1

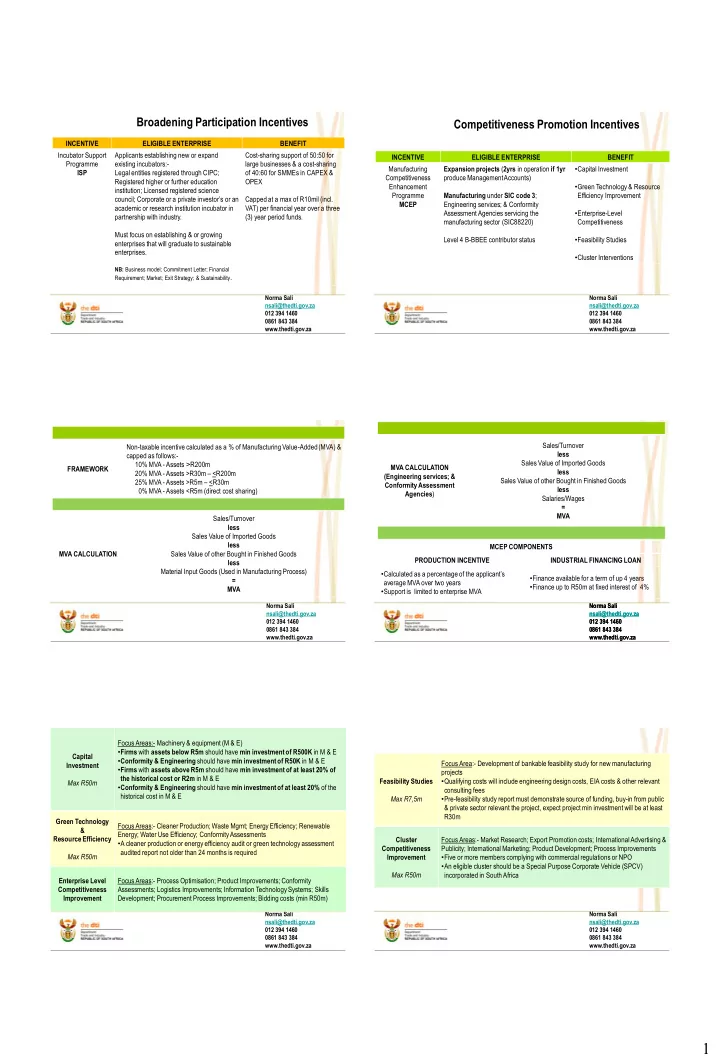

Broadening Participation Incentives

INCENTIVE ELIGIBLE ENTERPRISE BENEFIT Incubator Support Programme ISP Applicants establishing new or expand existing incubators:- Legal entities registered through CIPC; Registered higher or further education institution; Licensed registered science council; Corporate or a private investor’s or an academic or research institution incubator in partnership with industry. Must focus on establishing & or growing enterprises that will graduate to sustainable enterprises.

NB: Business model; Commitment Letter; Financial Requirement; Market; Exit Strategy; & Sustainability.

Cost-sharing support of 50:50 for large businesses & a cost-sharing

- f 40:60 for SMMEs in CAPEX &

OPEX Capped at a max of R10mil (incl. VAT) per financial year over a three (3) year period funds.

Norma Sali nsali@thedti.gov.za 012 394 1460 0861 843 384 www.thedti.gov.za

Competitiveness Promotion Incentives

Norma Sali nsali@thedti.gov.za 012 394 1460 0861 843 384 www.thedti.gov.za

INCENTIVE ELIGIBLE ENTERPRISE BENEFIT Manufacturing Competitiveness Enhancement Programme MCEP Expansion projects (2yrs in operation if 1yr produce Management Accounts) Manufacturing under SIC code 3; Engineering services; & Conformity Assessment Agencies servicing the manufacturing sector (SIC88220) Level 4 B-BBEE contributor status

- Capital Investment

- Green Technology & Resource

Efficiency Improvement

- Enterprise-Level

Competitiveness

- Feasibility Studies

- Cluster Interventions

Norma Sali nsali@thedti.gov.za 012 394 1460 0861 843 384 www.thedti.gov.za

FRAMEWORK Non-taxable incentive calculated as a % of Manufacturing Value-Added (MVA) & capped as follows:- 10% MVA - Assets ˃R200m 20% MVA - Assets >R30m – <R200m 25% MVA - Assets >R5m – <R30m 0% MVA - Assets <R5m (direct cost sharing) MVA CALCULATION Sales/Turnover less Sales Value of Imported Goods less Sales Value of other Bought in Finished Goods less Material Input Goods (Used in Manufacturing Process) = MVA

Norma Sali nsali@thedti.gov.za 012 394 1460 0861 843 384 www.thedti.gov.za Norma Sali nsali@thedti.gov.za 012 394 1460 0861 843 384 www.thedti.gov.za

MVA CALCULATION (Engineering services; & Conformity Assessment Agencies) Sales/Turnover less Sales Value of Imported Goods less Sales Value of other Bought in Finished Goods less Salaries/Wages = MVA MCEP COMPONENTS PRODUCTION INCENTIVE INDUSTRIAL FINANCING LOAN

- Calculated as a percentage of the applicant’s

average MVA over two years

- Support is limited to enterprise MVA

- Finance available for a term of up 4 years

- Finance up to R50m at fixed interest of 4%

Norma Sali nsali@thedti.gov.za 012 394 1460 0861 843 384 www.thedti.gov.za

Capital Investment Max R50m Focus Areas:- Machinery & equipment (M & E)

- Firms with assets below R5m should have min investment of R500K in M & E

- Conformity & Engineering should have min investment of R50K in M & E

- Firms with assets above R5m should have min investment of at least 20% of

the historical cost or R2m in M & E

- Conformity & Engineering should have min investment of at least 20% of the

historical cost in M & E Green Technology & Resource Efficiency Max R50m Focus Areas:- Cleaner Production; Waste Mgmt; Energy Efficiency; Renewable Energy; Water Use Efficiency; Conformity Assessments

- A cleaner production or energy efficiency audit or green technology assessment

audited report not older than 24 months is required Enterprise Level Competitiveness Improvement Focus Areas:- Process Optimisation; Product Improvements; Conformity Assessments; Logistics Improvements; Information Technology Systems; Skills Development; Procurement Process Improvements; Bidding costs (min R50m)

Norma Sali nsali@thedti.gov.za 012 394 1460 0861 843 384 www.thedti.gov.za

Feasibility Studies Max R7,5m Focus Area:- Development of bankable feasibility study for new manufacturing projects

- Qualifying costs will include engineering design costs, EIA costs & other relevant

consulting fees

- Pre-feasibility study report must demonstrate source of funding, buy-in from public

& private sector relevant the project, expect project min investment will be at least R30m Cluster Competitiveness Improvement Max R50m Focus Areas:- Market Research; Export Promotion costs; International Advertising & Publicity; International Marketing; Product Development; Process Improvements

- Five or more members complying with commercial regulations or NPO

- An eligible cluster should be a Special Purpose Corporate Vehicle (SPCV)

incorporated in South Africa