SLIDE 1

3/3/2011 1

Investment Market Review

Presented By:

- J. Scott Adams, CCIM

President, Mid-South Region

March 2, 2011

Part of the CB Richard Ellis affiliate network

Investment Market Review

- Positive Signs in the Economy and Property Markets

- Trends in Property Sales (UP!)

- Trends in Distressed Assets (STABLILIZED!)

TOPICS TO COVER

CB Richard Ellis | Page 16

- The Lending Market Today (IMPROVED!)

- Summary Observations

Positive Signs - Economy and Property Markets

SIGNS ARE POSITIVE IN THE NATIONAL ECONOMY

- Recession over and protracted expansion phase

begun

- Painful reductions in employment begun to turn

around

CB Richard Ellis | Page 17

- Corporate America more profitable and productive,

so the capacity to hire is increasingly evident

- Return of bank credit for small businesses where

the majority of jobs are created

Positive Signs - Economy and Property Markets

SIGNS ARE POSITIVE FOR EACH OF THE MAJOR PROPERTY TYPES

- Especially positive for Office and Multi-Family

- Vacancy

factors well below previous cyclical peaks

CB Richard Ellis | Page 18

p

- Buoyed by job growth expectations and housing

market

Positive Signs - Economy and Property Markets

SIGNS ARE POSITIVE FOR EACH OF THE MAJOR PROPERTY TYPES

- Clear signs of stabilization for Retail and Industrial

- Vacancy factors remain above previous cyclical

peaks

CB Richard Ellis | Page 19

peaks

- Buoyed by increased consumer spending and

rising trade volumes

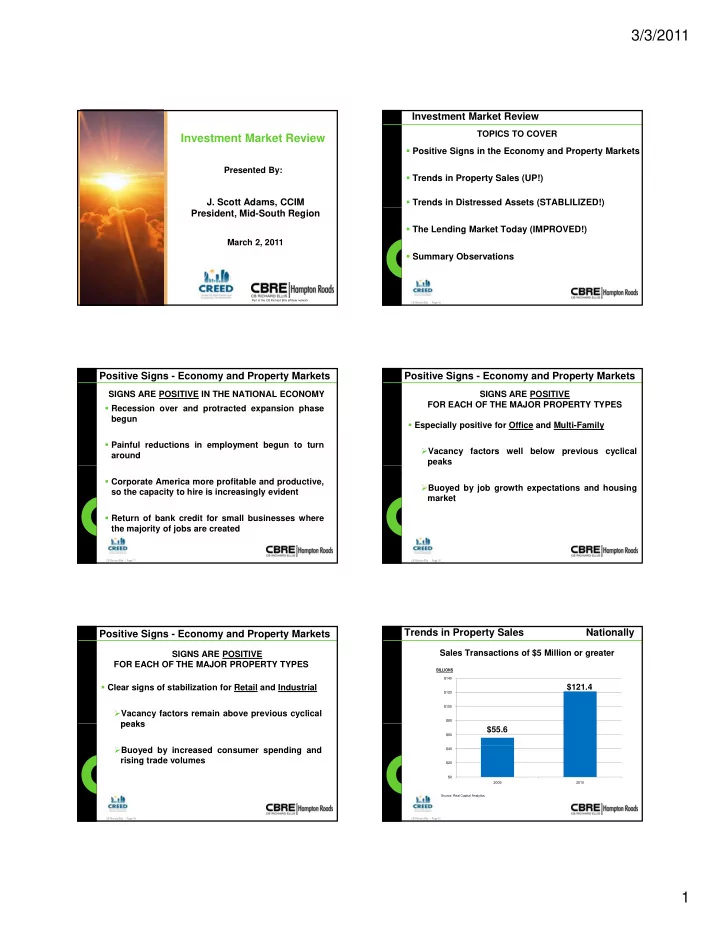

Trends in Property Sales Nationally

Sales Transactions of $5 Million or greater $121.4

$80 $100 $120 $140

BILLIONS

CB Richard Ellis | Page 20 Source: Real Capital Analytics

$55.6

$0 $20 $40 $60 2009 2010