SLIDE 1

9/23/2016 1

SRI LANK SRI LANKA

Trade and Investment Trade and Investment Opportunities Opportunities

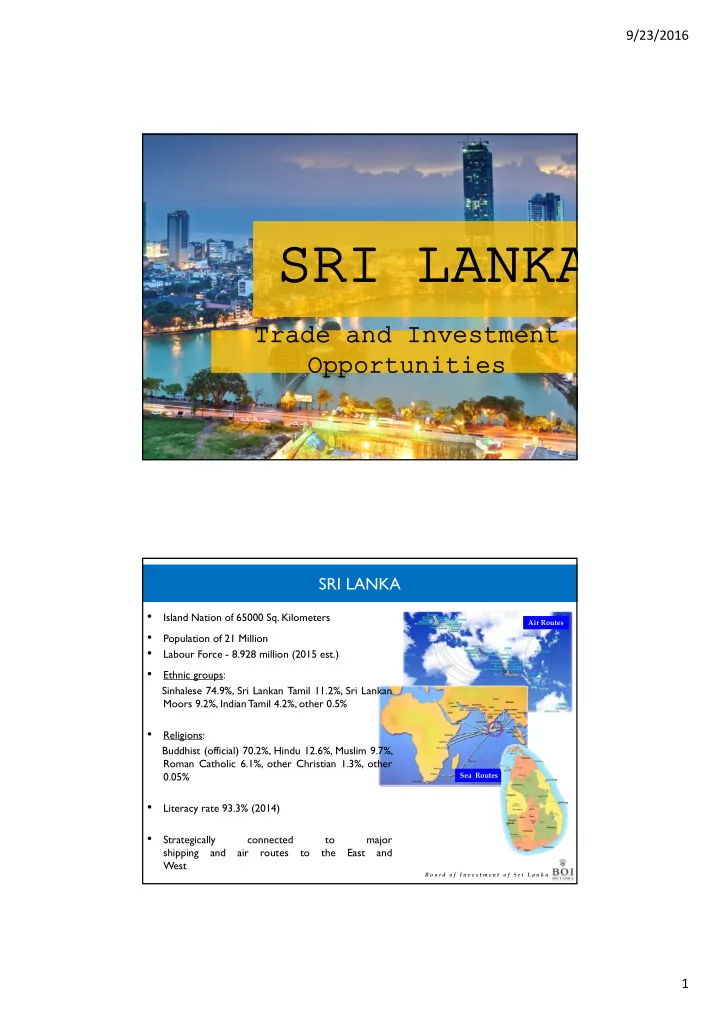

SRI LANKA

Air Routes Sea Routes

- Island Nation of 65000 Sq. Kilometers

- Population of 21 Million

- Labour Force - 8.928 million (2015 est.)

- Ethnic groups:

Sinhalese 74.9%, Sri Lankan Tamil 11.2%, Sri Lankan Moors 9.2%, IndianTamil 4.2%, other 0.5%

- Religions:

Buddhist (official) 70.2%, Hindu 12.6%, Muslim 9.7%, Roman Catholic 6.1%, other Christian 1.3%, other 0.05%

- Literacy rate 93.3% (2014)

- Strategically

connected to major shipping and air routes to the East and West

B o a r d o f I n v e s t m e n t o f S r i L a n k a