SLIDE 1 1 The Internet and Financial Markets

Hal R. Varian School of Information Management, UC Berkeley

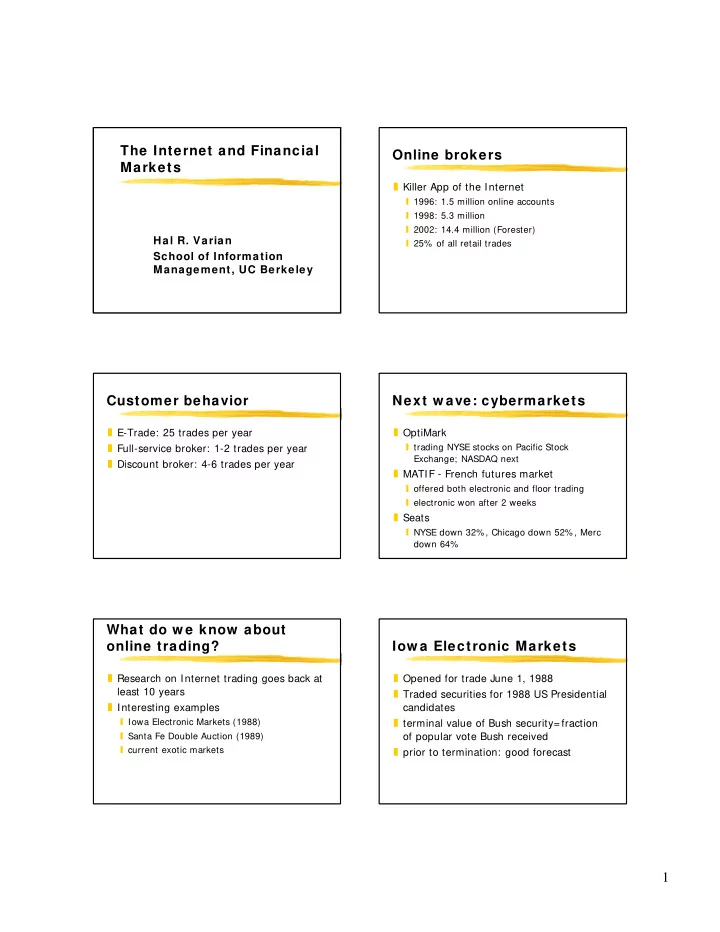

Online brokers

T Killer App of the Internet

S 1996: 1.5 million online accounts S 1998: 5.3 million S 2002: 14.4 million (Forester) S 25% of all retail trades

Customer behavior

T E-Trade: 25 trades per year T Full-service broker: 1-2 trades per year T Discount broker: 4-6 trades per year

Next w ave: cybermarkets

T OptiMark

S trading NYSE stocks on Pacific Stock Exchange; NASDAQ next

T MATIF - French futures market

S offered both electronic and floor trading S electronic won after 2 weeks

T Seats

S NYSE down 32% , Chicago down 52% , Merc down 64%

What do w e know about

T Research on Internet trading goes back at

least 10 years

T Interesting examples

S Iowa Electronic Markets (1988) S Santa Fe Double Auction (1989) S current exotic markets

Iow a Electronic Markets

T Opened for trade June 1, 1988 T Traded securities for 1988 US Presidential

candidates

T terminal value of Bush security= fraction

- f popular vote Bush received

T prior to termination: good forecast

SLIDE 2

2 Outcome of IEM

T Vote forecast for Bush: 53.2% (exact) T Vote forecast for Dukakis: 45.2% (off by

.2%)

T Comparison to polls

S much less volatile S polls exhibit classic biases S market did not exhibit biases

Why w as IEM so accurate?

T More rational participants?

S No, they showed same biases

T Market reflects weighted average

S marginal traders

R higher investment R higher return R more frequent trades R more “rational”

Santa Fe Double Auction

T Program trading in bid/ask market T Tournament play T $10,000 prize offered by IBM T 30 programs

S 15 economists, 9 computer scientists, 3 mathematicians, etc.

Outcome of Santa Fe

T Winner: Todd Kaplan, economics grad

student

T Why he won…. T What his program did

S “non-adaptive, non-predictive, non-stochastic, and non-optimizing”

Kaplan’s algorithm

T “Let others do negotiating. When bid and

ask get with 10%, jump in and steal the trade”

T Clearly dominated, even when other

programs optimized against it

T “Evolutionary tournament”

S after 28,000 plays had total domination S then market crashed!

Current exotic markets

T Idea Futures Market

S “DJIA below 7,000 by 11/30/99” S “Nuke capable terrorists by 2000” S “Mark McGwire hits more than 61 home runs”

T Hollywood Stock Exchange

S security payoff on box office gross during first 4 weekends S other entertainment bets

T Above are not for real money

SLIDE 3

3 HP sales forecasting

T Chen and Plott (1998) T Arrow-Debreu securities

S payoff contingent on sales of HP printers S internal to HP S real-money bets

T Consistently better than HP forecasts

Securitization

T David Bowie bonds = $55 million T Catastrophe bonds

S $477 million bonds tied to 1997 East Coast hurricane S $137 million bond tied to California earthquake

T Relationship to insurance markets? T Relationship to online trading?

Conclusions

T Electronic trading is here to stay T Exotic markets are useful forecasting tools T Electronic agents will be used, but may

well be passive

T Transparency is important T Securitization will thrive