SLIDE 1

FIN 551: Fundamental Analysis

1

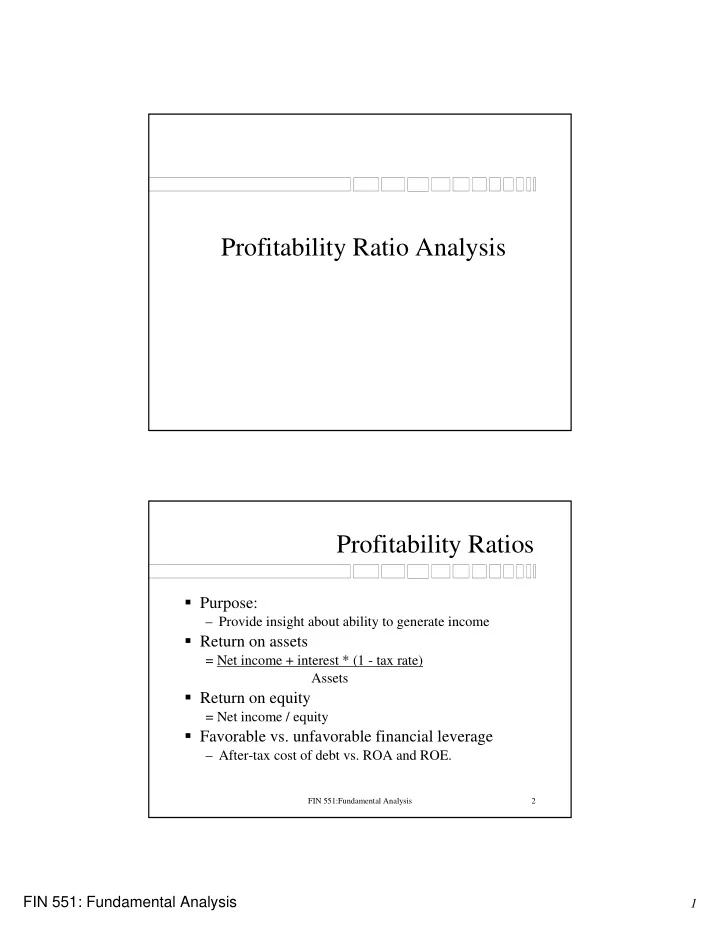

Profitability Ratio Analysis

FIN 551:Fundamental Analysis 2

Profitability Ratio Analysis Profitability Ratios Purpose: - - PDF document

Profitability Ratio Analysis Profitability Ratios Purpose: Provide insight about ability to generate income Return on assets = Net income + interest * (1 - tax rate) Assets Return on equity = Net income / equity Favorable

1

FIN 551:Fundamental Analysis 2

2

FIN 551:Fundamental Analysis 3

» What is the contribution of operating activity to profitability? » Can asset management improve profitability? » Has debt financing provided favorable leverage? » How have income taxes impacted profitability? » What is the influence of non-operating activities on profitability? » Can the firm sustain its current level of growth?

FIN 551:Fundamental Analysis 4

3

FIN 551:Fundamental Analysis 5

FIN 551:Fundamental Analysis 6

4

FIN 551:Fundamental Analysis 7

» Receivables, inventory, payables » Support normal operations

» Assets generate long-term earnings.

FIN 551:Fundamental Analysis 8

5

FIN 551:Fundamental Analysis 9

FIN 551:Fundamental Analysis 10

6

FIN 551:Fundamental Analysis 11

FIN 551:Fundamental Analysis 12

7

FIN 551:Fundamental Analysis 13

FIN 551:Fundamental Analysis 14

» Show a separate tax effect later.

8

FIN 551:Fundamental Analysis 15

» Interest expense multiplier » Balance sheet financing multiplier

FIN 551:Fundamental Analysis 16

9

FIN 551:Fundamental Analysis 17

FIN 551:Fundamental Analysis 18

10

FIN 551:Fundamental Analysis 19

FIN 551:Fundamental Analysis 20

1 2 3 4 5 6 7 8 9 2 4 6 8 10 12 14 16 18 20

Years %

11

FIN 551:Fundamental Analysis 21

FIN 551:Fundamental Analysis 22

12

FIN 551:Fundamental Analysis 23

FIN 551:Fundamental Analysis 24

13

FIN 551:Fundamental Analysis 25

FIN 551:Fundamental Analysis 26

14

FIN 551:Fundamental Analysis 27

Formula: Sustainable growth = ROS * Retention Rate * Assets/Equity . Assets/Sales - ROS * Retention Rate * Assets/Equity

FIN 551:Fundamental Analysis 28

15

FIN 551:Fundamental Analysis 29

FIN 551:Fundamental Analysis 30