SLIDE 1

Roadmap for Petroleum Plays in South Australia

4 September 2014 in Whyalla

- 1. Overview

- 2. Offshore Oil & Gas

- 3. Onshore

Conventional Oil

- 4. Unconventional

Petroleum

- 5. Vision for Nirvana

- 6. Roadmap for O&G

- 7. Roundtable - Join us

1

Barry Goldstein, Executive Director – Energy Resources Department of State Development South Australian State Government

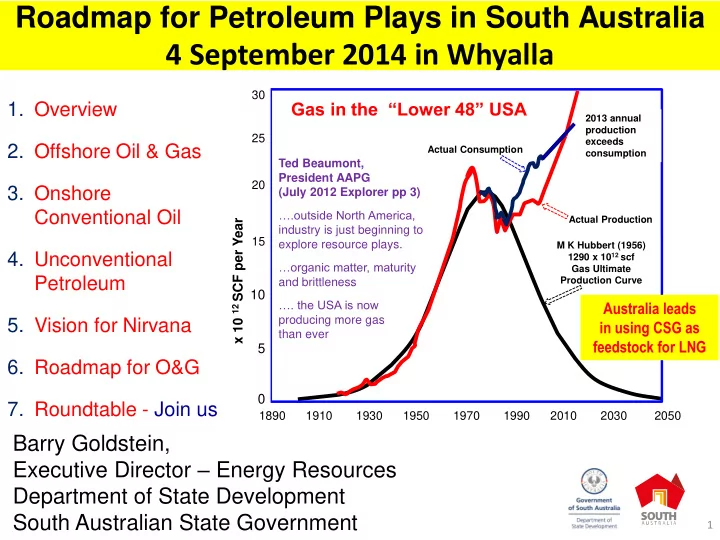

30 25 20 15

10 5

1890 1910 1930 1950 1970 1990 2010 2030 2050

x 10 12 SCF per Year

2013 annual production exceeds consumption Actual Consumption Actual Production M K Hubbert (1956) 1290 x 1012 scf Gas Ultimate Production Curve

Ted Beaumont, President AAPG (July 2012 Explorer pp 3) ….outside North America, industry is just beginning to explore resource plays. …organic matter, maturity and brittleness …. the USA is now producing more gas than ever

Gas in the “Lower 48” USA

Australia leads in using CSG as feedstock for LNG