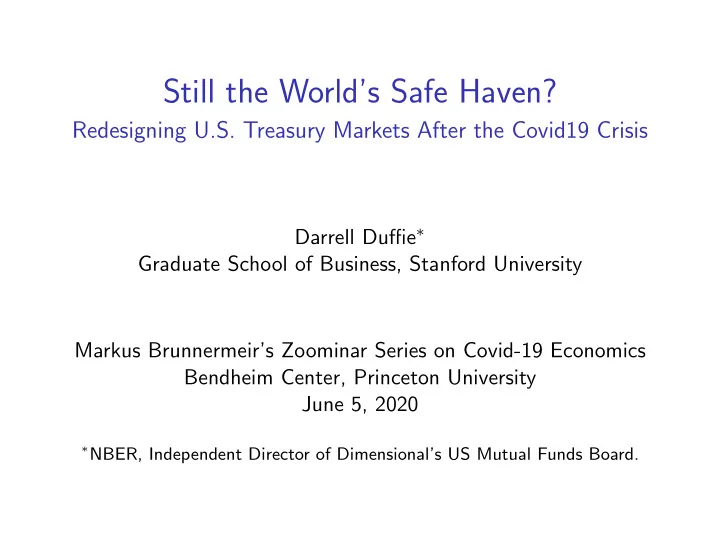

SLIDE 10 Cash-futures basis

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 01/02/20 01/04/20 01/06/20 01/08/20 01/10/20 01/12/20 01/14/20 01/16/20 01/18/20 01/20/20 01/22/20 01/24/20 01/26/20 01/28/20 01/30/20 02/01/20 02/03/20 02/05/20 02/07/20 02/09/20 02/11/20 02/13/20 02/15/20 02/17/20 02/19/20 02/21/20 02/23/20 02/25/20 02/27/20 02/29/20 03/02/20 03/04/20 03/06/20 03/08/20 03/10/20 03/12/20 03/14/20 03/16/20 03/18/20 03/20/20 03/22/20 03/24/20 03/26/20

Implied difference in interest rate (percent)

10 Year 5 Year 2 Year

Figure: The difference, in percent, between (a) the repo rate implied by selling

treasury futures, purchasing the cheapest-to-deliver underlying treasury note, and closing the futures contract at maturity by delivering the treasury note, and (b) the actual market general-collateral one-month repo rate. The data shown in the figure were provided to the author by Andreas Schrimpf, Hyun Song Shin, and Vladyslav Sushko, from Graph 3 of their paper “Leverage and Margin Spirals in Fixed Income Markets During the Covid-19 Crisis,” BIS Bulletin, Number 2, April 2, 2020.