SLIDE 1

{S2458666; 1}

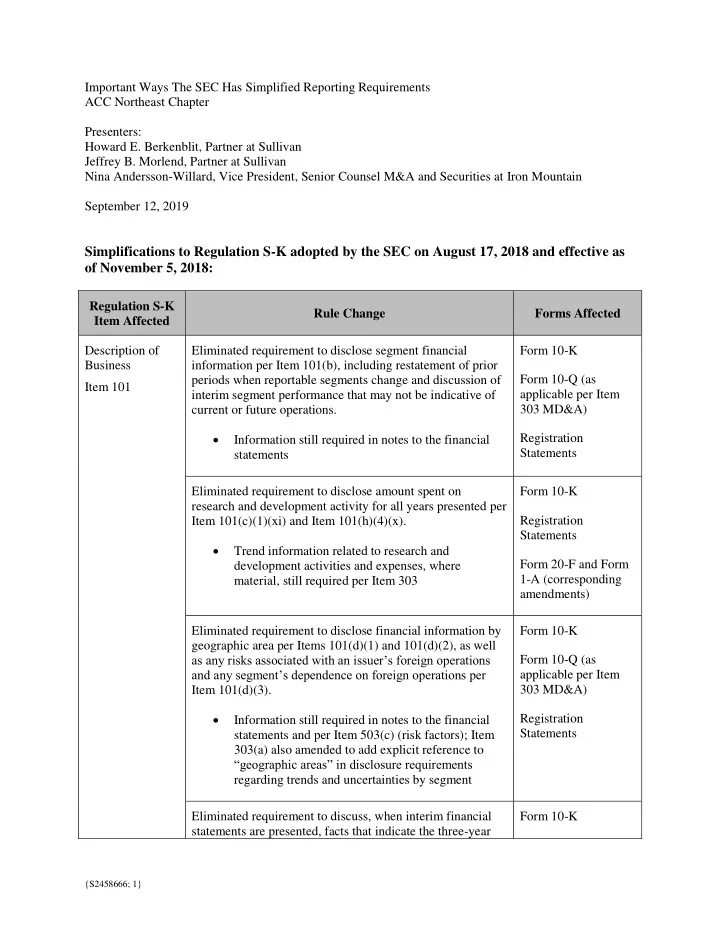

Important Ways The SEC Has Simplified Reporting Requirements ACC Northeast Chapter Presenters: Howard E. Berkenblit, Partner at Sullivan Jeffrey B. Morlend, Partner at Sullivan Nina Andersson-Willard, Vice President, Senior Counsel M&A and Securities at Iron Mountain September 12, 2019

Simplifications to Regulation S-K adopted by the SEC on August 17, 2018 and effective as

- f November 5, 2018: