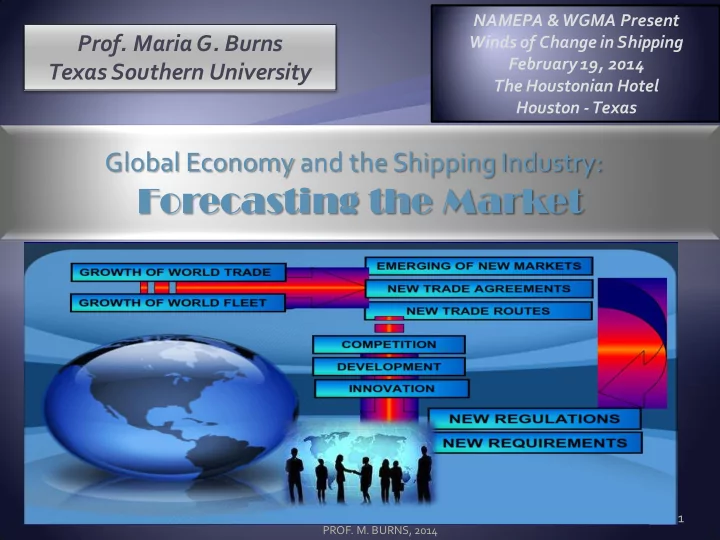

SLIDE 1

Global Economy and the Shipping Industry:

Forecasting the Market

1

- PROF. M. BURNS, 2014

- Prof. Maria G. Burns

Forecasting the Market 1 PROF. M. BURNS, 2014 2014 FORECAST! 80% - - PowerPoint PPT Presentation

NAMEPA & WGMA Present Prof. Maria G. Burns Winds of Change in Shipping February 19, 2014 Texas Southern University The Houstonian Hotel Houston - Texas Global Economy and the Shipping Industry: Forecasting the Market 1 PROF. M. BURNS,

1

MGB 2014

2

THE MANY FACES OF THE

MGB 2014

3

4

MGB 2014

5

SOURCE: M. BURNS - PORT MANAGEMENT AND OPERATIONS.*. CRC , 2014.

6

Source: M.BURNS - PORT MANAGEMENT AND OPERATIONS.*. CRC Press, Taylor & Francis Group

MGB 2014

7

MGB 2014

8

$77.00 $78.00 $79.00 $80.00 $81.00 $82.00 $83.00 $84.00 0.5 1 1.5 2 2.5 3 3.5

0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 1 2 3

$11,700 $11,800 $11,900 $12,000 $12,100 $12,200 $12,300 $12,400 $12,500 $12,600 1 2 3

MGB 2014

9

10

SOURCE: M. BURNS - PORT MANAGEMENT AND OPERATIONS.*. CRC Press, Taylor & Francis Group based on data from US Bureau Of Economic Analysis. 1980-2013,and China NBS, 2013.

100000 200000 300000 400000 500000 600000 700000 ASIA Shanghai, China Hong Kong, China Dalian, China Shenzhen, China Ningbo, China Guangzhou, China Quingdao, China QuinHUANdao,… Tianjin, China Rizhao, China Yingkou, China Nantong, China Xiamen, China Tokyo, Japan Yokohama, Japan Chiba, Japan Nagoya, Japan Kwangyang, S.… Busan, S. Korea Ulsan, S. Korea Inchon, S. Korea Port Kelang,… Kaohsiung, Taiwan OCEANIA Newcastle,… Port Hedland,… Dampier, Australia 2003 2007 2008 2011

MGB 2014

11

Figure 2.3 World’s Leading Ports: 2003-2013

Source: the Author based on data from World Shipping Council (2013), IMF (2013), Agência Nacional de Transportes Aquaviários - ANTAQ(Brazil), Institute of Shipping Economics & Logistics, Containerisation International Yearbook 2012; U.S. ArmCommerce Statistics Center, Secretariat of Communications and Transport (Mexico), Waterborne Transport Institute (China); AAPA Surveys ; and various port internet sites (2003-2013).

100,000 200,000 300,000 400,000 500,000 600,000 700,000 1 2 3 4 5 Shanghai, China Singapore, Singapore Tianjin, China Rotterdam, Netherlands Guangzhou, China Quingdao, China Ningbo, China QuinHUANdao, China Busan, S. Korea Hong Kong, China Port Hedland, Australia South Louisiana, LA, USA Houston, USA Dalian, China Shenzhen, China Port Kelang, Malaysia Antwerp, Belgium Nagoya, Japan MGB 2014

12

MGB 2014

13

14

MB, NAMEPA 2014

Millions

Used Oil from Land, Municipal & Industrial Waste

363

137

92

62

37

15

210

MGB 2014

15

16

MB, NAMEPA 2014

While the sources of anthropogenic (man-made) pollution receive considerable publicity, little is known of the naturally spilled oil and gas that the seas have been receiving and absorbing for 400 million years.

Non- Anthropogenic Pollution: Natural Seeps 60%

Anthropogenic Pollution: Extraction 2% Anthropogenic Pollution: Transportation, Refining, Distribution 4% Anthropogenic Pollution: Energy Consumption 34%

Source: compiled by M. Burns, based on data from Bureau of Ocean Energy Management, 2009 (w ww.boem.gov) and National Research Council, “Oil in the Sea” 2003 (w ww.nap.gov)

17

MB, NAMEPA 2014

MB, DOT 2013

18

TRANSPORTATION

MGB 2014

19

PRODUCTION : industrial zone, refineries. DISTRIBUTION CENTERS, Mass Storage Areas. TRANSPORTATION

MGB 2014

20

POLITICAL, MILITARY, ECONOMIC CENTERS

DISTRIBUTION CENTERS, Mass Storage Areas.

TRANSPORTATION I.T.

MB, DOT 2013

21

MGB 2014

22

Table: World seaborne trade in 2006-2012

LOADED UNLOADED

Year

Total

Crude Petroleum products and gas Dry cargo Total Crude Petroleum products and gas Dry cargo

2006 7,700.30 1,783.40 914.8 5,002.10 7,878.30 1,931.20 893.7 5,053.40 2007 8,034.10 1,813.40 933.5 5,287.10 8,140.20 1,995.70 903.8 5,240.80 2008 8,229.50 1,785.20 957 5,487.20 8,286.30 1,942.30 934.9 5,409.20 2009 7,858.00 1,710.50 931.1 5,216.40 7,832.00 1,874.10 921.3 5,036.60 2010 8,408.90 1,787.70 983.8 5,637.50 8,443.80 1,933.20 979.2 5,531.40 2011 8,747.70 1,762.40 1,033.50 5,951.90 8,769.30 1,907.00 1,038.60 5,823.70 2012 9,165.00 1,785.40 1,050.90 6,329.00 9,183.70 1,928.70 1,054.90 6,200.10

Sources: UNCTAD, Review of Maritime Transport, 2012, based on data supplied by reporting countries and as published on the relevant government, port industry websites and other specialist websites and sources.

MGB 2014

23

06 07 08 09 10 11 12 06 07 08 09 10 11 12

CARGO LOADED CARGO UNLOADED

SOURCE: M. BURNS - PORT MANAGEMENT AND OPERATIONS.*. CRC Press, Taylor & Francis Group based on data from UNCTAD Statistics, 1980 - 2013

MGB 2014

24

GLOBAL FLEET CARGO UNLOADED

06 07 08 09 10 11 12

SOURCE: M. BURNS - PORT MANAGEMENT AND OPERATIONS.*. CRC Press, Taylor & Francis Group based on data from UNCTAD Statistics, 1980 - 2013

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

25

PORT MANAGEMENT AND OPERATIONS.* M. BURNS . CRC Press, Taylor & Francis Group

1980 1985 1990 1995 2000 2005 2008 2009 2010 2011 2012 Oil & Gas 1,871 1,459 1,755 2,050 2,163 2,422 2,742 2,642 2,772 2,796 3,033 5 major bulks * 608 900 988 1,105 1,295 1,709 2,065 2,085 2,335 2,477 2,547 Other dry cargo 1,123 819 1,031 1,125 1,928 2,009 2,173 2,004 2,027 2,090 2,219 Container 102 152 234 371 598 909 1,249 1,127 1,275 1,385 1,498 Source: Compiled by UNCTAD, 1980 – 2013 UNCTAD review of maritime transport 1980 – 2013

* coal, alumina-bauxite, grain and oilseeds, iron ore, phosphate

26

MB, NAMEPA 2014

Compiled based on www.data.bsee.gov, 2013

85-86-87-88-89-90-91-92-93-94-95-96-97-98-99-00-01-02-03-04-05-06-07-08-09-10-11-12

Year Oil Gas 1985 6.009 0.834 1986 5.365 0.912 1987 5.211 0.978 1988 4.31 0.835 1989 3.564 0.687 1990 4.421 0.621 1991 7.764 1.241 1992 12.23 1.876 1993 11.91 2.575 1994 13.3 3.306 1995 15.99 3.788 1996 19.57 5.48 1997 26.36 7.419 1998 35.84 11.1 1999 45.45 16.71 2000 51.84 20.14 2001 56.44 23.28 2002 61.38 28.43 2003 62.36 32.19 2004 64.99 34.85 2005 69.72 37.7 2006 72.3 37.43

2007 70.1 36.51

2008 73.85 42.86 2009 80.22 44.99 2010 81.28 47.32

2011 78.55 46.77 2012 79.09 47.22

27

Source: M.BURNS - PORT MANAGEMENT AND OPERATIONS.*. CRC Press, Taylor & Francis Group

28

Source: M.BURNS - PORT MANAGEMENT AND OPERATIONS.*. CRC Press, Taylor & Francis Group

29

Source: M.BURNS - PORT MANAGEMENT AND OPERATIONS.*. CRC Press, Taylor & Francis Group

30

Source: M.BURNS - PORT MANAGEMENT AND OPERATIONS.*. CRC Press, Taylor & Francis Group

MGB 2014

31

32

Source: M.BURNS - PORT MANAGEMENT AND OPERATIONS.*. CRC Press, Taylor & Francis Group

33

34