SLIDE 4 ASK 2,182 2,674 3,507 4,498 Load Factor 77 % 75 % 75 % 74 %

77 % 75 % 75 % 74 %

0 % 20 % 40 % 60 % 80 % 100 % 1,000 2,000 3,000 4,000 5,000 Q1 08 Q1 09 Q1 10 Q1 11

Load Factor Available Seat KM (ASK)

ASK Load Factor

+ 28 %

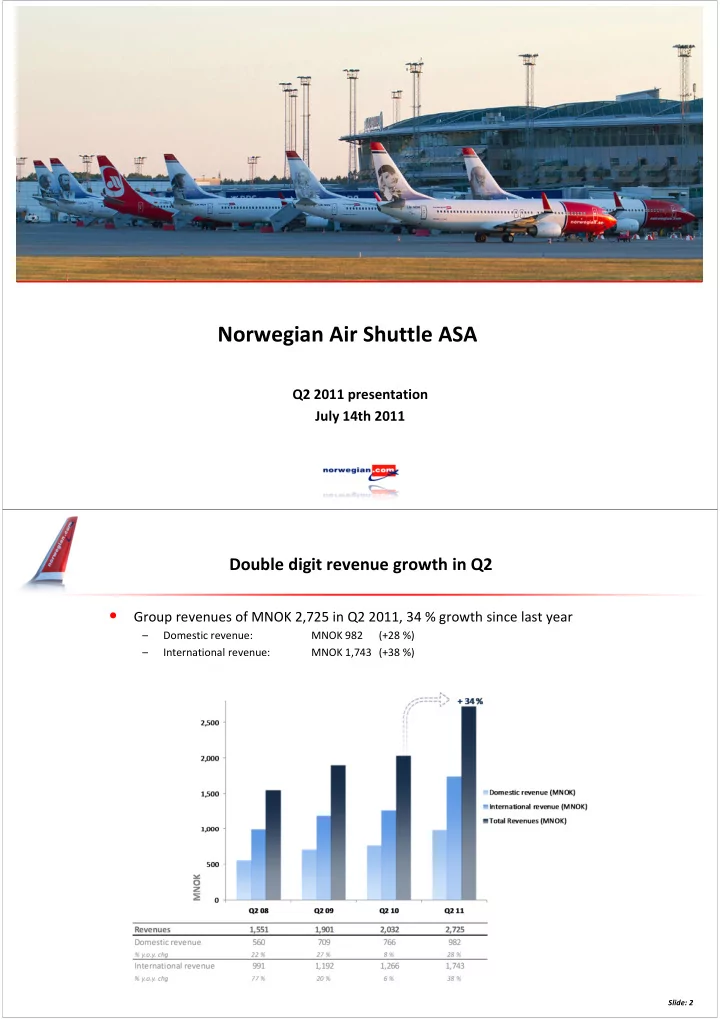

Production growth of 24 % in Q2

- 78 % load factor in Q2

- Load up 3 p.p. from last year

– Up 2 p.p. adjusted for last year’s closure of European airspace

Slide: 7 Slide: 7 ASK 2,974 3,469 4,449 5,518 Load Factor 78 % 78 % 75 % 78 %

78 % 78 % 75 % 78 %

0 % 20 % 40 % 60 % 80 % 100 % 1,000 2,000 3,000 4,000 5,000 6,000 Q2 08 Q2 09 Q2 10 Q2 11

Load Factor Available Seat KM (ASK)

ASK Load Factor

+ 24 %

- 26 % growth from last year

- An increase of 840,000 passengers

– Increase of 540,000 adjusted for last year’s closure of European airspace

Passengers (million) 2.3 2.8 3.2 4.0 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 Q2 08 Q2 09 Q2 10 Q2 11

Passengers (million)

+ 26 %

Passenger record:

More than 4.0 million passengers in Q2

Slide: 8 Slide: 8