SLIDE 1

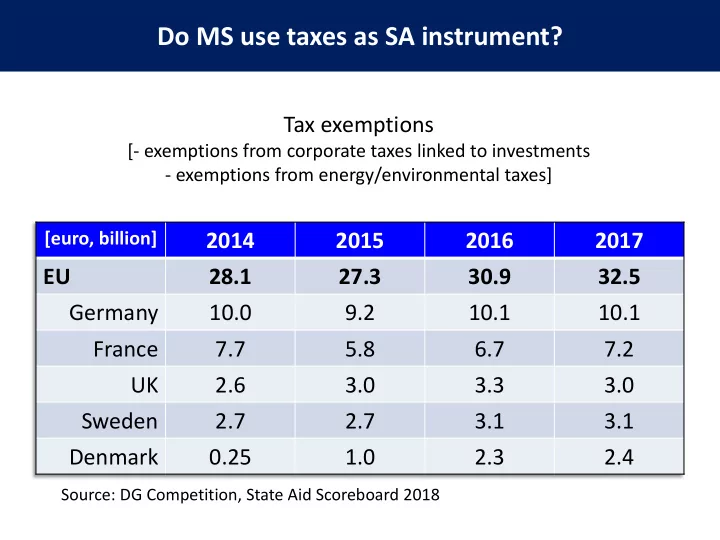

Do MS use taxes as SA instrument?

[euro, billion]

2014 2015 2016 2017 EU 28.1 27.3 30.9 32.5 Germany 10.0 9.2 10.1 10.1 France 7.7 5.8 6.7 7.2 UK 2.6 3.0 3.3 3.0 Sweden 2.7 2.7 3.1 3.1 Denmark 0.25 1.0 2.3 2.4 Tax exemptions

[- exemptions from corporate taxes linked to investments

- exemptions from energy/environmental taxes]