SLIDE 1

Regression Models

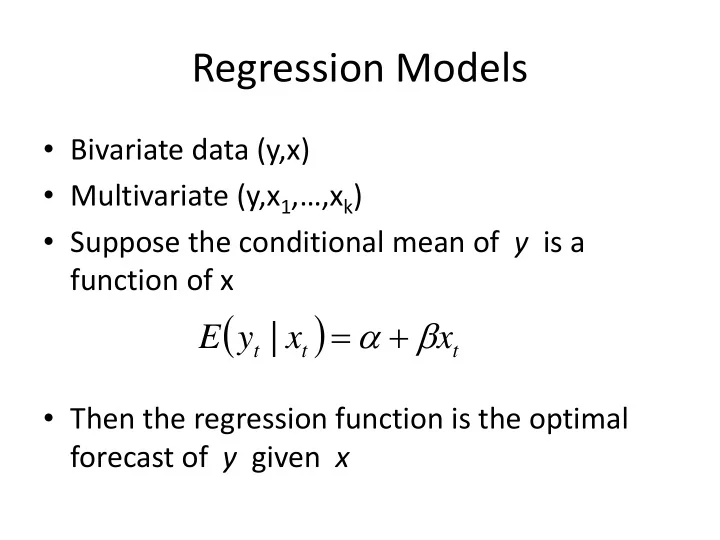

- Bivariate data (y,x)

- Multivariate (y,x1,…,xk)

- Suppose the conditional mean of y is a

function of x

- Then the regression function is the optimal

forecast of y given x

( )

t t t