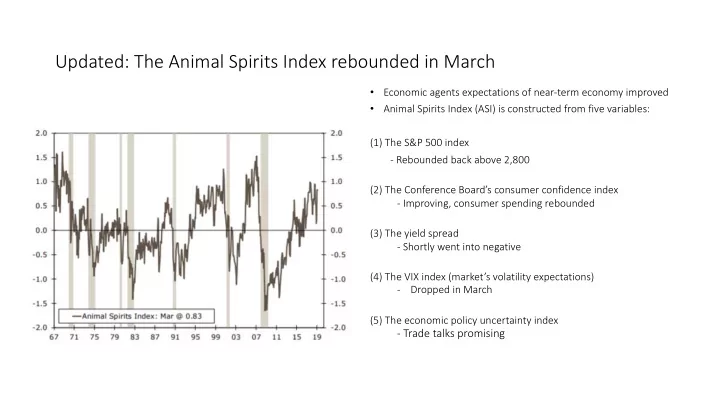

Updated: The Animal Spirits Index rebounded in March

- Economic agents expectations of near-term economy improved

- Animal Spirits Index (ASI) is constructed from five variables:

(1) The S&P 500 index

- Rebounded back above 2,800

(2) The Conference Board’s consumer confidence index

- Improving, consumer spending rebounded

(3) The yield spread

- Shortly went into negative

(4) The VIX index (market’s volatility expectations)

- Dropped in March

(5) The economic policy uncertainty index

- Trade talks promising