23.11.2009 1 –streng vertraulich, vertraulich, intern, öffentlich– Autor / Thema der Präsentation

1

Tools to optimize use of current supply

CITI: State of Telecom 2010 – New York, October 15th, 2010 Reinhard Wieck, Managing Director DT Washington Office*

*With Thomas Grob and Miguel Vidal, DT Group Headquarters

October 15, 2010 Reinhard Wieck, Managing Director, DT Washington Office / CITI State of Telecom 2010 2

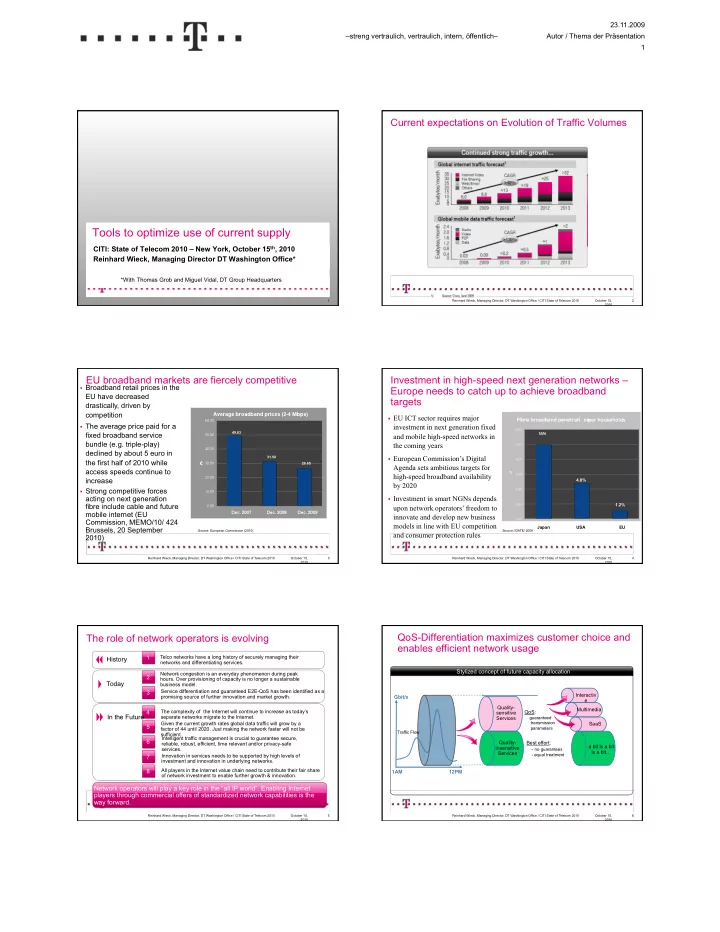

Current expectations on Evolution of Traffic Volumes

October 15, 2010 Reinhard Wieck, Managing Director, DT Washington Office / CITI State of Telecom 2010 3

EU broadband markets are fiercely competitive

- Broadband retail prices in the

EU have decreased drastically, driven by competition

- The average price paid for a

fixed broadband service bundle (e.g. triple-play) declined by about 5 euro in the first half of 2010 while access speeds continue to increase

- Strong competitive forces

acting on next generation fibre include cable and future mobile internet (EU Commission, MEMO/10/ 424 Brussels, 20 September 2010)

Source: European Commission (2010) 49.63 31.50 26.65 October 15, 2010 Reinhard Wieck, Managing Director, DT Washington Office / CITI State of Telecom 2010 4

Investment in high-speed next generation networks – Europe needs to catch up to achieve broadband targets

Source: IDATE/ 2009 49.63 31.50 26.65

- EU ICT sector requires major

investment in next generation fixed and mobile high-speed networks in the coming years

- European Commission’s Digital

Agenda sets ambitious targets for high-speed broadband availability by 2020

- Investment in smart NGNs depends

upon network operators’ freedom to innovate and develop new business models in line with EU competition and consumer protection rules

4.8% 1.2% Japan USA EU

October 15, 2010 Reinhard Wieck, Managing Director, DT Washington Office / CITI State of Telecom 2010 5

The role of network operators is evolving

Innovation in services needs to be supported by high levels of investment and innovation in underlying networks. All players in the Internet value chain need to contribute their fair share

- f network investment to enable further growth & innovation.

6 7

Network operators will play a key role in the “all IP world”. Enabling Internet players through commercial offers of standardized network capabilities is the way forward.

Telco networks have a long history of securely managing their networks and differentiating services. Network congestion is an everyday phenomenon during peak

- hours. Over provisioning of capacity is no longer a sustainable

business model.

1 2

History Today

The complexity of the Internet will continue to increase as today’s separate networks migrate to the Internet. Given the current growth rates global data traffic will grow by a factor of 44 until 2020. Just making the network faster will not be sufficient.

4 5

In the Future

Service differentiation and guaranteed E2E-QoS has been identified as a promising source of further innovation and market growth.

3

Intelligent traffic management is crucial to guarantee secure, reliable, robust, efficient, time relevant and/or privacy-safe services.

8

October 15, 2010 Reinhard Wieck, Managing Director, DT Washington Office / CITI State of Telecom 2010 6

QoS-Differentiation maximizes customer choice and enables efficient network usage

Stylized concept of future capacity allocation

Quality- insensitive Services 12PM 1AM Best effort:

- no guarantees

- equal treatment

Traffic Flow

Gbit/s QoS:

guaranteed transmission parameters

Quality- sensitive Services Interactiv e Multimedia SaaS a bit is a bit is a bit…