SLIDE 1

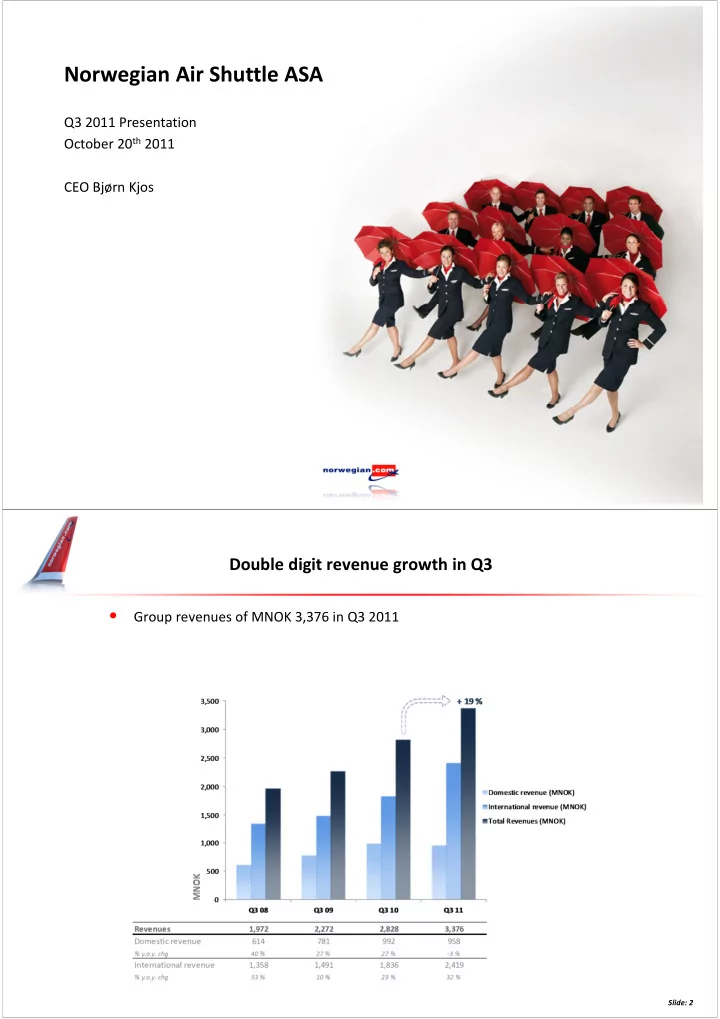

Norwegian Air Shuttle ASA

Q3 2011 Presentation October 20th 2011 CEO Bjørn Kjos

Double digit revenue growth in Q3

- Group revenues of MNOK 3,376 in Q3 2011

Slide: 2

Norwegian Air Shuttle ASA Q3 2011 Presentation October 20 th 2011 - - PDF document

Norwegian Air Shuttle ASA Q3 2011 Presentation October 20 th 2011 CEO Bjrn Kjos Double digit revenue growth in Q3 Group revenues of MNOK 3,376 in Q3 2011 Slide: 2 Q3 operating result (EBITDA) of 1 Billion NOK, improved by 378 million

Slide: 2

(840)

(624)

(573) .

(733)

(528)

Slide: 3

4

5

1,181 Cash 1,430 1,253 Receivables 1,577 4,047 Non-current assets 6,035

1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 Q3 10 Q3 11

MNOK

Equity 2,059 1,799 Pre-sold tickets 1,354 1,067 Other current liabilities 2,063 1,864 Long term liabilities 3,565 1,752

Q3 11 Q3 10

Slide: 6 Slide: 6

Equity 2,059 Pre-sold tickets 1,354 current liabilities 2,063 LT liabilities 3,565

Q3 11 (aircraft sold) Q3 11 (actual)

1,430 Cash 1,577 Receivables 6,035 Non-current assets

1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 Q3 11 (actual) Q3 11 (aircraft sold)

MNOK

7

ASK 3,590 3,979 5,331 6,480 Load Factor 82 % 82 % 80 % 84 %

82 % 82 % 80 % 84 %

0 % 20 % 40 % 60 % 80 % 100 % 1,000 2,000 3,000 4,000 5,000 6,000 7,000 Q3 08 Q3 09 Q3 10 Q3 11 Load Factor Available Seat KM (ASK)

ASK Load Factor

+ 22 %

Slide: 8 Slide: 8

Passengers (million) 2.6 3.1 3.8 4.6 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 Q3 08 Q3 09 Q3 10 Q3 11 Passengers (million) + 21 %

Slide: 9 Slide: 9

11

Cost per ASK (CASK) (NOK) 0.49 0.44 0.41 0.41 CASK excl. fuel & hedge gain 0.30 0.32 0.30 0.27

0.30 0.32 0.30 0.23 0.04

0.19 0.12 0.11 0.14 0.20 0.25 0.30 0.35 0.40 0.45 0.50 Q3 08 Q3 09 Q3 10 Q3 11 Operating cost EBITDA level per ASK (CASK)

Fuel share of CASK CASK excl fuel

Cost reducing hedge-effect Underlying CASK Reported CASK

Slide: 12 Slide: 12

13

Ancillary revenue/ scheduled pax 56 80 84 83 Ancillary revenue/ all pax (inc. charter) 56 79 84 80 10 20 30 40 50 60 70 80 90 Q3 08 Q3 09 Q3 10 Q3 11

Ancillary revenue per passenger (NOK)

Slide: 14 Slide: 14

15

Target

16

Slide: 17 Short-haul Long-haul

18

– 737-800: 44 (increase of 15 since last year) – 737-300: 17 (decrease of 11 since last year)

– 1 lease – 1 owned

Slide: 19 Slide: 19

Slide: 20 Slide: 20

Mailing address P.O. Box 113 No – 1330 Fornebu Visiting address Oksenøyveien 3 Telephone +47 67 59 30 00 Telefax +47 67 59 30 01 Internet www.norwegian.com Organization number NO 965 920 358 MVA

Slide: 22