SLIDE 1 JUNE 29th, 2020 Buy common Mid-America Apartment (MAA) / Sell common Boston Properties (BXP): A Play on Migration Trends

Sticking with the bearish theme on offices, this is a REIT sector pair trade that encapsulates how COVID-19 and WFH serves to accelerate migration to non-gateway cities, as these places offer a lower cost of living, less population density and congestion, and perhaps a higher quality of life. Time frame is 12 to 18 months. From the employees’ perspective, the motivation to move away from the inner cities and work remotely is pretty straightforward. Minimal exposure to viruses, less traveling and its associated costs, cheaper rent, and flexibility. Having experienced the benefits, some may want to continue with this arrangement permanently, in exchange for lower pay or similar concessions. And from the employers’ viewpoint, the pandemic has brought to light how densified floorplans for offices, where white-collar workers sit close to one another, are no longer as viable. Judging by how quickly the

- utbreak can spread at various meat plants and factories, I think the likelihood of infections getting out of

control in a populated office is very high. Thus, there is now a choice for companies to make going forward. They can either:

- Invest in more office space so that employees have more personal room to allow for social

distancing, while spending a significant amount of time and dollars implementing new health policies and safeguards. Alternatively, companies can rotate the people coming into the office on certain days instead of increasing floorspace, though this method may result in inefficiency.

- Have employees work remotely.

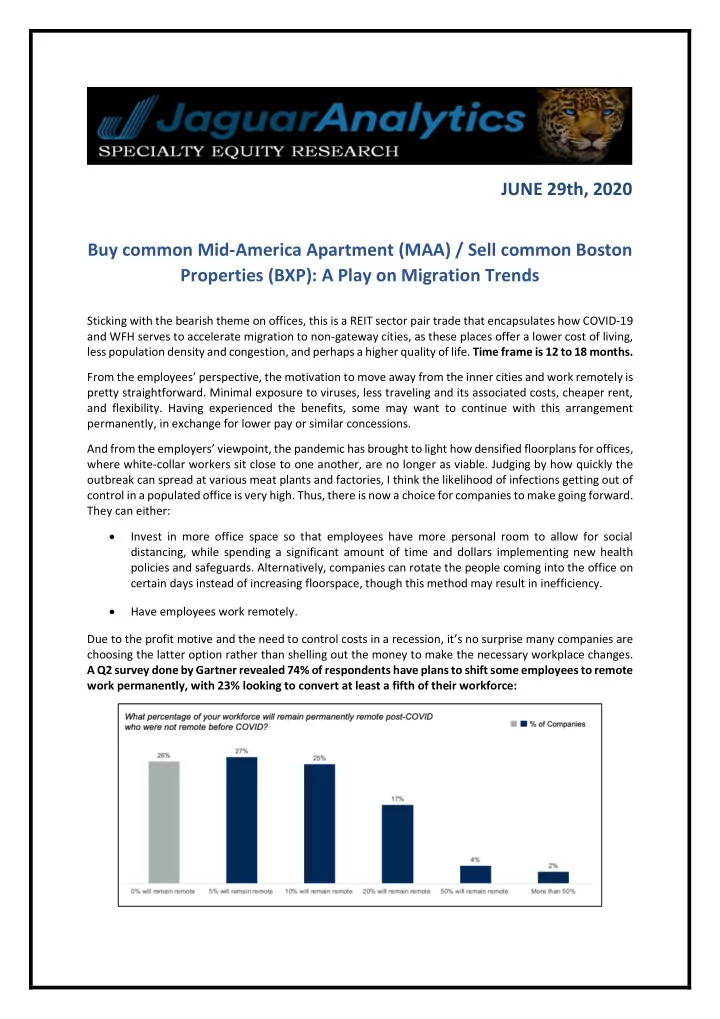

Due to the profit motive and the need to control costs in a recession, it’s no surprise many companies are choosing the latter option rather than shelling out the money to make the necessary workplace changes. A Q2 survey done by Gartner revealed 74% of respondents have plans to shift some employees to remote work permanently, with 23% looking to convert at least a fifth of their workforce:

SLIDE 2

COVID-19 and migration/WFH trends are bearish for Boston Properties (BXP)

A well-known commercial REIT, Boston Properties deals in large scale Class A office properties (close to 200 in total), with a focus on the central business districts (CBD) of five major gateway cities: Boston, New York City, Washington DC, Los Angeles, and San Francisco. Below is a geographic breakdown of the company’s portfolio, in net operating income terms: Heading into this COVID-19 crisis, the company had already been struggling with slow growth for years, due to oversaturation in city centers, management’s high level of conservatism (they only look to acquire extremely low risk assets with lease duration of at least 96 months), and just by virtue of already being the largest publicly-traded office REIT in the country. That’s the short explanation of why the stock had been going nowhere from 2015 to 2020: Looking ahead, the bear case for the remainder of the year is pretty obvious, but if we were to look at the company more intricately, it becomes clear Boston Properties is going to feel the pain more than most of its peers. Three are three major reasons for this.

SLIDE 3

- 1. Offices that cater to banks and the financial sector are at high risk of downsizing initiatives due

to WFH trends. Looking at Boston Properties’ portfolio, we can estimate that ~30% of their tenants are in the financial industry (including RE and insurance): One striking observation that has gone under the radar regarding the pandemic was how quickly the employees of major banks and financial services firms adapted to remote work, despite all of the complications and data security risks involved. As the industry weighs spending cuts to counter the economic crisis, permanently shifting finance jobs away from the office would save millions annually on rent and infrastructure. Personally, I think banking and finance employees tend to have an easier time working from home due to already being accustomed to the sedentary nature of their work and ease of setting up a home office (helped by better relative compensation vs other industries). Through JaguarLive, JaguarMedia and First Read, we’ve touched on multiple occasions how the leaders at Morgan Stanley (which currently has 90% of employees working from home), JPMorgan (90%), Mastercard (90%), Visa (“majority”), UBS (80%), and Barclays (“vast majority”) are now questioning the need for as much office floorspace. And we can now add Citi and Goldman Sachs to the list, after both banks recently said that the refilling of office desks is voluntary, including across seniority levels. BofA (major tenant of BXP) seems to be the lone holdout, with sections of the leadership insisting employees continue to be at their work desks. Looking at the overall picture, according to a Partnership for New York City poll in June, more than a third of respondents in the financial sector predicted that just 10% of their employees would return to city offices by August 15th, while 29% would return by December 31st. If firms are expecting less than a third of employees returning by the end of the year, it implies they likely have the remote work infrastructure in place to continue indefinitely, and I think the desire for less office space will only intensify. It also begs the question of whether companies can start sourcing talent across the nation rather than just locally. All of this will result in a weakening of Boston Properties’ negotiating power in both rent retention and prices. In square foot terms, roughly one-fifth of the company's leases will expire over the next two years. Looking at the most recent SEC filings, management is aiming to use upcoming renewals to increase rent per square foot from ~$55 currently, to $66 by 2022 and $68 by

- 2023. Based on WFH trends of the financial sector alone, I think those numbers will have to come down.

SLIDE 4

- 2. New York City fundamentals were already terrible going into the COVID-19 crisis.

We previously covered this topic in detail with our bearish case on Bank OZK. The key things to note are that population growth in NYC has been negative since 2017, and office demand was already declining with vacancies up 260 bps to 11.3% in the space of two years (see here), during what was supposed to be a good period economically for America! In FY19, NYC represented 35% of Boston Properties’ rental revenue, the highest exposure out of all the cities in which the company operates. To add to what’s already been discussed, Savills was out with a report on June 26th, forecasting Manhattan asking rents to decline 26% to a 9-year low of $62.47 a square foot in a prolonged recession. If that materializes, it will just spell further misery because Manhattan office rents had already been flat since 2015, based on Cushman & Wakefield data. Separately, Moody’s is forecasting office vacancy rates to rise to 20% by 2021, with NYC rents down 25%. Doing some rough math, that does seem about right. During the early 2000s recession, NYC office vacancies increased 910 bps from trough to peak. And during the GFC, they increased 620 bps. With vacancies currently at 11.3%, Moody’s estimate would imply an 870-bps increase, which is fairly realistic. Lastly, this is nothing new but has kind of been forgotten. The $10K cap on deductions for state and local taxes (aka SALT), as part of a 2017 tax code overhaul, has only served to make New York an increasingly unattractive place to live due to its high sales and property taxes. No doubt, this was a major contributor to the aforementioned negative population growth since 2017, and this will probably be exacerbated if the recession persists and/or remote work becomes permanent.

SLIDE 5

- 3. WFH-induced migration out of Silicon Valley is not baked into consensus.

Like financial industry professionals, the average tech worker is highly paid and faces minimal difficulties in transitioning to remote work. Thus, I think the risk of tech companies and startups eventually moving away from Silicon Valley to a “hire from anywhere” model is currently being understated. According to a 2Q20 CNBC workforce survey carried out in May, 44% of respondents from the tech industry reported incomes in the six figures, with 83% saying they’ve been able to work from home. Additionally, 27% say they want to work from home all the time from now on, while another 36% declared they want to work from home more often than they used to. We’ve already seen Twitter and Square announce employees will have the option to work from home

- forever. Meanwhile, Google and Facebook have announced plans to permit employees to do so through

the end of 2020. A similar trend is also emerging as well among the smaller firms, with a recent Forbes survey showing 76% of 165 tech startups saying the transition to WFH will be beneficial to productivity. This is important, because Boston Properties has 26% exposure to tech companies (with Salesforce being the largest tenant at 3.3% of the portfolio), with the majority in the Bay Area. If we assume working from home is going to persist, a lot of these software engineers and tech employees will no longer have much

- f a reason to continue living and paying expensive rent in this region, and the same goes for tech

- companies. In fact, Redfin carried out a polling last month and they found that more than 50% of

respondents would move out of San Francisco if they were given the green light to work from home permanently (and on a side note, 60% said they’d move out of Boston, which is another 33% of BXP’s revenue). The table below is a summary of Redfin’s findings, with San Francisco coming in second only to NYC in terms of net outflows: To add more color, migration out of expensive coastal parts of California is driving interest in “non- gateway” markets like Phoenix, Portland, Atlanta, Austin, and Dallas (where Mid-America Apartment Communities operates; more on this below). And Bay Area residents make up the largest portion of migrants looking to such spots, with nearly three quarters of out-of-town searches in those places

- riginating from San Francisco.

So, it’s not just migration from NYC that Boston Properties has to worry about, but migration from the West Coast too. This is yet another headwind.

SLIDE 6

Long offset to Short BXP: Mid-America Apartment Communities (MAA)

It is no secret the South region has been the focal point of the recent surge in COVID-19 cases, with large metros seeing the most extensive outbreaks. Should the situation remain elevated, I think this is going to drive an increasing number of people to not necessarily leave the region, but at least move to less densely populated markets. While some of those who migrate may buy a new house immediately, I suspect many are going to want to initially rent a place for at least 12 months, to get a feel for the situation and new surroundings. Moreover, housing supply remains low historically, a tailwind for rental demand. This will benefit Mid-America Apartment Communities, which is a residential REIT that operates ~102K apartment homes across the Southern Sun Belt states, specializing in smaller cities, suburbs, and regional non-gateway markets: Migration to these markets is not a new theme, as the company had been experiencing rent growth even before the pandemic. Impressively, just under 60% of all US domestic moves in the last decade were to markets where Mid-America operates, which has been the main driver for FFO growth:

SLIDE 7

Additionally, Mid-America’s operating expenses per property have been coming in well below their peers due to their local expertise, their heavy investment in technology, as well as aggressive cost control via their unique web-based property management system. The system is an all-in-one AI-driven solution which includes mobile maintenance technology that helps with on-site activities, management of individual apartment unit data, monitoring and addressing variances in utility usage, digital marketing, virtual online tours of properties, and automated leasing. According to management, the use of AI-screening and capture technology to efficiently drive qualified leasing traffic, combined with proactive utility monitoring and lease expiration management, has resulted in average annual same-property expense growth of 2.5% vs the sector average of 3.0%. In dollar terms, the company’s estimates its total annual value creation (AVC) from operating expense control has nearly tripled from $54.0M in 2015 to $140.4M in 2019. Mid-America is also in the middle of a large scale 2-year project to upgrade interiors and install smart home technology into 24% of its properties and by year end, with revenue benefit in 2021. Trials at 15 properties the previous year were well received, with mobile control of lighting, thermostat, security, and leak monitoring among the newly added features. Although the program was temporarily halted in March, installations are set to resume in July. All in, the company is forecasting $238.8M in net value creation from the project alone by 2021 (implying at least +70.1% AVC vs 2019). Meanwhile, the company’s high- speed internet access initiative is also being deployed, and will be offered at a discounted price to residents. Management expects the bulk cable program to have 50bps contribution to 2020 NOI growth. On rent collections and occupancy, there is nothing to worry about in this regard. The company recently provided an update at a conference in early June, saying they’ve collected 99% of April rent and 96% of May rent in cash. To provide some perspective, the industry average is just 90% for April and a preliminary 93% for May. Meanwhile, occupancy has remained steady at 95%, with 8,688 new leases in May vs year-ago 8,419.

SLIDE 8 There are several key reasons behind the resilience in the company’s numbers throughout the pandemic, and it is mainly to do with the high-quality resident profile, plus regional affordability. First off, 62% of all current residents are employed in white-collar industries that have remained intact in the face of COVID- 19, with WFH policies in place (which is a plus for Mid-America). Secondly, these residents are mostly single professionals in well-paying jobs, with average income ranging anywhere between $65K to $95K: Further, living costs in these non-gateway regions tend to be lower than the coastal cities and other large metros that these workers are migrating from, which results in rent eating less into monthly paychecks. While mentioning these advantages, CEO Eric Bolton (in the most recent conference call in May) also pointed out the fact that unemployment claims in these regions have been tracking at lower vs the national average, another reason why Mid-America will continue to see less rent growth and collection volatility than its peers: “when you look at the kind of weight our performance – of our portfolio of states, if you will, we continue to run at unemployment claims as a percentage of the employment base that at percentages lower than national average… But the other thing to keep in mind is that average rent to income of our portfolio at 20%, it’s a pretty affordable region of the country to live in, and dollar goes a lot further in our region of the country. And so, I think that – we think that while certainly there’s been some benefit from some of these federal assistance programs, I would suggest that it’s not a huge tailwind for us.” And lastly, Mid-America has made great strides in deleveraging its balance sheet the last several years, taking advantage of its investment grade rating plus favorable interest rate environment to lower borrowing costs and extend maturities. According to SEC filings, the average duration of MAA’s debt structure has been pushed out significantly from 2.6 years in 2016 to 7.5 years @ 3.9% currently, with

- nly $137.8M maturing this year and $193.5M in 2021 (FCF was $653.1M in 2019). And as of 1Q20, debt

to EBITDA remains historically low at 4.5 vs industry average of 5.0. Thus, the company has plenty of wiggle room in navigating the pandemic as well as borrowing capacity to make opportunistic moves.

SLIDE 9 Why a pair trade instead of just shorting Boston Properties directly?

The short answer is that correlations between stocks are currently high, with bottom-up fundamentals taking a back seat to an unpredictable tug of war between COVID-19 fears and stimulus. Good news and stimulus? Everything rallies. Bad news? Everything drops. Moreover, we’ve seen growth to value rotations take place for a couple weeks, only to reverse course suddenly and without warning. Making directional bets right now, especially in the commercial REIT sector, is akin to flipping a coin.

- In terms of upside, one thing the powerful rally from March has taught us is that we have a very

active Federal Reserve, Treasury, and White House who will intervene at all costs to protect the

- downside. And as ridiculous as it sounds, we also cannot forget the President has Twitter, and he

has shown on multiple occasions he is willing to make use of it to spark intense rallies. For example, back when crude was crashing in early April, all it took for oil prices to spike 40% in two days was a single tweet from President Trump about the prospect of negotiations with the Saudis and

- Russians. When it comes to these matters, we have no edge in predicting when exactly such

headlines and announcements will come.

- In terms of downside, one thing the crash in early March has taught us is that the aforementioned

trio are still neither quick nor proactive enough to prevent massive drawdowns. So, always being long because “the Fed has our back” is not a viable strategy either. They only have our backs after people have lost our shirts. Coming back to the trade idea, if we were to simply short Boston Properties without an offset, it may work for a while. But there is a risk the stock will have another 47% face ripping rally, like the one we had throughout Q2, if the FHFA makes an out of the blue announcement to extend mortgage payment relief,

- r the if Fed announces increased corporate bond buying. We have no edge in forecasting these headlines.

Where we do have an edge is in knowing MAA has better growth prospects than BXP going forward, thus the pair trade. If the Fed or FHFA suddenly announces something bullish and the entire REIT sector rips, who cares? We just need MAA to rip higher than BXP to make money. Similarly, if the entire market picks a random day to begin spontaneously tanking, who cares? We just need MAA to drop less than BXP. We can put on this pair trade and go to sleep at night not having to worry about where the S&P will go or where REIT stocks are headed.

Chronicle Yu

Research Analyst, Jaguar Analytics Email: cy@jaguaranalytics.com Twitter: @JaguarAnalytics