SLIDE 1

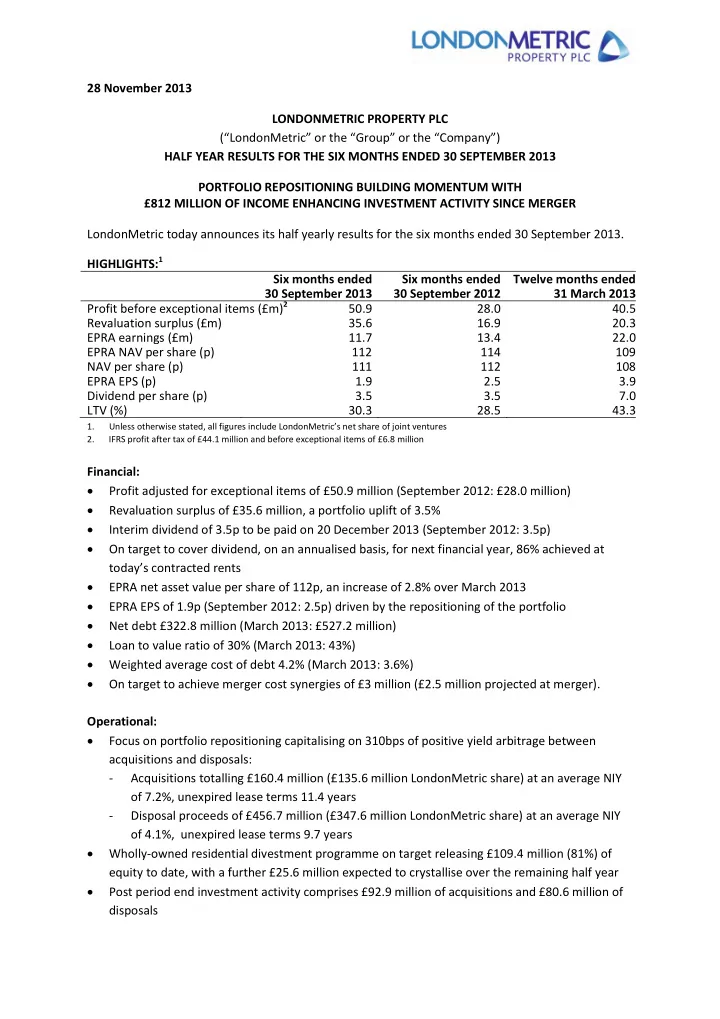

28 November 2013 LONDONMETRIC PROPERTY PLC (“LondonMetric” or the “Group” or the “Company”) HALF YEAR RESULTS FOR THE SIX MONTHS ENDED 30 SEPTEMBER 2013 PORTFOLIO REPOSITIONING BUILDING MOMENTUM WITH £812 MILLION OF INCOME ENHANCING INVESTMENT ACTIVITY SINCE MERGER LondonMetric today announces its half yearly results for the six months ended 30 September 2013. HIGHLIGHTS:1 Six months ended 30 September 2013 Six months ended 30 September 2012 Twelve months ended 31 March 2013 Profit before exceptional items (£m)2 50.9 28.0 40.5 Revaluation surplus (£m) 35.6 16.9 20.3 EPRA earnings (£m) 11.7 13.4 22.0 EPRA NAV per share (p) 112 114 109 NAV per share (p) 111 112 108 EPRA EPS (p) 1.9 2.5 3.9 Dividend per share (p) 3.5 3.5 7.0 LTV (%) 30.3 28.5 43.3

1. Unless otherwise stated, all figures include LondonMetric’s net share of joint ventures 2. IFRS profit after tax of £44.1 million and before exceptional items of £6.8 million

Financial: Profit adjusted for exceptional items of £50.9 million (September 2012: £28.0 million) Revaluation surplus of £35.6 million, a portfolio uplift of 3.5% Interim dividend of 3.5p to be paid on 20 December 2013 (September 2012: 3.5p) On target to cover dividend, on an annualised basis, for next financial year, 86% achieved at today’s contracted rents EPRA net asset value per share of 112p, an increase of 2.8% over March 2013 EPRA EPS of 1.9p (September 2012: 2.5p) driven by the repositioning of the portfolio Net debt £322.8 million (March 2013: £527.2 million) Loan to value ratio of 30% (March 2013: 43%) Weighted average cost of debt 4.2% (March 2013: 3.6%) On target to achieve merger cost synergies of £3 million (£2.5 million projected at merger). Operational: Focus on portfolio repositioning capitalising on 310bps of positive yield arbitrage between acquisitions and disposals:

- Acquisitions totalling £160.4 million (£135.6 million LondonMetric share) at an average NIY

- f 7.2%, unexpired lease terms 11.4 years

- Disposal proceeds of £456.7 million (£347.6 million LondonMetric share) at an average NIY

- f 4.1%, unexpired lease terms 9.7 years