SLIDE 1

BMS HND - FA - Dhanushka Abeysekara 1

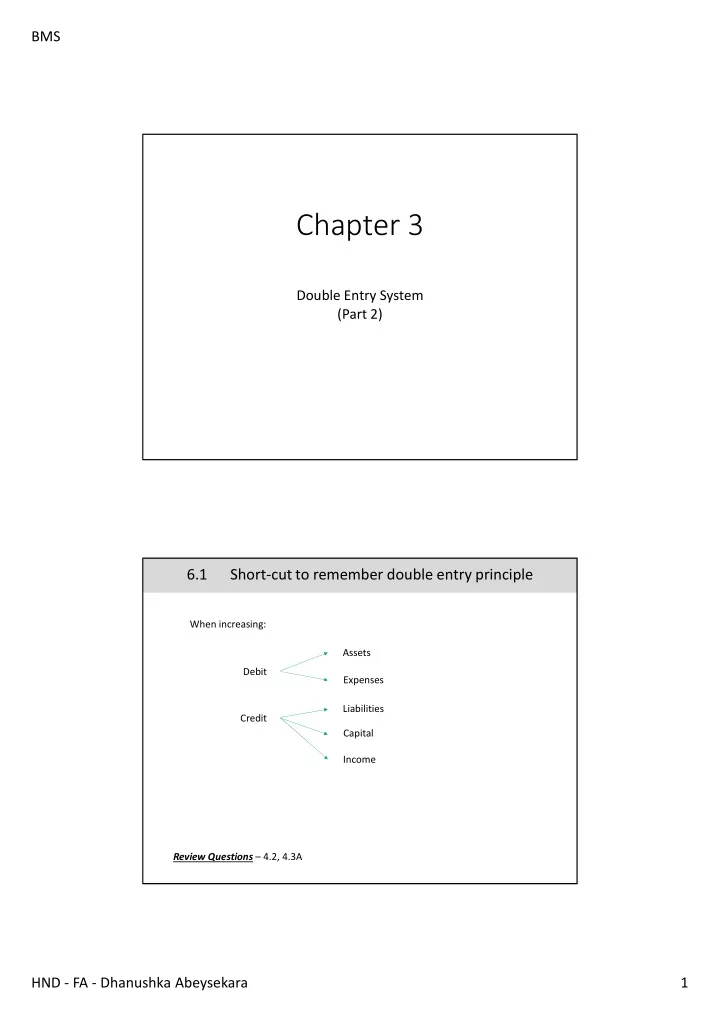

Chapter 3

Double Entry System (Part 2)

When increasing: Debit Credit Assets Expenses Liabilities Capital Income

6.1 Short-cut to remember double entry principle

Review Questions – 4.2, 4.3A

Chapter 3 Double Entry System (Part 2) 6.1 Short-cut to remember - - PDF document

BMS Chapter 3 Double Entry System (Part 2) 6.1 Short-cut to remember double entry principle When increasing: Assets Debit Expenses Liabilities Credit Capital Income Review Questions 4.2, 4.3A HND - FA - Dhanushka Abeysekara 1 BMS

BMS HND - FA - Dhanushka Abeysekara 1

Double Entry System (Part 2)

When increasing: Debit Credit Assets Expenses Liabilities Capital Income

Review Questions – 4.2, 4.3A

BMS HND - FA - Dhanushka Abeysekara 2

Bank Cash 15,000 Rent 80 Furniture 1,500 SP 330 Advertising 25 15,330 15,330 Bal C/f 13,725

15,330 1,605 Step 1 Step 2 Step 3

Closing balance is named as Balance carried forward (Bal c/f) For Income & Expenses closing balance is named as Profit or loss (P or L) Because Income & Expenses are transferred to Profit or loss (P or L)

Bank Bal b/f 13,725

As illustrated above the closing balance of one period becomes the opening balance of the following period Remember that balances of income and expenses are not carried forward to the following period. They are transferred to profit or loss

BMS HND - FA - Dhanushka Abeysekara 3

Debit balance = Debit side > Credit side Credit balance = Credit side > Debit side Closing balance in the credit side = Debit balance Closing balance in the debit side = Credit balance Opening balance in the credit side = Credit balance Opening balance in the debit side = Debit balance

$ Debit / Credit

Capital 20,000 Credit Cash 1,760 Debit Bank 13,725 Debit Purchases 8,900 Debit JM 2,000 Credit ERD 3,000 Credit Wages 170 Debit Rent 80 Debit Sales 10,200 Credit Furniture 1,500 Debit SP 250 Debit Fittings 600 Debit Advertising 25 Debit KM 8,090 Debit Drawings 100 Debit

Illustration – Debit balances and credit balances for example 1

BMS HND - FA - Dhanushka Abeysekara 4

Readings Study text – Chapter 5 – 5.1, 5.2