SLIDE 1

Understanding Brexit: : It Its complicated

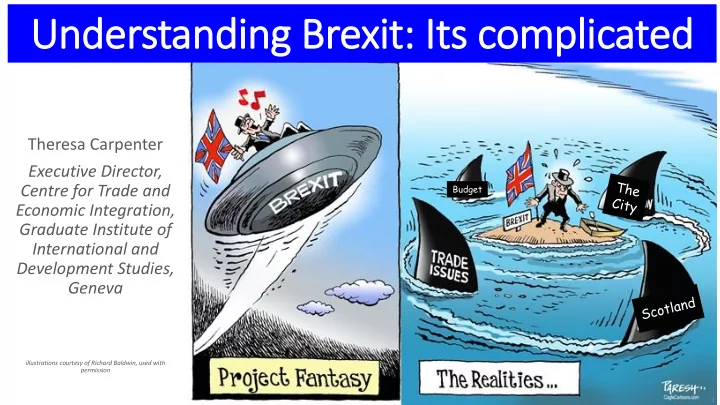

Theresa Carpenter Executive Director, Centre for Trade and Economic Integration, Graduate Institute of International and Development Studies, Geneva

illustrations courtesy of Richard Baldwin, used with permission 1

Budget